With the 12-month rate of CPI inflation now at 6.2%, inflation is once again in the news. Should we worry about inflation? If so, why?

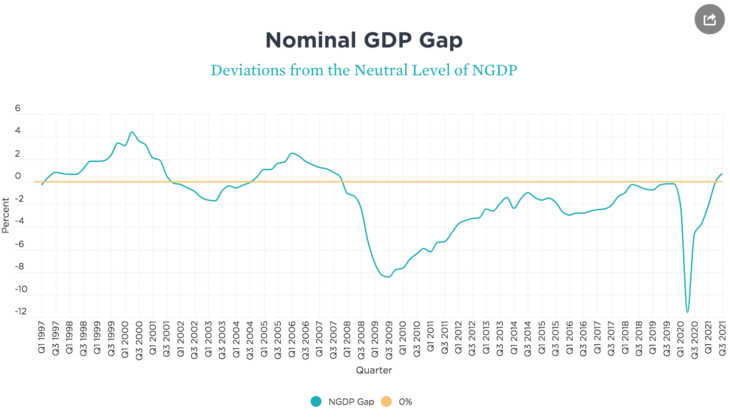

I have what might seem like contradictory views on inflation. On the one hand, I’m an inflation hawk who came of age in the 1970s and I view the high inflation of that decade as a major policy mistake. On the other hand, I’ve argued that inflation doesn’t really matter, that the so-called “welfare costs of inflation” are better measured by looking at NGDP growth. And a model produced by David Beckworth suggests that NGDP is back on track:

Of course, the 1970s didn’t just have high inflation, that decade also saw wildly excessive NGDP growth (11%/year from 1971-81), so there were good reasons for inflation hawks like me to worry about high inflation even if in some sense inflation doesn’t matter. The metric we prefer was just as excessive.

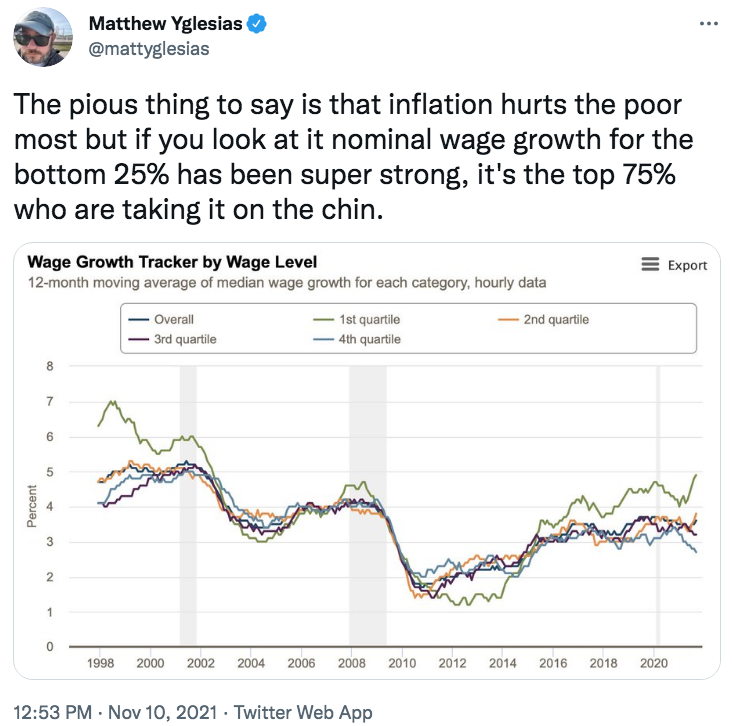

If you ask the average person why they worry about inflation you quickly realize that their actual concern isn’t inflation; it’s something more like falling real GDP. Thus they might fear that higher prices will cause a fall in their living standards. But higher prices are a zero sum game; they do not directly reduce the living standards of Americans. At this point some will shift the argument to “distributional effects”, and claim that some people are getting rich while the poor are being hurt by inflation. As Matt Yglesias pointed out today, however, the poor are seeing their incomes rise faster than any other group:

Real GDP growth has been lower than normal over the past 7 quarters, but growth is far better than in 2008-10, and that’s because the Fed switched to a monetary policy closer to what market monetarists like myself recommended back in 2008-09. At the time, we were told that a commitment to return prices or output to the previous trend line would make no difference at the zero lower bound. In fact, quickly bringing NGDP back to trend has resulted in a much better performance for RGDP, and hence living standards, relative to what we saw in 2008-10.

So why is inflation bad? After all, if one person pays more for a good, another receives more. And there’s really no evidence that the distributional effects favor the rich. The stock and bond markets did horribly during the high inflation 1970s. So why is inflation bad?

