Today, we received another jobs report showing that the labor market remains red hot. Unemployment fell to 3.4%, a 54-year low. Job growth was 253,000, which is well above trend and well above pre-report estimates.

By far the most important data point, however, is the growth rate of average hourly earnings. Nominal wages grew at a 6% annual rate in April, well above expectations. (The 12-month growth rate ticked up from 4.3% to 4.4%.) For a Fed that is trying to slow the growth in aggregate demand, this is bad news. For the purposes of monetary policy, wage inflation is the only inflation rate that matters.

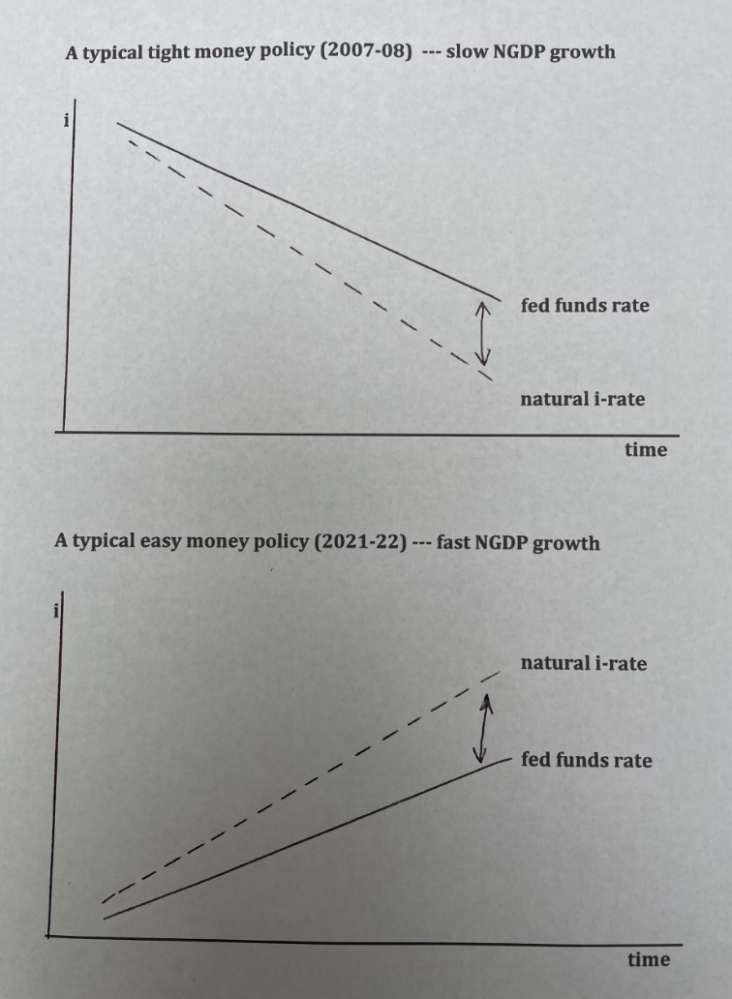

Why does the economy remain so hot, despite more than a year of “tight money”? Is it long and variable lags? No. A truly tight money policy reduces NGDP growth almost immediately. The actual problem is a misidentification of the stance of monetary policy.

I’ve discussed this issue on numerous occasions, but people don’t seem to be paying attention. So perhaps a picture would help. In the two graphs below I provide typical examples of a tight money policy and an easy money policy. Note that what really matters is the gap between the policy rate (fed funds rate) and the natural interest rate.

It’s not always true that a period of tight money is associated with falling interest rates, but that is usually the case. Does that mean the NeoFisherians are correct—that lower interest rates represent a tight money policy? No. For any given natural rate of interest, lowering the policy rate makes monetary policy more expansionary. That fact is clear from the way that asset markets respond to monetary policy surprises. But when the natural rate is falling (often due to a previous tight money policy), the policy rate usually falls more slowly. To use the lingo of Wall Street, the Fed “falls behind the curve.”

The opposite happened during 2021-22, when the Fed raised rates more slowly than the increase in the natural interest rate. In this case, it wasn’t so much the pace of rate increases, which was fairly robust, it’s that they waited too long to raise rates, by which time the natural interest rate had already risen sharply.

P.S. The natural rate cannot be directly measured; we infer its position by looking at NGDP growth. That’s why I ignore interest rates and focus on NGDP.

READER COMMENTS

Bobster

May 5 2023 at 2:28pm

Scott,

At this point should we return to NGDP trend to the pre-2020 trend or just return to 4% ngdp from current levels?

Scott Sumner

May 5 2023 at 7:40pm

If they had previously announced a policy of level targeting, then we should have returned to the trend line. But since they didn’t, 4% growth going forward would be better.

The Fed really messed up with its messaging.

Matthias

May 5 2023 at 7:48pm

Well, they could also try to get back to the price level trend they were on when they announced average inflation targeting.

Scott Sumner

May 6 2023 at 1:24am

Yes, but they later said they never meant it. It’s a mess.

