This post discusses what should have happened in 2008-09 and what did happen in 2006-08. Reallocation of resources.

Instead, we got a deep recession in 2008-09.

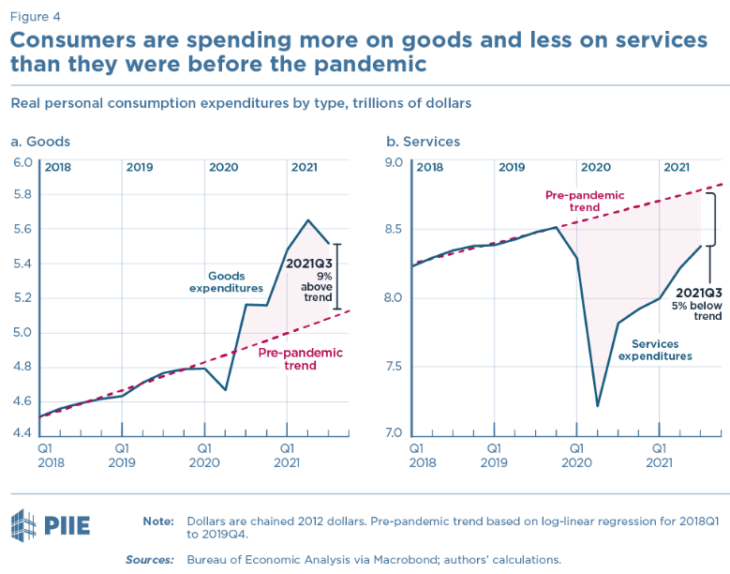

Fortunately, Fed officials learned from their mistake and when services tanked due to the Covid crisis they pumped up nominal spending enough so that the decline in services was mostly offset with a booming goods sector. This is from a very informative post by Jason Furman and Wilson Powell:

Between January 2006 and April 2008, housing construction plunged by more than 50% and yet the unemployment rate stayed low, rising from 4.7% to just 5.0%. That’s how it should be. Productive resources were reallocated from housing to other sectors. Then in late 2008, the Fed let NGDP plunge and output fell in almost all sectors of the economy. Unemployment surged to 10% in late 2009, and then declined at an agonizingly slow rate.

This time things were different. Unemployment surged to 14.8% in April of last year, but has already fallen back to 4.8% as job losses in services were partly offset by job gains in goods production. That’s how things are supposed to work. You don’t want to move inside the production possibilities frontier, you want to move along the PPF.

There can be a brief recession during a period of reallocation, but nothing like what we saw in 2008-09. For that, you need overly contractionary monetary policy.

HT: David Beckworth

READER COMMENTS

MarkLouis

Oct 30 2021 at 5:23pm

Makes sense although part of me wonders if the Fed is simply forced to choose between higher unemployment or an inflation overshoot. I don’t necessarily see why one is preferable to the other. Feels like a tradeoff between concentrated hardship or diffuse hardship.

Real GDP is still well below trend so it’s not yet clear which period will score better on that measure but we’re probably ahead this time around is my guess.

Scott Sumner

Oct 30 2021 at 6:38pm

There’s not much of a tradeoff. The higher inflation is just a smaller problem than the higher unemployment, it’s an order of magnitude smaller.

Brent Buckner

Oct 31 2021 at 9:33am

@Scott Sumner wrote: ” The higher inflation is just a smaller problem than the higher unemployment, it’s an order of magnitude smaller.”

…and that’s why the so-called “misery index” can be so misleading – it equally weights 1% of inflation and 1% of unemployment!

Thomas Lee Hutcheson

Nov 2 2021 at 8:12am

The “misery index” is exactly the tradeoff that is built into to NGDP targeting as a way for the Fed to achieve it employment and price change mandate.

MarkLouis

Oct 31 2021 at 12:08pm

I don’t see why that’s necessarily true. The entire population subject to a highly regressive tax vs a few million out of work and able to collect various unemployment benefits until they can be employed again. Not saying you’re wrong, I just don’t see why it’s obvious.