The textbooks say that one problem is menu costs, the cost of changing prices in menus, but those are pretty trivial. The main cost of inflation is that raises nominal interest rates. One cost of higher nominal rates is that people go to the ATM machine more often, but again that cost is pretty trivial. The main cost of higher nominal interest rates is that they distort the tax system. Higher inflation raises the nominal return on investments, which causes the real tax rates on investment to be higher than otherwise. I used to teach my students that if the nominal interest rate were 12% and the inflation rate was 10%, then the real rate of return would be 2%. If you then added a 50% tax on investment income, the real rate of return falls to minus 4% ((0.5*12%) – 10%). That’s a real tax rate of 300%. Thus inflation discourages saving and investment.

But note that the mechanism by which inflation discourages saving and investment is by raising nominal interest rates. In the previous example, in an economy without inflation the after-tax real rate of return would be 1% (50% of 2%), not minus 4%. Oddly, the recent bout of inflation has not raised nominal interest rates. The nominal rate on 5-year Treasury bounds is about 1.2%, while the real return on 5-year TIPS is negative 1.9%. Read that again, you earn negative 1.9% per year by investing in Treasury notes. And the TIPS inflation adjustment is also taxable.

Thus while the stock market did horribly from 1966-82, stocks have done very well in recent years. This time around, inflation has not resulted in high nominal returns on risk-free investments, and thus has not distorted our tax system to anywhere near the extent it did in the 1970s and early 1980s, when yields on Treasury bonds rose to nearly 15%.

So how should we think about the “inflation problem” that most consumers worry about? It’s not really an inflation problem; it’s a real GDP problem caused by supply chain disruptions. So yes, some people are suffering, but it’s not useful to think that “inflation” is the source of their problems; rather it’s a lack of real GDP growth. If you thought inflation was the source of the problem, then you’d advocate that we switch back to the failed policies of 2008-10. But the solution is not tighter money, it’s supply-side reforms.

This is not to say that we don’t have any inflation problem at all, i.e. an excessive rate of NGDP growth. While NGDP is roughly back on track, it now looks to me like we are going to overshoot what David Beckworth and I view as “neutral”. The TIPS spreads are too high. So I favor the Fed tapering, and indeed would like them taper even faster.

PS. After linking to Beckworth’s graph, Matt Yglesias had this to say:

I’m increasingly worried about the fact that I find myself agreeing with Yglesias more and more often. Hopefully, this is because he’s moving in my direction. I’d hate to think that I’m moving in his direction. 🙂

READER COMMENTS

William Connolley

Nov 10 2021 at 4:12pm

https://www.economist.com/graphic-detail/2021/11/06/a-handful-of-items-are-driving-inflation-in-america is interesting.

Andrew_FL

Nov 10 2021 at 4:22pm

Yes, your views are contradictory, because in your worldview, there is only tight money and high inflation, and high inflation doesn’t have negative welfare effects but tight money does. Your view is asymmetric and does not allow for any distortions and dislocations when NGDP is above trend like it does when NGDP is below trend. Only quickly rising prices, which you have struggled to articulate any problem with.

You are not moving in Yglesias’ direction. You were already there.

Scott Sumner

Nov 10 2021 at 6:36pm

Because you didn’t understand the post, I’d encourage you to read it again.

Andrew_FL

Nov 10 2021 at 7:22pm

The most you could come up with is that inflation makes taxes on investment worse. So if we didn’t tax investment, there’d be literally no problem with inflation.

Thomas Lee Hutcheson

Nov 11 2021 at 7:59am

No, inflation makes estimating future relative prices more difficult and so reduces the real returns to investment. But inflation also facilitates changes in relative prices which increases the real return on investment. The Fed’s job is to find the optimal rate and persuade decision makers that it will achieve it.

Matthias

Nov 11 2021 at 11:00am

I think the most you can read into the article is that if there’s effectively no tax on investment, than low, steady (ie well anticipated) inflation isn’t too much of problem.

The article doesn’t say much about high inflation, or about wild swings in inflation.

Andrew_FL

Nov 11 2021 at 11:12am

And I disagree with that, and it’s asymmetric.

Scott Sumner

Nov 11 2021 at 12:18pm

“The most you could come up with”

That’s more than you came up with. In any case, I did mention some other costs, but pointed out that they were relatively small.

And again, I think you missed the whole point of the post.

Andrew_FL

Nov 11 2021 at 3:38pm

More than I came up with? Well I suppose that’s true, I can’t take credit for the idea that inflationary policy sets in motion an unsustainable boom and misallocation of resources.

Scott Sumner

Nov 11 2021 at 8:31pm

No, that comes from an excessive NGDP growth policy.

Andrew_FL

Nov 12 2021 at 2:01am

So the Plucking Model is false, and business cycles do exist? Next you’ll tell me you don’t believe in the Crusonia Plant either!

Mark Z

Nov 10 2021 at 4:45pm

I think you overlook a couple of the biggest problems with inflation (or, really, with unexpected inflation), which is that it upsets pre-existing contracts and increases uncertainty in long term contracts going forward. Unexpected inflation arbitrarily redistributes from people with relatively inflexible wage/salary contracts to people with relatively flexible contracts. If I knew Fed were going to permanently increase the inflation rate to 6% the next time I had to negotiate a new salary, I wouldn’t so much care; but if you’re already locked into a contract based on prior inflation expectations, then you definitely care. And the second issue: unexpected increases in inflation tend to correlate with greater uncertainty in future inflation, which increases the risk premium on long-term contracts. I think these factors are likely much more important than things like menu costs.