Thomas L Hutcheson

May 5 2023 at 9:02pm

I agree. FAIT ought to mean that at every decision point the Fed is aiming for it’s 2% target. It would help, however if it explained why 2% and why it may be good temporarily to deviated from it.

Bobster

May 7 2023 at 1:51am

What are the implications for inflation if they target 4% going forward?

Does it mean higher inflation for longer since many contracts still need to adjust?

Scott Sumner

May 7 2023 at 12:21pm

I suspect that 4% NGDP growth would produce slightly above 2% inflation, as trend RGDP is slightly below 2%.

Bobster

May 7 2023 at 2:33pm

And that’s regardless of whether we return to trend?

Or if we return to pre 2020 trend will we have a recession and some deflation?

Scott Sumner

May 8 2023 at 12:40am

We aren’t going to return to trend; doing so at this late date would obviously cause a severe recession.

robc

May 8 2023 at 8:34am

Doesnt that depend on how fast you return to trend?

If they announced a 3.9% target going forward until they return to trend of 4%, then 4% target after that, they would eventually be back on trend. I doubt choosing 3.9 over 4.0 would cause a major recession.

Tsergo Ri

May 5 2023 at 2:38pm

If the monetary policy is loose, then why do you think the 5-Year Breakeven Inflation Rate is just 2.13 (https://fred.stlouisfed.org/series/T5YIE)?

Scott Sumner

May 5 2023 at 7:41pm

My argument is that monetary policy was loose in 2021 and 2022.

Breakeven rates are useful, but not perfect.

Grand Rapids Mike

May 5 2023 at 9:02pm

Monetary policy was not just loose, but think it was super loose if one considers the 38% M2 growth from March 2020 into January or so 2022. Along with the Gov. spending, how could inflation not be expected to be prolonged. While M2 has declined a bit, it doesn’t seem like very much, considering the mentioned 38% growth.

Also, just an anecdotal data point, here in the NW Chicago Suburbs there is no sign of construction spending stopping. The money is there for building stuff and so far it is not stopping. So I think the lags of excessive money growth has a way to go.

Thomas Hutcheson

May 5 2023 at 9:07pm

Why say “policy” is “loose?” [Your book explains why “policy” is an ambiguous concept.] Why not just say what the instrument settings should have been, at least qualitatively. It seem as useless as characterizing a Fed “stance.”

Thomas L Hutcheson

May 5 2023 at 6:07pm

“For the purposes of monetary policy, wage inflation is the only inflation rate that matters.” This seems absurd if only because “wages” is hugely heterogeneous, less so but of the same magnitude as the heterogeneity of prices of goods which make up “inflation.” Monetary policy aims to promote real income growth by facilitating changes in relative prices of goods and services and labor when different prices do not adjust equally to changes in supply and demand. How does one subset of prices get priority over others?

Thomas L Hutcheson

May 5 2023 at 6:13pm

While on the subject, why is 3.4% unemployment “hot?” It seem to imply “too high.” How do we know that?

Scott Sumner

May 6 2023 at 11:14pm

I’m not saying it’s too low, I’m saying it’s the lowest in 54 years.

Michael Sandifer

May 5 2023 at 11:23pm

Given inflation expectations, which should be the focus, I think pandemic-related supply and demand shocks are driving current high inflation, to the degree it’s high after stripping out lagged components. That NGDP growth is above trend, with roughly 2% core PCE inflation going out for years is telling. It certainly isn’t consistent with the idea that money’s still too loose, if one takes Treasury markets seriously.

vince

May 6 2023 at 2:42pm

Are you saying the Fed should continue to increase the federal funds rate until NGDP growth gets back to 4 percent? It was 6.6 percent in Q4 2022 and 5.1 in Q1 2023. It looks like that’s exactly what the Fed is doing.

Scott Sumner

May 6 2023 at 11:15pm

I’d say that roughly 3.5% NGDP growth would deliver 2% inflation.

Spencer

May 7 2023 at 9:48am

re: ” A truly tight money policy reduces NGDP growth almost immediately.”

That’s right! Powell’s attempting a soft landing.

Loans = Deposits.

Bank Credit, All Commercial Banks (TOTBKCR) | FRED | St. Louis Fed (stlouisfed.org)

But monetarism has never been tried.

Link: Daniel L. Thornton, May 12, 2022:

“However, on March 26, 2020, the Board of Governors reduced the reserve requirement on checkable deposits to zero. This action ended the Fed’s ability to control M1.”

Link the GOSPEL

http://bit.ly/1A9bYH1

Contrary to Powell and Selgin, banks aren’t intermediaries between savers and borrowers.

Spencer

May 7 2023 at 9:52am

Why do you think the commercial banks exclusively were saddled with Reg. Q ceilings in the GD?

Why do you think the ABA fought so hard to remove them?

Scott H.

May 8 2023 at 12:32pm

Is there a separate post on this? Otherwise, I could really use a more detailed explanation for the validity and desirability of this assumption.

Comments are closed.