Ludwig Wittgenstein pointed out that many words don’t have a simple precise meaning, but instead refer to a set of concepts with a sort of family resemblance. I thought of this when reading a twitter exchange, which was triggered by a recent post I did over at TheMoneyIllusion:

There are a number of different ways that one could address this question. For simplicity, I’ll focus on a fiat money system, as I’d probably define monetary policy slightly differently under a gold standard.

Monetary policy occurs:

1. When a monetary authority . . .

2. uses a set of monetary policy tools . . .

3. or signals intentions to make future use of policy tools . . .

4. to impact the supply and/or demand for the medium of account, . . .

5. which impacts nominal aggregates such as the price level and NGDP.

Later I’ll return to the question of whether only actions by the monetary authority (such as a central bank) should count. For now, let’s look at the other parts of my definition.

In the US, the monetary base (cash plus reserves) is the medium of account. The Fed has traditionally had three policy tools that impact base supply and demand, but those tools have changed over time:

Policies affecting the supply of base money: Open market operations and loans to banks.

Policies affecting the demand for base money: Reserve requirements and interest on reserves (IOR).

That’s four tools, but prior to 2008 IOR did not exist and today reserve requirements do not exist. So mostly three tools. Basically, the Fed adjusts the supply of base money by the purchase and sale of assets, as well as loans of base money. Demand is impacted via changes in IOR. More supply of base money is expansionary, ceteris paribus, and more base demand is contractionary. But, and this is important, policy is not necessarily expansionary when the base is increasing, and it’s not necessarily contractionary when higher IOR is tending to increase base demand. Lots of other things matter, by far the most important of which is signals about the future path of policy, that is, the future use of the three major policy tools.

You could make an argument that monetary policy should refer not just to actions taken by the monetary authority that impact the supply and demand for base money, but also to any other action that impacts the purchasing power of money. Thus, suppose Bill Gates were to shift $50 billion of his wealth from stocks to US currency placed in safe deposit boxes? That increases the demand for base money, doesn’t it? Why not consider his action to be monetary policy?

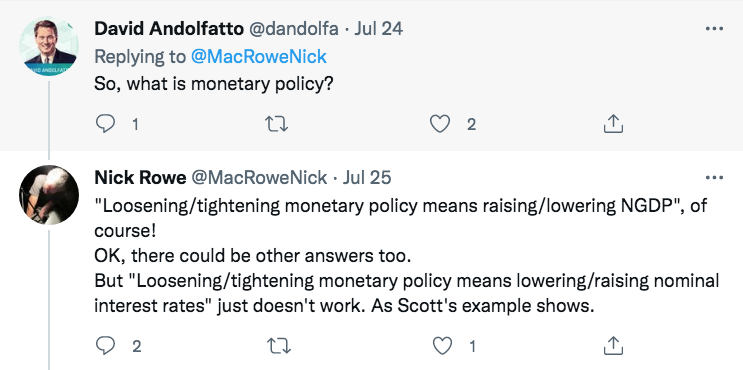

David Andolfatto makes a related point in response to Nick Rowe:

I can give you two reasons why I don’t think it’s useful to expand the definition of monetary policy beyond the monetary authority:

1. The behavior of the monetary authority is a very important part of government policymaking. It is useful to have a term that applies to monetary actions taken by this specific institution, and have other terms (currency hoarding, fiscal policy, etc.) for actions taken by other entities that might impact the value of money.

2. As a practical matter, I don’t think that currency hoarding by Bill Gates would impact the value of the dollar. I suspect that the Fed would respond by injecting enough extra base money to offset the effect that Gates’ action might otherwise have on the value of money. In the same way, I suspect that the Fed would roughly offset the effect of more fiscal spending on prices and nominal spending. And if it didn’t, I’d still call that passivity an “expansionary monetary policy”. (A good example is the Fed’s expansionary policy during 2021, which was discretionary, not forced by fiscal policy.)

I do not believe this monetary offset argument applies in countries like Zimbabwe. But even in those cases (of fiscal dominance), the first reason I provided is sufficient for having a special term to designate policies of the monetary authority that impact the supply and demand for base money. I’d prefer to call deficit spending in Zimbabwe “fiscal policy”, while acknowledging that it would likely impact inflation.

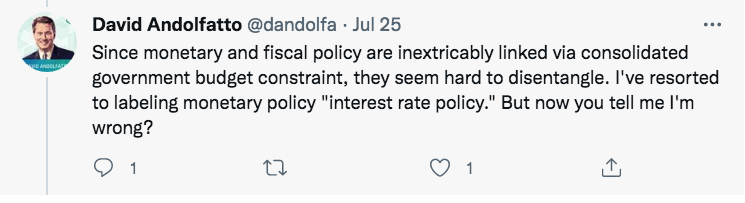

PS. Here’s another tweet by Andolfatto:

I’m not sure how much weight anyone puts on my views, but I will say that Milton Friedman would have certainly viewed that definition as being wrong. (Although I suppose it could technically be correct if one were to define monetary policy as policy affecting both the path of interest rates and the path of the natural interest rate.)