Scott Sumner

Nov 10 2021 at 6:39pm

I agree that inflation creates uncertainty, although once again NGDP volatility is a better metric. But that’s not why average people worry about inflation.

zeke5123

Nov 12 2021 at 12:36pm

Well, average people do care about pre-existing contracts — it is called a salary. In the short-run, salaries are sticky so unexpected inflation does crimp someone’s life style.

Scott Sumner

Nov 12 2021 at 12:50pm

Supply chain problems don’t crimp lifestyles because wages are sticky, they reduce living standards because they make country’s poorer, they reduce real GDP.

On the other hand, a sudden demand shock (rising NGDP) does hurt those with sticky wages. Which is why talking about “inflation” is pretty meaningless.

Floccina

Nov 10 2021 at 5:36pm

If I buy VPU (Vanguard Utilities Index*), I do not think that I should subtract the inflation rate from the yield because I expect inflation to drive up the value of the assets and the yield up. In my thinking the problem with inflation and stocks, is inflation could cause the power companies to overestimate demand growth and over build.

Am I wrong?

Don’t laugh I’m past retirement age and hoping to live off dividends.

Scott Sumner

Nov 10 2021 at 6:38pm

Yes, inflation drives up nominal asset values. The problem is that you get taxed on both the real yield and the inflation adjustment. So high inflation is a problem.

Mark Brophy

Nov 10 2021 at 7:08pm

The problem with inflation is that it enables the government to spend more money. We need to to shrink the government rather than expand it.

Matthias

Nov 11 2021 at 11:01am

How does inflation do that?

(I assume we are talking about the real spending power, not nominal spending?)

Jon Murphy

Nov 10 2021 at 7:13pm

Scott-

Your posts over the past few weeks on NGDP and inflation have been insanely helpful to me. I am a microeconomist. A lot of what I am seeing at the macro level doesn’t make a lot of sense, but your posts help me sort through things (and, as an added benefit, I can explain inflation and the current macro situation to my students better).

Honestly, I feel better after reading your posts.

Scott Sumner

Nov 11 2021 at 12:19pm

Thanks Jon!

David S

Nov 11 2021 at 6:18pm

I’m with Jon–thank you. A few days ago I made a bet with myself that you would post a rational and concise response to the inflation brouhaha this week—and you did. You don’t sound too worried about Fed policy–maybe a modest acceleration to the taper plan is warranted over the next few months. I also appreciate that you’re adjusting your position based on fresh data.

I’m trying not to let myself get distracted by normal media outlets and statements by braindead politicians. I wouldn’t be surprised to read the following headlines going through January:

“Markets demand recession to cure supply chain problems!”

“Joe Manchin calls for Fed board to be replaced with veterans from the Bank of Japan!”

“Higher unemployment is the only way to save stores and restaurants!”

MarkLouis

Nov 10 2021 at 9:36pm

Seems to me that high inflation would increase the range from outcomes: bigger winners and bigger losers. If you’re on a fixed income or lack bargaining power, your standard of living is now falling quickly.

Real wages only tell part of the story; wealth inequality in increasing rapidly. This bout of inflation has been very good for asset owners but very bad for those who don’t own a home and/or don’t have enough savings to accept the risks associated with volatile assets

I can understand why inflation is unpopular.

Matthias

Nov 11 2021 at 11:03am

What is this bargaining power you are talking about?

And why, if you lack bargaining power, would you get screwed over less in a scenario with less inflation? Wouldn’t people take advantage of you just the same? Why not?

MarkLouis

Nov 11 2021 at 11:11am

Because we know wages are sticky on the downside. So even if you lack bargaining power it’s unlikely your wages fall. In a 2% world you can fall behind up to 2% annually. In a 5% world you can fall behind much more rapidly.

Dylan

Nov 11 2021 at 5:30pm

Interestingly, my wages have only ever seemed sticky on the way up. They’ve had no problem going down year after year for long stretches.

More seriously, total compensation doesn’t seem to be all that sticky, even in good times, ~20% of the workforce will see a compensation reduction year over year, even while staying at the same job. So my experience isn’t all that unique.

For me though, the issue with inflation is largely aesthetic. After decades of very low inflation, where the price of most of the goods I consume have stayed in a pretty tight range (my rent hasn’t changed in 10 years, the price of a can of soda is the same as it was in 2000, a pint of beer at a bar was $6, etc…) Now those prices have nominally increased a lot (beer is now $10+ and we only get 11oz, not even a pint!) So, everything feels very expensive. I suspect that is the case, even if your income has gone up proportionally, and when things feel expensive, you either consume less of them or consume the same amount and feel bad about it.

MarkLouis

Nov 11 2021 at 7:25pm

Yes I agree there is some level of sticker shock regardless of whether you’re on the winning or losing side of inflation. I know both: I have family members for whom COVID was a windfall and others who are on fixed incomes etc. Inflation is definitely worse for the latter.