Scott Sumner

Oct 31 2021 at 12:51pm

Living standards depend on output. Output is far higher this time around, and it’s not even close. An extra 1% inflation is about a $20 billion inflation tax, peanuts compared to the labor market benefit.

MarkLouis

Nov 1 2021 at 8:54am

I’m not sure where you get $20b. US personal consumptions expenditures are $15-16t – an additional 1% tax on that is $150-160b. Annually.

We are 7 quarters past the peak of real GDP (Q4 2019) and the figure is now $460b higher. 7 quarters past the 2008 Q2 peak we were $320b lower. The net is $780b.

Inflation is running about 3% higher vs this point of the 2008 cycle. Applied to my $160b figure gets you to $480b.

First time i’m thinking through this using numbers so maybe there is a flaw here. But on the surface it seems like the outcomes may be fairly close.

Scott Sumner

Nov 1 2021 at 12:04pm

The inflation tax is the fall in the real value of the monetary base due to inflation. Rising prices are not a “tax”, after all, inflation also causes rising wages. The base is about $2 trillion.

Thomas Lee Hutcheson

Nov 2 2021 at 8:18am

But the size of the inflation tax is not a measure of it’s cost. The cost of one rate compared to another is the loss of real output that inflation caused via making long term planning more difficult vs making relative prices more flexible when there are nominal downward rigidities. Rights?

Benoit Essiambre

Oct 30 2021 at 9:05pm

I still can’t get over the mind boggling level of carnage the western world self inflicted in the decade following 2008, the untold human suffering, desperation and helplessness as livelihoods of a plurality simply disappeared. The subsequent rise of scapegoat xenophobia, demagoguery and Trumpism, the emboldening of authoritarian China and Russia, the unfortunate blow to the reputation of democratic liberalism, all easily avoidable. What a sad period. And so few seem to be aware of the root unforced mistake.

Michael Sandifer

Oct 31 2021 at 12:26am

I have to disagree about 2006-2008. NGDP fell during those years, completely unnecessarily. Sure, real growth is expected to fall at times, and even nominal growth temporarily, as during the pandemic, but it wasn’t necessary to nominal growth to fall from 2006-2008, particularly as it was a trend that simply continued until we were in a deepening recession.

Michael Sandifer

Oct 31 2021 at 12:27am

Sorry, I meant to type that NGDP growth fell from 2006-2008.

Scott Sumner

Oct 31 2021 at 12:52pm

It was good that NGDP growth slowed, it was too high in 2005-06.

Michael Sandifer

Oct 31 2021 at 6:06pm

Scott, it’s interesting you say that NGDP was too high in 2005-2006. By my calculation, it was still a bit too low then as well. There wasn’t complete catch up after the 2001 recession. Yes, the inflation rate was rising, but not because monetary policy was loose. That was due to the growing commodity shortages.

Of course, there are different ways to do these calculations. I take NGDP growth from Q3 1992 to Q3 2000, and then compare to Q3 2000 to Q3 2005. What intervals are you looking at?

Scott Sumner

Nov 1 2021 at 12:07pm

NGDP growth was 6.5% and unemployment was fairly low. That can’t go on forever without inflation running well over the Fed’s 2% target.

Michael Sandifer

Nov 1 2021 at 3:11pm

I see your point, with respect to the Fed’s inflation targeting regime, which is obviously pro-cyclical, but why judge it on that basis in this post, at least without mentioning that, from an NGDP level targeting perspective, money was tight? I’m not saying you don’t have a good reason, but that I don’t know what the reason is.

Also, why bother mentioning the NGDP growth rate or unemployment rate in this context? You’ve stated many times that these are not reliable metrics to determine the stance of monetary policy. We shouldn’t try to estimate what real GDP potential or NAIRU are, but instead level target NGDP. RGDP potential obviously fluctuates, as does NAIRU, and the unemployment rate hadn’t even returned to the pre-recession low. Of course, the NAIRU may have been higher due to higher commodity costs, but how do we really know? We’re guessing, if we’re using conventional econ. It’s part of what’s gotten the Fed in trouble in the past, which Powell so eloquently addressed in his “navigating by the stars” speech.