READER COMMENTS

Kevin Erdmann

Jul 27 2022 at 12:21am

Read practically any social media thread, talk to just about any uncle who dabbles in the market, or even attend a mixer of registered financial advisors, and you are likely to hear stressful conversations about how to invest that are based on some vague and ever-present notion that “monetary policy is interest rate policy”. It will include some idea that rates are perpetually too low, which induces households and corporations to take on too much debt. All that artificially subsidized debt leads us constantly to overconsume, and puts us at risk of financial crisis at any moment. It means that the price of stocks and homes are always artificially too high except for during temporary bouts of crisis. And a combination of covering for the oversized federal debt or avoiding the inevitable recession means that the Fed keeps doubling down on an unsustainable path.

That stress and all of the suboptimal and fear induced financial decisions it leads to all come from the convention of central bankers to communicate that “monetary policy is interest rate policy” and I think it has been an emotional and financial poison.

Scott Sumner

Jul 27 2022 at 12:32pm

Good points.

vince

Jul 27 2022 at 2:11pm

Right, and Andolfatti succinctly defines contemporary monetary policy. All the talk about the Fed’s dual mandate ignores the third mandate: moderate long-term interest rates? Not high, not low. Moderate.

Scott Sumner

Jul 27 2022 at 7:24pm

I recently did a paper (in Cato) arguing that the third mandate should be taken seriously.

Lizard Man

Jul 28 2022 at 9:44am

Is there a correlation between low interest rates and accounting/securities fraud? Does an environment with low rates encourage investment in Ponzi schemes? I don’t know the answer to those questions, but it is a theory that I have read before about why interest rates can be “too low” and destabilize an economy. It does seem to me that a lot of startups are difficult to distinguish from Ponzi schemes, but I don’t know if the funding of so many dubious startups is about low interest rates or about the beliefs of folks in Silicon Valley.

Scott Sumner

Jul 28 2022 at 1:51pm

Are you referring to real or nominal interest rates? (I suspect that interest rates have little effect on Ponzi schemes.)

Spencer Bradley Hall

Jul 27 2022 at 10:40am

The economic definition of base money (money multiplier) is wrong. Under our managed system it is impossible for the public to add to the total money supply consequent to increasing its holdings of currency. And the trend of currency has been up since 1930. An increase in the currency component is contractionary, unless offset by FED credit (as it always has been).

Unfortunately, the only tool, credit control device, at the disposal of the monetary authority in a free capitalistic system through which the volume of money can be properly controlled is legal reserves. Powell eliminated legal reserves in March 2020.

Daniel L. Thornton, May 12, 2022 agrees with me:

“However, on March 26, 2020, the Board of Governors reduced the reserve requirement on checkable deposits to zero. This action ended the Fed’s ability to control M1. In February 2021 the Board redefined M1 so that M1 and M2 are very nearly identical. Consequently, it makes little sense to distinguish between them. In any event, the checkable deposit portion of M2 cannot be controlled now because there are no longer reserve requirements on these deposits. Here is the reason the Fed cannot control these deposits.”

https://www.dlthornton.com/images/services/Some%20Thoughts%20About%20Inflation%20and%20the%20Feds%20Ability%20%20to%20Control%20It.pdf

Spencer Bradley Hall

Jul 27 2022 at 10:46am

The FED no longer has the “tools” to control N-gDp. The money supply can never be properly managed by any attempt to control the cost of credit. Interest is the price of credit. The price of money is the reciprocal of the price level.

The effect of the FED’s operations on interest rates is indirect, varies widely over time, and in magnitude. What the net expansion of money will be, as a consequence of a given injection of additional reserves, nobody knows until long after the fact.

The consequence is a delayed, remote, and approximate control over the lending and money-creating capacity of the payment’s system.

Don Geddis

Jul 27 2022 at 4:51pm

No, because interest rates — the price of credit — is not a major part of the monetary policy transmission mechanism. The primary monetary policy transmission mechanism (after expectations, of course) is the Hot Potato Effect. Which doesn’t rely on the bank lending channel at all. It doesn’t matter what happens to interest rates. (This is why Quantitative Easing works, while ignoring any interest rate effects.)

The Fed’s control of the quantity of the monetary base is all the “tool” that it needs in order to successfully target any nominal aggregate (including NGDP or inflation). This would be true even in an economy with no commercial banks and no bank lending at all.

