There are several different theories of what determines growth in manufacturing employment. Officials for the Trump administration emphasize the role of trade imbalances, whereas I would argue that real economic growth is the most important factor. The past two years provide an interesting test of these two hypothesis, as job growth has accelerated at the same time that the trade balance in goods have gotten considerably “worse”, i.e. more negative.

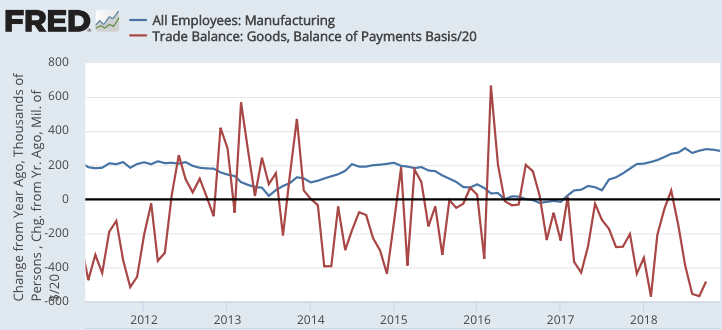

The following graph shows 12 month changes in manufacturing employment (blue line) as well as changes in the trade balance for goods (red line):

Clearly the trade data is a bit noisy, but you can see that in the past year the trade deficit has been getting larger (more negative) at the same time that growth in manufacturing employment has accelerated. Manufacturing employment is a procyclical variable, rising and falling with overall economic growth, whereas the trade balance tends to be countercyclical, falling during booms and “improving” during recessions. (Of course this “improvement” isn’t actually a good sign, but it’s often interpreted that way.

Just to be clear, I’m not claiming that trade deficits have no impact on manufacturing employment. If one hold growth constant, then a bigger trade deficit probably reduces manufacturing employment somewhat. Rather my claim is that the effects of trade are small in comparison to the effects of aggregate growth.

Unfortunately, this point is not well understood. The Financial Times reports that Trump administration officials are viewing the recent growth in manufacturing employment as a sign that their trade policies are working.

Figure of the week: 284,000

The number of manufacturing jobs created in the US last year, which the US trade representative touted on Friday as the biggest increase in 21 years and evidence that the administration’s trade policies were working.

Their argument for protectionism, however, was based on the claim that manufacturing jobs could be created here if we reduced the trade deficit. Instead, Trump policies such as the corporate tax cut have boosted the trade deficit. Indeed even our trade deficit with China has increased.

Actually, it’s possible that Trump policies have played some role in the creation of manufacturing jobs (although it’s hard to be certain about these things.) But if the policies have worked, it’s more likely that a combination of corporate tax cuts, deregulation, and easier money (faster NGDP growth) have produced more jobs, not trade barriers. For every steel job saved via tariffs, several jobs are lost in steel consuming manufacturing industries.

If the term ‘trade’ were removed from the FT quote above, the claim would become defensible. As it is, the claim is quite dubious.

READER COMMENTS

Auguste Gusteau

Jan 13 2019 at 2:06pm

If one hold growth constant, then a bigger trade deficit probably reduces manufacturing employment somewhat.

Surely this is reasoning from a trade deficit change. 😉

Jon Murphy

Jan 13 2019 at 2:33pm

Just for fun, I ran a quick correlation between the full data for the above two series: -0.45 and it is statistically significant.

I disagree. I think the reason for the trade deficit would matter. If, for example, the imports are compliments (or inputs) for domestic manufacturing, a trade deficit would probably have a positive effect on manufacturing employment.

Warren Platts

Jan 15 2019 at 12:48am

Hmm. So a grand total of about 20% of the variation is thus explained…

That is hard to believe. That would require a very strange model: the reduction in price gained by losing jobs manufacturing intermediate inputs would somehow be great enough to justify even more jobs doing final assembly. Not saying it is logically impossible. But to show the probability, some more explanation would be desirable…

Jon Murphy

Jan 15 2019 at 1:28pm

I’m not sure I’d call the Law of Demand “a very strange model,” but hey, preferences are subjective.

Warren Platts

Jan 16 2019 at 12:18pm

It depends. For a developing country, importing capital and high-tech intermediate goods while running a trade deficit might boost manufacturing employment, as it did for the United States for most of the 19th century.

But now, in the 21st century, the imported inputs would likely be labor intensive products, and would thus replace labor intensive factories here. More productive capital-intensive factories might see some employment growth due to the cheaper inputs, but overall manufacturing numbers would go down. Indeed that would happen even if trade was balanced.