Don’t tell Scott wages aren’t sticky downwards. If that’s the case we lose most of the economic support for fighting unemployment with monetary policy 🙂

Matthias

Nov 11 2021 at 11:37pm

That’s a good argument.

Though isn’t downward wage stickiness usually meant to imply that people will lose their jobs (instead of getting a wage cut), not that they will keep their current wages?

Scott Sumner

Nov 11 2021 at 12:21pm

“This bout of inflation has been very good for asset owners”

I doubt the inflation actually caused real asset prices to rise. I suspect it had more to do with the long term downward trend in real interest rates.

MarkLouis

Nov 11 2021 at 12:25pm

But those go hand-in-hand. The very definition of allowing inflation to overshoot is keeping interest rates lower than they otherwise would be – which means lower real rates.

Scott Sumner

Nov 11 2021 at 8:33pm

The Fed isn’t driving down long term real interest rates, it’s much deeper structural forces that are doing so. Yes, the Fed can affect short-term rates, but that’s not the main factor driving up asset prices.

Matthias

Nov 11 2021 at 11:41pm

Interest rates are a distraction.

For clarity, think of how this discussion would play out, if the Fed was instead using foreign exchange markets and exchange rates as their policy tool, not bonds and interest rates.

Singapore’s central bank doesn’t something like this.

An additional benefit is that zero lower bound is not even a theoretical problem.

Btw, if the Fed was buying and selling long term bonds, then the zero lower bound also wouldn’t be an issue. Even less sk if they were buying and selling consoles (ie perpetual ‘bonds’ that just pay a coupon forever).

zeke5123

Nov 12 2021 at 12:41pm

They have been great for asset managers. It is somewhat similar to your tax point. If I get a 20% carry on nominal growth but there hasn’t been any real growth, then I’ve shifted money from investor to manager for zero reason.

Ken P

Nov 11 2021 at 12:14am

The inflation story fits with your banana republic theory since our inflation figures are moving that direction. We’re now tied with Mexico. Our debt level limits our options and we are heavily skewed to short term debt so rising rates have a big impact.

If you’re low income and wages go up 6%, while gas is up 50%, utilities up 30%, meat 12%,… I don’t think its a good thing. If you’re a high earner or own assets you might think it’s a good thing if you cam kick the can down the road on paying your capital gains taxes.

MikeW

Nov 11 2021 at 7:43am

I’m retired, with a pension that is not indexed to inflation. So I definitely care about inflation.

MarkLouis

Nov 11 2021 at 8:52am

This is an example of the phenomenon I mentioned above: higher inflation will create bigger winners and bigger losers. At high inflation, someone in your shoes can see their standard of living fall quite rapidly. Truth is, economists don’t care as long as “on average” everything looks OK.

Matthias

Nov 11 2021 at 11:06am

Well, if financial markets were complete enough, you could just enter into a swap contract to turn your fixed income into inflation adjusted income.

(Basically the effect would be similar to short selling treasury bonds and going long on inflation adjusted bonds.)

MarkLouis

Nov 11 2021 at 11:14am

This illustrates the problem. By the time the average pensioner realizes the central bank has abandoned it’s mandate, markets would have long since adjusted the relative prices of nominal vs inflation-linked bonds. When you abruptly change the rules of the game, those closest to the game are going to win.

Thomas Lee Hutcheson

Nov 11 2021 at 5:50pm

It appears that the Fed has rather (finally) decided to play by the rules — its congressional mandates. The decade + of undershooting inflation was abandonment of its duty.

rsm

Nov 12 2021 at 3:47am

What if the Fed paid you inflation as interest on an individual Fed CBDC account?

Thomas Lee Hutcheson

Nov 11 2021 at 7:55am

The tax distortions could be alleviated by indexing, taxing only real interest and real capital gains just as savers and investors can contract for indexed income streams. But these adjustments are themselves costly. But beyond these costs, I think that estimating relative prices in the future — the essence of investing — is more difficult with higher inflation. Weighting these costs and benefits presumably goes into the Fed’s choice of its inflation target.

Robert Schadler

Nov 11 2021 at 10:00am

To add to Mark Louis’ points:

The assumption that everyone will anticipate the inflation correctly — or will anticipate it incorrectly in the same way — seems implausible. So, among the winners will be those whose anticipation is close to accurate.

Nor should we assume everyone adjust both their income and assets equally. How does a typical saver with 30-year bonds adjust; likewise those with a 30-year mortgage?

Free market advocates almost always include “rule of law” as a necessary element of markets working well. Among the chief merits of “rule of law” (not considering the substantive merits of good laws vs bad laws) is that it provides a necessary stability for long-range planning. The uncertainty that inflation engenders undermines that necessary stability for long-term planning.

And to focus simply on wages seems unusually narrow. For some, wages is their only source of spending power; some have other sources; for some wages are largely irrelevant to their overall economic well-being

MarkLouis

Nov 11 2021 at 10:59am

Well said.

