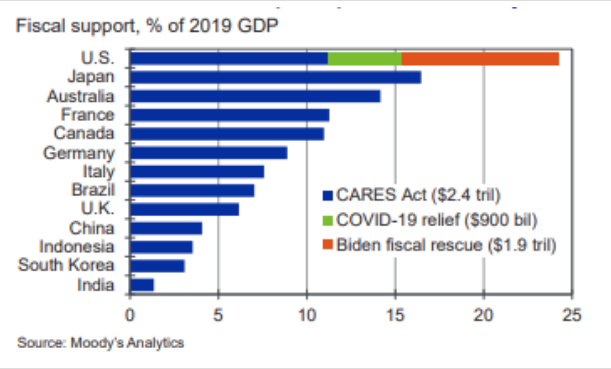

Greg Mankiw recently presented a graph showing that the US is doing much more fiscal stimulus than other big economies during the Covid crisis, even as a share of GDP:

I was struck by the big difference between the US and major European economies such as Germany, France and Italy. According to mainstream macroeconomic theory, the Eurozone economies should have been doing far more fiscal stimulus than the US.

The standard model suggests that monetary policy should steer demand during normal times. According to this view, there might be two situations where fiscal stimulus is appropriate:

1. If a country lacks an independent monetary policy.

2. If a country is stuck at the zero bound, and monetary policy is ineffective.

Both the US and the Eurozone have near-zero short-term rates. In contrast to the Eurozone, however, longer-term rates are well above zero in the US. So the case for monetary policy ineffectiveness is stronger in the Eurozone.

The US has an independent monetary authority that can provide stimulus when needed. Individual Eurozone countries lack such an authority, and thus might benefit more from fiscal stimulus.

This is not to suggest that I believe Eurozone countries should have done more fiscal stimulus. I’m skeptical of the efficacy of fiscal stimulus, and countries without an independent bank have less margin for error in terms of avoiding a debt crisis. Rather my point is that for whatever reason, developed countries are not following the playbook suggested by the standard model of fiscal policy. The US would be expected to do far less fiscal stimulus than the Eurozone countries.

PS. For those interesting in long run debt sustainability issues, I strong recommend David Beckworth’s podcast with Ricardo Reis. It’s a bit technical, but highly informative.

READER COMMENTS

Garrett

Feb 16 2021 at 3:14pm

Is this explained by the increasing influence MMT ideas are having? Has MMT taken hold more in the US than Europe?

Matthias

Feb 17 2021 at 12:35am

Might also just be the German influence in Europe?

(It’s not always the US that’s special.)

Scott Sumner

Feb 17 2021 at 2:03pm

I don’t see evidence that MMT is having any influence at all.

Jose Pablo

Feb 18 2021 at 12:51pm

One thing is having the CBO “watching” your fiscal policy and another, completely different, is having other 26 governments plus the European Commission “watching” your fiscal policy and threatening you with sanctions if you go even a little wild.

One of the European Union cornerstone are the rules to limit individual countries fiscal profligacy … it seems to be working

Thomas Hutcheson

Feb 16 2021 at 6:07pm

Maybe the US did zero “stimulus” but lots of “relief,” shifting consumption from people who were harmed less or not at all by the pandemic to those who were harmed more, but did it pretty sloppily.

Jerry Brown

Feb 17 2021 at 2:34am

I kind of think that some of the terminology is getting misused. I mean it might be appropriate for the government to spend money in an attempt to relieve suffering for those hardest hit by the economic changes caused by this pandemic totally separate from the idea of providing spending stimulus to an economy in recession in an attempt to increase demand and thereby pull an economy out of an economic recession caused by lack of aggregate demand.

Does that make any sense at all?

Marco Miorandi

Feb 17 2021 at 12:09pm

Isn’t the reason why EU countries are waiting to do fiscal stimulus that they’re waiting for the execution of the EU’s recovery plan (https://ec.europa.eu/info/strategy/recovery-plan-europe)?

Scott Sumner

Feb 17 2021 at 2:04pm

Thomas and Jerry, Yes, but much of the spending was clearly intended to be stimulus, not relief.

Henri Hein

Feb 17 2021 at 2:49pm

It was interesting to see this. I have been following your writings for a while, and I was curious what your position on stimulus is. You don’t get into it much in The Midas Paradox, which I do understand, as you had a lot of material to cover there.

Personally, and this is purely as a layman poking around at some data in my spare time, I have not found evidence that stimulus is effective. It doesn’t seem to boost employment, for instance, which is one of the stories often repeated to advocate for stimulus.

Scott Sumner

Feb 17 2021 at 5:31pm

I’ll cover this in the book I have coming out this year. It can have a very brief impact on spending, but over time it’s offset by monetary policy.

Henri Hein

Feb 17 2021 at 10:29pm

Cool, I’ll look forward to it.

Jose Pablo

Feb 18 2021 at 1:09pm

Maybe the impact is brief … but definitely seems to be “an impact”.

There were no hotel vacancies, and no restaurant tables this weekend in South Florida, and it took more than one hour to get a table for brunch at a no-reservations place on Sunday.

For less “anecdotal evidence”:

https://www.wsj.com/articles/us-economy-january-retail-sales-coronavirus-recovery-11613503145?mod=searchresults_pos9&page=1

https://www.wsj.com/articles/walmart-promises-raises-for-425-000-workers-after-strong-holiday-sales-11613652639?mod=searchresults_pos3&page=1

are not these the kind of news inflation is made of?

Henri Hein

Feb 20 2021 at 1:52pm

The restaurant backlog doesn’t tell me anything. It is a lot easier to pick up the phone or log on to opentable to make a reservation than it is to reopen a restaurant, or expand its services. So as lockdown restrictions ease, I would expect backlogs to develop.

Measuring the health of the economy by looking at sales data also strikes me as spurious. Employment is not going up, at least not significantly. When I look at the data over the past year, I don’t see any sign that stimulus boosts employment. (Sources: Treasury.gov and bls.gov).

Rajat

Feb 17 2021 at 8:29pm

My takeaway from the Reis discussion was that r<g, or – more precisely – r<m, is an anomaly, a 'bubble'. But we don't believe in bubbles, Scott. I think John Quiggin has long written about the 'equity premium puzzle' – why required rates of return on equity are much higher than on government debt, adjusting for risk.

Comments are closed.