“Efficiency” might be increased, but income inequality would also rise, pushing up savings while pushing down consumption among the working class, thus driving down overall aggregate demand. The excess savings exacerbated by the capital surplus would be wasted on unproductive investments. Overall economic growth rates would likely slow.

Jon Murphy

Jan 16 2019 at 1:01pm

Ok. Irrelevant to my point, though. Stay on topic.

Warren Platts

Jan 16 2019 at 2:32pm

Huh? The law of demand is exactly what I’m talking about. Lower priced imports will allow a lower priced finished good, and that lower price will then allow more of those goods to be sold. Since more finished goods will be sold, more workers in the finished goods industry will need to be hired. I get that.

On the other hand, as you note, import competition among manufactured intermediate goods will lower employment in input goods. Right?

The question is whether the gain in making finished goods outweighs the job losses making intermediate goods.

To make that claim, that overall manufacturing jobs would go up requires a rather strange model–at least for 21st century United States. As I said above, import competition tends to fall heaviest on more labor-intensive manufacturing. Meanwhile, if the finished goods maker is hiring more thanks to cheap imports, then they obviously are not suffering much import competition. That in turn entails they must be a capital-intensive, highly productive business.

Do you see?

If the relative productivity in the inputted goods and finished goods sectors was about the same, the subtraction from the intermediate goods sector would about equal the gain in the finished goods sector, other things being equal.

If the finished goods sector was less productive than the intermediate goods sector, then we should expect an increase in overall employment. The loss in the intermediate goods sector will be more than outweighed by the gain in the finished goods sector. This model will work for a place like China: they get high-tech chips from USA and Taiwan and Japan, and assemble them by hand in China. But that is a rather strange model for the USA.

In the USA, for a loss in employment in a less productive intermediate goods sector because of cheap imports to cause even more jobs to be hired in the more productive finished goods sector would require some sort of what seems to me to be a rather strange, nonlinear response. That is, the reduction in price of the intermediate good (and hence subsequent reduction in the price of the finished good) must not only increase the quantity demanded of the finished good, but also cause a shift in demand as well (i.e, the demand curve must move to the right).

But why should we expect that to happen?

There is one way: exports. But your point, Jon, was specifically about what happens under a trade deficit. Somehow domestic demand itself–not just quantity demanded–would have to increase. It is hard to think of what such a channel would look like. Do people’s tastes change just because there has been job losses in a particular sector? But please feel free to elaborate on what such a channel might be like.

If the USA was running a massive trade surplus like Germany, then I can see more jobs being created in the highly productive finished goods sector than would be lost in the less productive intermediate goods sector. The highly productive labor force would then have a market of 7 billion people to sell to.

Benjamin Cole

Jan 13 2019 at 7:18pm

When US trained economists discuss regional economics within the US, they are well aware of the role of manufacturing in creating a plethora of related jobs in administration, transportation, warehousing and so on, and, most importantly, in bringing income into the region.

A region within the US cannot borrow its way to prosperity.

Somehow, when we move into national economies, this understanding of a regional economy is lost.

Though it moves into the tainted realm of behavioral economics, most economists also understand the “clustering” of skills and industry as well.

Free-trade theologies and the development of economies are two topics that mix like oil and water.

Mark

Jan 13 2019 at 10:13pm

Looking at regions within the US, it becomes obvious that manufacturing is neither necessary or sufficient for a prosperous economy.

The ten states with the highest median household income are Maryland, New Jersey, Hawaii, Massachusetts, Connecticut, New Hampshire, Alaska, California, Virginia, and Washington. All 10 of these states have less than the national average of 12% of GDP being manufacturing.

On the other hand, the ten states with the lowest median household income are West Virginia, Mississippi, Arkansas, Louisiana, New Mexico, Alabama, Kentucky, Oklahoma, South Carolina, and Tennessee. 7 out of these 10 states have more than 12% of GDP in manufacturing.

Manufacturing is one potential avenue to prosperity, but many times a person’s or region’s comparative advantage will point elsewhere. The most economically productive and prosperous parts of the US are not the parts with the most manufacturing. And it’s only trivially true that manufacturing adds supporting jobs and brings in income, because all industries add supporting jobs and bring in income.

Thaomas

Jan 14 2019 at 3:40am

Our current fiscal policy of high deficits with relatively tight monetary policy = “strong” dollar, is a formula for higher trade deficits in manufactures.