An abrupt change in central bank behavior is essentially fiscal policy. When a central bank which targets steady inflation of ~2% all of a sudden allows for a significant (and permanent) overshoot it creates various winners and losers. The person who owns assets on leverage experiences a windfall (think Donald Trump). The person on a fixed pension experiences a loss (think our previous commenter). (And if you believe in loss aversion this may create net-negative well-being.)

All that occurs without any input from Congress or the electorate. This is the antithesis of the rule of the law or the spirit of a “fair” system.

If the central bank were to say “we’re raising the inflation target gradually over the next 10 years after consultation with Congress” I’d be Ok with that. Allow people ample time to adjust and give the electorate some input.

When the current dust settles and we look at the wealth distribution, there is little doubt in my mind that the winners of the past several decades will win again. And these people are the ones making policy.

What the Fed is in the process of doing is how central banks can lose credibility very quickly.

Scott Sumner

Nov 11 2021 at 12:23pm

The Fed’s shift to FAIT should reduce long run inflation uncertainty.

MarkLouis

Nov 11 2021 at 1:04pm

The market is clearly saying the Fed has abandoned FAIT. We are in the midst of an overshoot – so FAIT would call for bringing the price level back to the prevailing 2% trend over some future time period. Yet 30 year inflation expectations are currently 2.46%. Once you make a PCE adjustment let’s say that translates to 2-2.2%. If you apply that to the current price level we remain above the 2% trend into perpetuity. In other words, FAIT has been abandoned.

I assume you disagree, what part of that doesn’t make sense?

Scott Sumner

Nov 11 2021 at 8:35pm

Unfortunately, the Fed’s policy is a bit more vague than I’d like, but I continue to expect inflation to average closer to 2% during the 2020s than during the 2010s.

MarkLouis

Nov 12 2021 at 7:08am

If we managed monetary policy according to a NDGP futures market would you be equally skeptical of the market signals as you are of inflation expectations?

Scott Sumner

Nov 12 2021 at 12:52pm

I don’t know what you mean by skeptical of market signals.

MarkLouis

Nov 12 2021 at 1:06pm

Your view of “2% in the 2020’s” is significantly different from what one would conclude using market-based inflation expectations.

Of course we can all disagree with the market but that then makes it hard to argue something like ngdp futures should be used to set monetary policy, no?

MarkLouis

Nov 12 2021 at 1:16pm

For reference, 5yr inflation expectations are 3.17% as of right now.

Scott Sumner

Nov 13 2021 at 12:01pm

I expect inflation to average above 2% during the 2020s.

MikeW

Nov 11 2021 at 1:09pm

A big question is whether we can really trust them to stick with that. The political pressure on the Fed not to “take away the punch bowl” (or whatever the expression was) is going to increase. How long will they be able to hold out? Keeping in mind that presidents can, over time, change the Fed membership to align with their political desires…

MarkLouis

Nov 11 2021 at 2:05pm

I suspect inflation will be unpopular with the electorate. Already Republicans appear to be adopting inflation-backlash as a core platform issue. I suspect a “red wave” in 2022 will change the nature of the political demands on the Fed.

Thomas Lee Hutcheson

Nov 11 2021 at 5:55pm

Exactly. Inflation makes planning for relative prices far into the future more difficult. Indexing financial instruments and tax rules can reduce some of that uncertainty but not a lot.

Roger Sparks

Nov 11 2021 at 10:26am

The agriculture sector worries about inflation. High rates can make it nearly impossible to recover enough from this year’s crop to fully fund the crop inputs for next year’s crop.

Matthias

Nov 11 2021 at 11:07am

That’s seems rather weird.

Why would this supposed effect hit the agricultural sector harder than any other sector were proceeds get reinvested?

Roger Sparks

Nov 11 2021 at 1:54pm

Of course I oversimplify to give a quick answer, but I hope to convey the fundamentals.

Think of a farmer who sold last year’s crop. He paid all of his expenses, including living expenses, with enough money left over to do it again IF CONDITIONS ARE STABLE.

Comes spring, and he finds machinery cost are up, fertilizer cost up, prospective labor cost up, personal cost of living up, and just everything up. What does the farmer do? He hasn’t enough money to repeat last years farming program!

Our farmer, looking ahead, can borrow the shortfall from a bank, look to government for help, or if lucky, drawn on his personal financial reserves. From my experience, our farmer will do the math, worry, and make choices.

Agriculture is a competitive market. Our farmer will talk with the neighbors, gather information from all sources, and push ahead. After all, the year comes only once; sunshine and warmth are lost if unutilized.

But our farmer can’t do it alone. It takes a helping off-farm team to bring in a crop.

Matthias

Nov 11 2021 at 11:46pm

Thanks for explaining.

I would assume our farmer can either park his money at the prevailing real interest rate or lock in prices of his inputs via something like futures?

(If the real interest rate is negative, or he can’t lock in future prices of inputs and outputs, his economics worsen.)

