In a recent post, I discussed two widely held views that seem inconsistent. I am indebted to Ryan Bourne for pointing to another example.

Unemployment in Western Europe was quite low during the 1960s. During the 1980s, unemployment rose to very high levels, and never fell back again, even after their economies had recovered from the two oil shock recessions. This led to theories of “hysteresis”, the idea that a severe slump could cause permanently high unemployment, as workers who were unemployed for long periods became less employable. The policy implication is that it is especially important to have demand stimulus during recessions, to prevent a permanent rise in unemployment.

This argument was used for aggressive stimulus during the Great Recession. Today, we see almost the opposite argument. Despite the unusual length and depth of the Great Recession, many pundits claim that the natural rate of unemployment in the US and in many other developed countries has fallen to historically low levels. This is cited as justification for additional monetary stimulus.

I fear that people will misinterpret this post. I don’t believe these arguments are necessarily wrong. Long time readers know that I favored additional monetary stimulus during the Great Recession. I also agree with the claim that the natural rate of unemployment has recently declined in the US and some other nations.

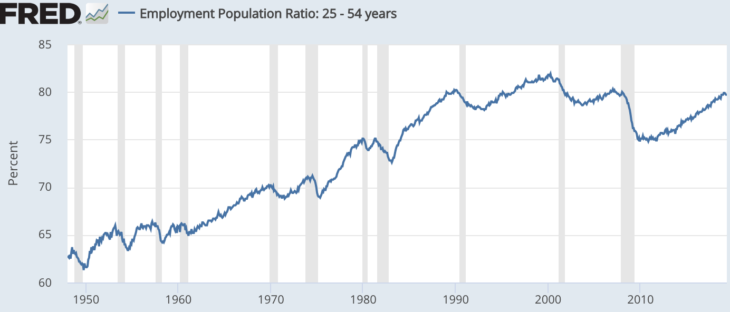

But it is important to be consistent. The recent trends in unemployment cast doubt on the hysteresis theory. It does not seem like the Great Recession permanently damaged the US labor market. If you prefer another labor market measure, such as the employment ratio for prime age workers, that’s also back to pre-recession levels:

READER COMMENTS

Michael Sandifer

Jul 5 2019 at 12:09pm

Scott,

Yes, but the current figure is still almost 2 points below the 90s high, and ECI growth is still weak in this context, despite some recent strengthening.

If I’m right about the neutral interest rate equaling potential real GDP + inflation at monetary equilibrium, then the Fed Funds rate should be lowered close to zero again and we should gain around 250 basis points on the long end of the yield curve, assuming sufficient confidence in the Fed’s actions and regime. Then, some combination of unemployment reaching below 2% and real GDP growth reaching 5.5% should occur. That 5.5% would likely not be sustainable, but would be a temporary catch up rate, after which real GDP growth potential would average about 3.5%.

Yes, it’s heresy to think there’s still some potential to get closer to the previous RGDP growth trend line, but I think the nature of the Fed reaction function continues to put a lid on AD, including investment and resulting productivity.

I also think there’s a circular relationship between real GDP growth/capita and population growth, both in terms of family size and immigration. Yes, our population growth would be slowing anyway, but not as dramatically as it has.

Why can we still grow at 3.5%, sustainably. Technology and at least slightly increased population growth.

I don’t worry that the in employment rate has never been so low in the US. As I see it, the Fed has always done some combination of cutting recoveries short with tight money, or throttling real growth potential with too much inflation. I don’t think we truly know what we’re capable of, empirically.

Scott Sumner

Jul 5 2019 at 12:29pm

Michael, You said:

“Yes, but the current figure is still almost 2 points below the 90s high, and ECI growth is still weak in this context, despite some recent strengthening.”

That actually supports my argument. The ratio fell after the weak 2001 recession, but did not fall after the major 2008-09 recession. The hysteresis theory would predict the exact opposite

Michael Sandifer

Jul 5 2019 at 12:18pm

And before anyone mentions the 70s, I favor a 5% NGDP level target. Little to lose here, prescriptively.

Brian Donohue

Jul 5 2019 at 12:35pm

The last decade is a compelling counterpoint to hysteresis theory.

But this:

“Despite the unusual length and depth of the Great Recession, many pundits claim that the natural rate of unemployment in the US and in many other developed countries has fallen to historically low levels.”

Who’s making this argument? A less strawmanny argument might be:

Labor market metrics are way fuzzier than they used to be, particularly at 55-70, which is a growing segment of the population. LFPR and various U rates are still helpful, but more reliance should be put on wage growth particularly as a labor market indicator. Wage growth was pretty anemic for most of the recovery, somewhat higher more recently, but nothing that looks close to overheating. If real wages do rise, it may induce yet more of the “voluntary old people” workforce back in.

Scott Sumner

Jul 5 2019 at 7:35pm

Brian, It’s not a “straw man” argument if I correctly point out that lots of economists are making it. Not sure what your point is. You are claiming that the labor market is not overheating, which is also the implication of my “straw man” argument that the natural rate of unemployment has fallen. Perhaps I’m missing your point.

Robert EV

Jul 8 2019 at 1:14am

This is the sort of question that needs a more thorough analysis than an employment graph.

I have questions on suicide rates and overall mortality among the relevant demographics (particularly recently in the US).

Questions on credentialism during the 60s-80s in Western Europe.

Questions on external stimuli rates (Marshall plan and tariffs) during the relevant time periods in Western Europe.

Questions on population movement (or lack thereof) during the relevant time periods.

Comments are closed.