The current period is much clearer, because, if measured against the immediate pre-recession trendline, Fed policy is roughly on track, both from an average inflation targeting perspective and from a level targeting NGDP perspective. That’s not the trendline I think we should measure against, but at least one can say the Fed’s done a much better job during this cycle than in previous ones.

Andrew_FL

Oct 31 2021 at 9:35am

As long as we put the right Market Socialists in charge of centrally planning NGDP, we never have to pay any price for funding unprofitable investments out of money that hasn’t been voluntarily saved!

Scott Sumner

Oct 31 2021 at 12:55pm

You are mixing up RGDP (which can be centrally planned) and NGDP, for which the term ‘central planning’ is nonsensical. It’s like saying that inflation targeting “centrally plans” the price level, or the gold standard centrally plans the price of gold.

Andrew_FL

Oct 31 2021 at 3:21pm

Inflation targeting does in fact centrally plan the price level.

Michael Sandifer

Nov 1 2021 at 3:18pm

Andrew_FL,

I don’t entirely agree with how you characterize how current monetary policy is made, but I do agree that we should try letting the private market issue money and see what happens with monetary policy. I don’t think it should be tried in a large country, but perhaps a smaller country can experiment with 100% free banking and private monetary policy. It would be interesting to see what this looks like going in the third decade of the 21st century.

Even here in the US, I think we should experiment with alternative banking charters that allow for far less regulation, but also no moral hazard.

Andrew_FL

Nov 1 2021 at 3:39pm

Don’t reply to me, go work on your equations to describe the behavior of human beings. I rebuke you, Walrasian.

Thomas Lee Hutcheson

Nov 1 2021 at 6:40am

You are right that the Fed reacted quickly and on the whole very well. Unfortunately in March 2020 people did not know that the Fed was going to (almost) prevent a decline inflation and so acted mistakenly on expectations of a longer recession. The story about car companies cancelling cancelling their chip orders would be an example of the costs of the Fed not having established expectations of its policies.

I think the harm done by the Fed’s 2008-2020 behavior in not keeping inflation on target is still much underappreciated.

David S

Nov 1 2021 at 9:01am

I think that firms and individuals are capable of making bad decisions regardless of expectations about Fed policy.

I sure have.

David S

Nov 4 2021 at 2:33am

This thread is probably dead but I have insomnia and I’m mildly annoyed by Arnold Kling’s attempt to rewrite history in his review of Scott’s book.

https://www.econlib.org/library/columns/y2021/klingmarketmonetarist.html

It’s not a bad review–I appreciated his anecdotes about working at the Fed–but he misrepresents an example cited by Scott here about the stock market reactions at the end of 2007:

That’s when the Fed announced a disappointingly small rate cut (0.25%, from 4.50% to 4.25%). I could write a whole book on this decision, because it has vast implications for monetary theory. But let’s start with some basic data.

… The Dow Jones Industrial Average immediately plunged by almost 1.5%, and ended the day almost 2.5% below the preannouncement level. (p. 251)

Kling uses this example to accuse Scott Sumner of reasoning from a price change. That isn’t fair because in that chapter– and in the chapter on Japan– Scott lays out comprehensive arguments about how central banks that ignore data from markets can create years of misery. The stock market movements were part of a shift in several other declining indicators for the economy that the Fed ignored while it was doing hand-wringing over inflation. Kling clearly doesn’t remember the tight money regime that led to high unemployment, underinvestment, and a loss of credibility for monetary policy.

Currently, Kling is one of the economists who is worried that Fed actions will lead to a repeat of the 1970’s. He seems dismissive of an NGDP growth forecast (granted, that’s Hypermind, which may just be a group of idiots) for 2022 that’s HALF of what it usually was during that decade. We’ll see who is right in a year, and for the rest of the week we’ll see if the taper announcement crashes stock markets.

Comments are closed.