In any case, I still don’t understand how the farmer is any different from anyone else in a seasonal business?

Though what you are describing is at most a transistory phenomenon, isn’t it? If inflation stays high and variable, and it really is a problem for farmers, enough farmers would exit the market until profitability returns. Wouldn’t they?

Roger Sparks

Nov 12 2021 at 11:17am

I had to think about these questions before trying to answer. Good questions.

First, about using futures or options: They can help (where coverage is available) but the skills needed to utilize this mechanism are not the skills usually found in the farming cohort. Also, the scaling of units is usually a poor fit for on the ground needs.

Next, variations within the seasonal business sector: I think all seasonal businesses are indeed somewhat the same. The biggest difference would be the degree of dependency upon off farm inputs like machinery, fertilizer and fuel. It’s the off-farm inputs that are sensitive to inflation. It’s also the off-farm inputs that makes possible the abundant production that the modern world enjoys.

Finally, farmer exit due to inflation: I read someplace that Venezuela farmers have nearly vanished but can’t verify that. I think the better answer is that farmers would try to store value seasonally in another currency, not the inflation troubled currency. I can’t really address this issue based on my own knowledge; the American dollar has been reasonably stable during my lifetime.

To close this comment, I think I will emphasize that modern agricultural production is a team effort, with most of the team off-farm.

Matthias

Nov 11 2021 at 11:10am

Scott, I wonder what the effective capital gains tax on the marginal invested dollar in the US is?

You correctly remark that even anticipated inflation hurts investment, because capital gains taxes (and taxes on dividends etc) are paid on nominal values, not real values.

But rich enough people can use buy-borrow-die to avoid capital gains taxes.

Scott Sumner

Nov 11 2021 at 12:25pm

If they die then they face death taxes, aka inheritance taxes.

robc

Nov 11 2021 at 5:27pm

If they stay below the $5MM (or whatever it is today) limit, they pay no death tax. And the cost value resets at time of death for those who inherit capital.

Personally, I somewhat agree with those who want to change the value reset rule. But I also want a 0% tax rate on capital gains. I am willing to compromise and combine the two!

Thomas Lee Hutcheson

Nov 11 2021 at 5:58pm

No reset, but index the value of the capital gain.

Scott Sumner

Nov 11 2021 at 8:37pm

Yes, but he said “rich”, which I interpreted as estates above $5 million.

Matthias

Nov 11 2021 at 11:50pm

I had people richer than 5 million USD in mind. Though I’m not quite sure, it depends a bit on how wealth is distributed empirically:

What I’m really interested in is the taxation on the typical dollar of capital. Or perhaps the marginal dollar of capital?

Btw, I’m in Singapore with zero capital gains tax, and about half my investments are in American markets. American capital gains taxes or death taxes don’t apply.

(I suspect if you are rich enough in the US, you can probably do some more tax shenanigans with shell conpanies or trusts etc?)

zeke5123

Nov 12 2021 at 12:44pm

Estate taxes are largely voluntary with proper planning. Seriously — if you look up how much money the estate tax generates it is very small because it is easy between trusts, foundations, etc. to reduce inheritance tax.

Mark Brophy

Nov 12 2021 at 11:18am

Rich people can’t use buy-borrow-die to avoid capital gains taxes unless interest rates are artificially low. We need to allow interest rates to operate in a free market.

Scott Sumner

Nov 12 2021 at 12:55pm

“We need to allow interest rates to operate in a free market.”

We already do. The fed targets the fed funds rate, but the rates that matter are set in a free market.

David Seltzer

Nov 11 2021 at 3:14pm

Scott: Excellent explanation. My understanding of macroeconomics, limited as it is, is aided by this post. What’s happening in the bond market seems contradictory to concerns regarding inflation. As a trader, I’ve seen the 2y/10y treasury spread narrow to 1.04. the 10y is around 1.45%…nominal. Are the bond traders saying there is zero anticipated inflation and real rates are a 55 basis point discount to historical 2% real rates? is there Inflation or decrease in supply in the short term causing prices to to reflect equilibrium? Thank you.

Thomas Lee Hutcheson

Nov 11 2021 at 6:04pm

Bond traders today believe that inflation over the next 10 years will average 2.7% pa; over the next 5 years, 3.00% Both are sharply higher since Oct 29.

Scott Sumner

Nov 11 2021 at 8:38pm

I suspect the equilibrium real rate on risk free bonds is now quite negative, and likely to remain so.

Ted Durant

Nov 11 2021 at 4:54pm

Why should I prefer stable NGDP growth and varying inflation over varying NGDP growth and stable inflation?

Isn’t inflation simply a tax on holders of currency?

Scott Sumner

Nov 13 2021 at 12:02pm

NGDP growth is a better indicator of the inflation tax than inflation itself.

Ted Durant

Nov 13 2021 at 10:41pm

Please explain, or point me to a paper/book section where you (or someone else) make(s) that argument in more detail.

Thanks!

Radford Neal

Nov 11 2021 at 8:41pm

It seems to me that you’ve missed the fundamental issue.