Spencer Bradley Hall

Jul 28 2022 at 11:14am

LSAPs in conjunction with the remuneration of interbank demand deposits is less than optimal. First, as George Selgin pointed out, paying interest on reserves at a higher rate than money market rates induces nonbank disintermediation (an outflow of funds or negative cash flow). And the nonbanks are the economic generators. The welfare of the banks is determined by the welfare of the nonbanks. The Gurley-Shaw thesis is nonsense.

Second, the FRB-NY trading desk’s money multiplier, the ratio of bank vs. nonbank purchases is unknown.

Unlike Treasury issuance, because the belligerent bifurcation (the mis-aligned distribution of sales and purchases of debt by the FRB-NY’s trading desk and its customers/counter-parties is largely unpredictable, so too now is the volume and rate of expansion in the money stock. FOMC policy has now been capriciously undermined – by turning non-earning excess reserve balances into bank earning assets.

This is in direct contrast to targeting: *RPDs* (reserves for private nonbank deposits), as Paul Meek’s (FRB-NY assistant V.P. of OMOs and Treasury issues), described in his 3rd edition of “Open Market Operations” published in 1974.

This adds up to an obdurate apparatus that the Fed cannot monitor, much less control, even on a month-to-month basis. What the net expansion of the money stock will be, as a consequence of any given addition or subtraction in Federal Reserve Bank credit, nobody can forecast until long after the fact.

Michael Rulle

Jul 27 2022 at 11:39am

It is the above description that I have always understood once I first read your concept of the supply and demand for money and monetary offset. It also felt consistent with Friedman, who may have written (?) in a less complex time for monetary policy.

The last few days I have been googling about monetarism, and unless I insert the phrase “market monetarism” virtually the only name that appears is Friedman. Re.MM you appear most and are sometimes damned with faint praise by some because these ideas first appeared in a “blog” and at Bentley

YET —-one also reads that Bernanke explicitly discussed NGDP targeting —-I believe even futures too

I think it is fair to say that the Fed can never perceive in real time, but they can see in recent past and state that they will adjust. The major problem with Powell is it is very hard to understand what he believes. Today’s market belief is that he will “tighten” (raise Fed Funds rate aggressively) thus having the ability to “ease” (lower Fed Funds rate) earlier than if he did not tighten aggressively. That thought process is dominant.

After the FAIT fiasco I have no idea what Powell will do. Yet there still seems to be a belief that inflation will fall based on I-rate thinking

It still confuses me

Spencer Bradley Hall

Jul 27 2022 at 11:46am

I started using required reserves as the money multiplier (base money) after the 1979 money supply errors. That’s when a surge in the money stock sent stocks reeling.

“Last week the Fed announced that a massive $3.7 billion mistake had been made in the weeks ending Oct. 3 and 10 because of faulty numbers submitted by Manufacturers Hanover Trust Co. of New York. Yesterday, the Fed revealed that the same bank had since made an $800 million mistake. Both errors were on the high side.”

Spencer Bradley Hall

Jul 27 2022 at 11:48am

Link: “Bank Reserves And Loans: The Fed Is Pushing On A String” by Charles Hugh Smith

Bank Reserves and Loans: The Fed is Pushing On a String – InvestingChannel

Don Geddis

Jul 27 2022 at 4:59pm

And that article also makes the mistake of equating monetary stimulus with increased bank lending. And falsely claiming that monetary stimulus is “pushing on a string” if bank customers are “not interested in borrowing”.

The correction is easy: the transmission mechanism for monetary stimulus does not run through increased bank lending. All the data and charts in that article are completely irrelevant. They simply don’t matter.

Spencer Bradley Hall

Jul 28 2022 at 9:14am

The point was that required reserves, regardless of the increasing multiplier, reflected monetary policy period. Required reserves demonstrated fixed monetary lags.

Iskander

Jul 27 2022 at 4:44pm

Scott, can fiscal policy have a permanent impact on nominal aggregates (except through its impact on aggregate supply)?

Raising government expenditure today relative to its trend might raise (both real and nominal) interest rates, and therefore the price level via its effect on the opportunity costs of holding money but this is by definition a temporary effect (I guess that a permanent expansion would be neutralized by consumption smoothing/PIH, but this is speculation) . By contrast, raising the price level through monetary expansion can easily be permanent and comes with a much lower opportunity cost.

Scott Sumner

Jul 27 2022 at 7:27pm

I suspect that any effect would be offset by monetary policy. If not, then permanent fiscal stimulus results in a one-time increase in P and NGDP, but not their long run growth rate.

Comments are closed.