ChrisA

Jan 15 2019 at 12:13am

Considering the wide latitude in how jobs are classified any arguments based on data of growth in manufacturing jobs is pretty silly. For instance a design engineer in a consultancy is classified as doing service work, but if he were employed by a manufacturing company then he would be classified under manufacturing, even if in both cases he did exactly the same work. Nowadays it is very common for companies to have their high paid design and higher end work in one country and the low end jobs assembly jobs in another country. Proponents of manufacturing jobs would argue this is a bad thing – which is silly. On a personal level what job would you rather be doing?

Warren Platts

Jan 15 2019 at 12:57am

Whenever I see something marked “Designed in USA; Made in China”, I wince. There is no substitute for not having the engineers next to the factory floor.

As for the desirability of being a factory worker versus an engineer, that depends on personal comparative advantage, does it not?

In my opinion, we should not sell short the working class of the United States. They constitute the majority of the electorate, and they are responsible for much of the aggregate demand that drives the entire economy. Instead of trying to cut them off at the knees, we should be seeking policies that will boost their wages. And no, I am not talking about minimum wage increases. I am talking about managing for a tight labor market.

ChrisA

Jan 15 2019 at 12:59pm

Warren – I am an engineer and I would say that knowledge of a manufacturing process is important but you don’t need to located all the time next to the factory floor to get that knowledge. That is a pretty silly idea to be frank – clearly large scale manufacturing is all about doing the same thing over and over again – what would you learn after you had seen it a few times?. Also I don’t see what comparative advantages have to do with preferences – I might have comparative advantage as a coal miner but I might prefer to be a chef as an example as more interesting work. I see this nostalgia for manufacturing all the time, vs service industry jobs. It is a strange thing – when you think about rows of people all doing the same thing for hours on end you wonder anyone could prefer them to a service job where there tends to be more variety, personal contact and less physical labor. In addition basic manufacturing jobs are the most easiest copied by overseas companies, so unless you are investing all the time in productivity (again causing constant job losses), you are locked into a spiral of lowering wages to remain competitive.

Jon Murphy

Jan 15 2019 at 1:25pm

Opportunity costs, not preferences, determine comparative advantage. And opportunity costs depend on real, as opposed to imaginary, alternatives.

Warren Platts

Jan 15 2019 at 12:34am

Let us be clear: that is your theoretical prediction. The empirical facts so far belie your prediction. Jobs in steel consuming manufacturing industries are up way more than the steel producing jobs. There is zero evidence (so far) that the tariffs are reducing employment in steel consuming manufacturing industries.

Scott Sumner

Jan 15 2019 at 1:35pm

Warren, No, it’s not a prediction, it’s an estimate. And no, the empirical facts do not “belie” my estimate, for reasons that are clearly explained in this post. If you think the post is wrong (as it may be), then please explain why.

Warren Platts

Jan 16 2019 at 1:30pm

I pretty much agree with most of your post, sir. (As for the trade deficit getting bigger, that imo is probably more of a function of (a) exporters front-running the tariffs, which is a common historical pattern; and (b) as long as the USA is a safe haven for parking excess savings from abroad, we are still going to have a trade deficit, no matter how much we raise tariffs, within reason.)

I was objecting to the specific estimate that for every steel job saved, several more jobs in steel consuming industries will be lost. My evidence is the latest jobs report put out by the BLS. Yes, steel jobs are up–as expected because of the steel tariffs–but steel consuming jobs are up way more in sectors that are consumers of steel, such as fabricated metal products (+7K), transportation equipment (+4K), machinery (+3K), heavy and civil engineering construction (+16K).

https://www.bls.gov/news.release/empsit.t17.htm

Yes, correlation does not imply causation; there are a lot of things going on at once. But if it really is the case that the steel tariffs are costing jobs in steel consuming industries, that is not obvious in the data so far.

I suppose you could counter that the strong economy is masking the effect of the steel tariffs. After all, you say the strength of the economy is stronger than effects caused by trade and the trade deficit. Fair enough.

On the other hand, one could argue that Trump’s twin policies of restricting immigration combined with tariffs on many imports is having the desired effect of tightening the labor market, thus giving the working class a much needed raise. Putting more cash in workers’ pockets spurs aggregate demand because they spend their wages on consumption rather than unproductive investments.

Meanwhile, it sure seems that much of proceeds from Trump’s corporate tax cuts are going into relatively unproductive stock buybacks, rather than purchases of more U.S. goods and services. For those two reasons, a protectionist can say that jobs in steel consuming industries are increasing not in spite of Trump’s tariffs, but because of Trump’s tariffs.

Comments are closed.