One can imagine that the problems you mention could all be solved – eg, tax law could be changed to only tax real rather than nominal gains, menu costs might go down with more experience of inflation, contracts could have inflation adjustment clauses, etc. Once all these issues are solved, inflation would be no problem!

Except, inflation is a _choice_ made by the government. Why do they make this choice? Could it be precisely _because_ of these issues that the choice to inflate the currency is made by those in power?

And beyond the issues that have been mentioned, the most fundamental one is that when the government inflates by creating money, real wealth is transferred from the people to the government – ie, it’s a hidden tax, not enacted by a democratic process. This may not be the primary motivation at fairly low levels of inflation, but is the dominant consideration in hyperinflationary episodes.

In summary, one must ask, if inflation doesn’t have any important effects, why would those in power choose to create it?

Matthias

Nov 11 2021 at 11:52pm

How is inflation as a tax less democratically enacted than any other tax?

The legislature passed laws for taxes. And they also pass laws to indirectly select what inflation a country is getting. The American Fed operates along guidelines set by law, and thsoe laws can be changed by the normal processes.

Radford Neal

Nov 12 2021 at 1:37am

Well, I doubt that the US congress is allowed to just delegate the setting of income tax rates to some bureaucrat. Not sure, but I think that may be contrary to the US constitution, and it would certainly be completely contrary to normal practice.

Furthermore, governments typically engage in propaganda campaigns to try to obscure their responsibility for inflation, and hence dodge any democratic accountability for the tax – instead, inflation is always the fault of greedy businesses, or greedy labour unions, or greedy foreigners… or maybe bad weather.

Thomas Lee Hutcheson

Nov 12 2021 at 5:36am

Inflation is a “choice” made by government only in the limited extent that the Fed’s targets are set by law as interpreted by the people appointed by law and by ownership of the Federal Reserve banks. The rhetoric of inflation as a “tax” is not vey useful. Better to think of the expenditure as the “tax” a that is what removes resources from alternative uses.

Radford Neal

Nov 13 2021 at 9:21am

Yes, its a “choice” made by the government in accordance with how the government operates. How else would the government make a choice? The choice is certainly not closely dictated by democratically-enacted legislation. There is considerable opacity regarding who really decides these things.

You’re right that it’s expenditures that really count, since those are what consume real resources. By that logic, income taxes, sales taxes, tobacco taxes, etc. are also not really “taxes”. But I think most people use “tax” to mean something the government does that provides it with the ability to make expenditures, partly because the funds obtained are fungible, so thinking of taxes and expenditures separately makes sense.

Scott Sumner

Nov 12 2021 at 12:59pm

Not sure what point you are making. In the post, I pointed out that the government benefits from inflation by getting more tax revenue. You pointed to another (much more minor) way they get more tax revenue. So what’s your point?

Radford Neal

Nov 12 2021 at 1:49pm

Maybe unfairly, I think I’m reacting less to what you said than to what you didn’t say. From your comment that “I’ve argued that inflation doesn’t really matter…” it seemed to me that, like many other people, you’re viewing inflation as something that just happens, without considering that it is a choice, made for some reason by those in power.

You do also say you’re an “inflation hawk”, and that this may seem contradictory. Your resolution of this contradiction by discussing NGDP growth hasn’t entirely resolved this for me…

But maybe I’m also really reacting to some of the other comments, rather than your post itself.

Alex S.

Nov 11 2021 at 10:38pm

Re: TIPS spreads. I sense that you might be looking at the 5- and 10-year varieties. If you’re not already keep an eye on the 5-Year, 5-Year Forward TIPS spread. As of 11/10 it was 2.3%. Assuming a spread of 0.3pp between the CPI and the PCEPI, it implies markets expect inflation will average 2% between 2026 and 2031.

Source: Federal Reserve Bank of St. Louis, 5-Year, 5-Year Forward Inflation Expectation Rate [T5YIFR], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/T5YIFR, November 11, 2021.

Scott Sumner

Nov 12 2021 at 12:58pm

I understand that. But you can argue that 2% is too high under FAIT. That’s why I focus on the 10-year TIPS spread.

BC

Nov 12 2021 at 4:33pm

“But the solution is not tighter money, it’s supply-side reforms.”

I agree that are problems today are with supply-side policies, not loose monetary policy. Record numbers of ships waiting to enter the Port of Los Angeles isn’t due to monetary policy. What are the most salient supply-side policies and reforms right now? More open immigration is the obvious low hanging fruit as immigration restrictions are estimated to have cut global real GDP by 50%. But, that has been true long before today’s supply shocks. Similarly for longstanding problems like occupational licensing and real estate zoning. (Although, perhaps occupational licensing and/or union rules play some role in our current truck driver and port capacity shortages? I read somewhere that it takes much longer for new truck drivers to get licensed today than the time required to complete their training.) On energy, I thought that US fracking was now the swing oil producer, stabilizing oil and natural gas prices, but the most recent spike in oil and natural gas prices has not seemed to raise US energy production, not enough to counter the price spikes anyways. Are recent energy/climate policy changes discouraging US energy producers from ramping up production in some way?

If nominal GDP (AD) has been stabilized, then inflation spikes must be caused by shifts in the AS curve, right? What has caused the current shift? If US GDP is about 21T, then each 1T of new government spending increases present value of future taxes by the same amount, about 4.8% of GDP. What is the expected deadweight loss per 1T as a percent of GDP? Even if one thinks current supply problems are due to Covid-related worker reluctance to return to work, one can view the pandemic aid checks as a form of leisure subsidies that still produce deadweight losses, right?

rsm

Nov 13 2021 at 1:55am

《If US GDP is about 21T, then each 1T of new government spending increases present value of future taxes by the same amount, about 4.8% of GDP. 》

Since Treasury makes money selling new bonds faster and often at higher prices than it redeems old bonds, is this tired old formula obsolete yet?

Are taxes even necessary?

Spencer Bradley Hall

Nov 13 2021 at 9:38am

“But higher prices are a zero sum game; they do not directly reduce the living standards of Americans”

You forgot to include the graph that shows inflation is surpassing wage growth.

#1 IRS Says Tax Brackets Will Be Higher In 2022 Thanks To Faster Inflation

#2 More Bad News For Biden As Real Wages Plunge

rr

Nov 13 2021 at 11:02am

Scott,

I buy everything you wrote here to include your supply side concerns. Curious. What are the top two supply side reforms you most recommend. And do you recommend any policy responses to offset any negative effects of those reforms?

Scott Sumner

Nov 13 2021 at 12:06pm

More immigration and eliminate residential zoning rules.

Of course I could cite many others as well, like freer trade and ending occupational licensing laws.

bb

Nov 15 2021 at 7:55am

@Scott,

That’s awesome. I assumed it would be something involving taxes, federal regulations, or unemployment insurance. I’d be 100% in favor of all of your suggestions. Thanks.

Grand Rapids Mike

Nov 13 2021 at 11:23am

If inflation is not bad, then why should the Fed not just keep on printing money. Part on!

Scott Sumner

Nov 13 2021 at 12:06pm

Because that would lead to fast NGDP growth, which is bad.

Grand Rapids Mike

Nov 13 2021 at 6:25pm

The same thing by a different name.

MarkLouis

Nov 13 2021 at 11:57am

Scott, economic theory question. Is there any level of corporate profit margins at which the inflation-> lower real wages-> more employment logic breaks down?

At the current profit margin levels (highest in history) it’s a bit hard to imagine that real wages are holding back hiring decisions.

Scott Sumner

Nov 13 2021 at 12:08pm

I agree that real wages are not currently holding back hiring decisions. There’s a labor shortage.

MarkLouis

Nov 13 2021 at 8:55pm

In all seriousness, where is the letter to the Fed “signed by 100 influential economists” that continuing to ease policy into a labor shortage defies any economic logic? (And yes, judging by inflation expectations policy is getting easier, not tighter).

Spencer Bradley Hall

Nov 14 2021 at 9:10am

N-gDp targeting is a bad policy to compensate for a failed economic policy, one where economists haven’t been able to increase R-gDp.

Roger Sparks

Nov 14 2021 at 10:04am

When money is created, the incremental increase in money supply has value because an economy is in existence already (which uses the same money). Hence, the workers who built over time have their monetary reward (for building) in the form of money waiting to be spent.

Any new money coming into the system introduces new monetary competition for whatever it was that they built. This new competition has both good and bad effects.

I think both central banks and private banks can introduce new money that gets into the ownership of the transactional sector. A discussion of the actual bank mechanics of money creation can distract us away from concentrating on how the transactional sector uses money as a store of value and medium of exchange.

Inflation would be one of the bad effects of the increased competition resulting from a money supply increase.

Jose Pablo

Nov 14 2021 at 9:55pm

Inflation kills long term fixed rate investors (long term bond investors, live insurance takers, live-saving mixed products, …). They keep getting the same nominal dollar returns that now can buy much less stuff. And the “principal” they get at the end of the investment period (nominal again) has much lower “real value” (it also buys much less stuff).

So, many (most of the time unsophisticated) investors that believed the “risk free” mantra discover that it was not that risk free (they suddenly realize inflation was a true risk they thought gone forever).

And yes, inflation (meaning “not-priced-in inflation”) is a significant transfer of wealth from savers (invested in long term fix rates securities) to debtors (indebted in long term fixed rates securities).

Jose Pablo

Nov 14 2021 at 10:03pm

For instance: inflation transfers wealth from holders of US government long term “risk-free” bonds to the US government. And there are lots and lots of holders of US long term bonds.

John Hawkins

Nov 19 2021 at 2:33pm

Scott, I was surprised to see you discount relative prices so heavily – I’ve personally been very intrigued by George Selgin’s argument for the Productivity Norm that heavily emphasizes minimizing changes to prices. Do you have a perspective on that?

Comments are closed.