Back in the late 1970s, economists began exploring the “time inconsistency problem” in monetary policy. In the long run, we are better off if central bankers maintain a low inflation rate (or NGDP growth rate.) But in the short run, the economy may do better with a more expansionary policy. The negative consequences of that expansionary policy will be mostly borne by future policymakers.

It turns out that the time inconsistency problem in central banking is somewhat overrated. Central banks often succeed in keeping inflation low for long periods of time (but not recently.)

In fact, the time inconsistency problem is far worse for banking regulation. Political and economic managers like President Biden, Janet Yellen, and Jay Powell would very strongly prefer that a financial crisis not occur on their watch.

There’s a common but understandable misconception that there is a sort of tradeoff involving financial stability and moral hazard. People assume that we can have financial stability with moral hazard, or we can have financial instability with a regime free of moral hazard. I cannot emphasize enough that this is a false assumption!

Policies that lead to moral hazard (government deposit insurance, TBTF, bailouts, etc.), cause more financial instability in the long run. There’s no trade-off to exploit here. We don’t buy a more stable financial system with bailouts. We encourage more risk taking. So then why does the federal government keep bailing out financial actors that made bad decisions?

Here’s where the time inconsistency problem comes into play. While bailouts make for a more unstable financial system by encouraging ever-greater risk taking, in the short run they do reduce financial instability. And it seems as though President Biden, Janet Yellen, Jay Powell and the other key policymakers favor steps that would make for less financial instability over the next 5 years, even if they would make for more financial instability over the next 50 years.

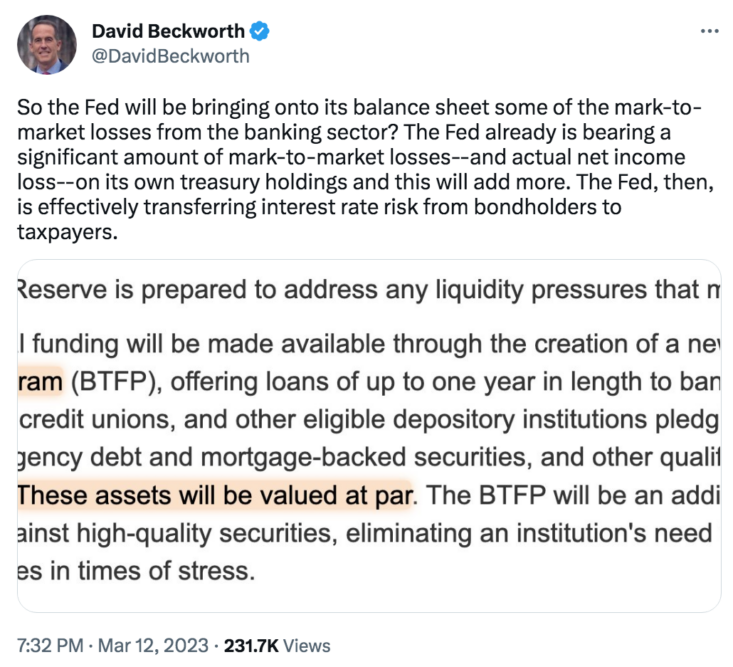

PS. While the media has focused on SVB, the much bigger outrage is the Fed’s new facility to bail out all banks that made bad decisions. You bought risky long-term bonds with short-term deposits? Don’t worry; the Fed’s got your back:

This is one of the darkest days in US financial history—a breathtaking expansion of moral hazard. Younger readers should brace themselves for much worse in the decades ahead. We are sowing the seeds of future financial crises.

PS. I highly recommend reading Peter Conti-Brown’s tweets on this affair. Here’s one example:

READER COMMENTS

vince

Mar 13 2023 at 4:10pm

The Fed has its own moral hazard problem. SVB was regulated by the Fed. If depositors lose, they would blame the Fed’s regulatory failure. The Fed can always bail its way out of its own regulatory failure.

Jose Pablo

Mar 13 2023 at 4:35pm

In fact, you could think that the FED is trying to cover its own incompetence since they were in charge of supervising SVB

An institutional design in which you have the ability to cover up your own incompetence, has not a kind of moral hazard embebded?

Jose Pablo

Mar 13 2023 at 4:43pm

This is one of the darkest days in US financial history

Indeed! … and that is a extremely tough competition to win!

nobody.really

Mar 13 2023 at 5:14pm

1: Beckworth seems to have qualified some of his earlier tweets.

2:

Is this a problem? As far as I can tell, the feds have acted to address SVB and Signature in order to stop a general run on the banks. Yes, other managers, shareholders, and bondholders can now learn from this (that is, they can exploit the PUBLIC GOOD called information) and modify their behavior prospectively. Are “bail outs” bad if there are no incremental public dollars involved?

If people go skating on thin ice and one guy breaks through, does it create a moral hazard to let other skaters learn from his experience and get off the ice?

On A Prairie Home Companion, Garrison Keillor told a story about some poor kids in Lake Woebegone who committed a crime (vandalism, I think). A cop nearly catches them, but doesn’t. Keillor later implies that the cop could have caught the kids, but concluded that the better outcome would result having the kids NEARLY get caught–and learning from the experience. Maybe someone should have given that cop a lesson on moral hazards.

Scott Sumner

Mar 13 2023 at 5:43pm

“Are “bail outs” bad if there are no incremental public dollars involved?”

Yes, as they encourage more reckless behavior. In any case, there will be public dollars involved.

vince

Mar 13 2023 at 6:08pm

What do you mean by incremental public dollars?

FDIC is a government corporation. What other insurance company would pay out more than the coverage a policyholder purchased?

nobody.really

Mar 13 2023 at 6:31pm

Imaging the feds would ensure all the deposits in SVB and Signature even if they were the only banks at risk. Now introduce the fact that other banks are at risk. The existence of these other banks adds nothing to the cost the feds will incur dealing with SVB and Signature. If the managers, shareholders, and bondholders of these other banks can learn from the example of SVB and Signature (specifically, learn that the managers, shareholders, and bondholders get wiped out) and can modify their behavior to mitigate their risk prospectively, this benefit comes at no incremental cost (indeed, probably at a savings) to government.

vince

Mar 13 2023 at 6:48pm

Depositors need to learn too. They shouldn’t expect to chase yield and then be bailed out when excess risks were taken. A depositor shouldn’t have to look at the bank’s financials, but should be aware that FDIC covers $250k, nothing more. It’s no secret, and unfortunately neither are bank failures.

nobody.really

Mar 13 2023 at 7:10pm

Fair enough; you’ve persuaded me.

But I had been discussing managers, shareholders, and bondholders. It’s less clear how the fed policy will prompt them to engage in riskier behavior….

…unless we anticipate collusion between large depositors and managers, shareholders, or bondholders. And collusion between large depositors and managers seems plausible–though this would require these managers to act contrary to the interests of shareholders and bondholders. But principal/agent problems are omnipresent. Maybe that’s a place for bank examiners to look….

Jose Pablo

Mar 13 2023 at 7:36pm

[M]anagers, shareholders, and bondholders. It’s less clear how the fed policy will prompt them to engage in riskier behavior….

Really?

Have you take a look at SVB balance sheet? the extremely risky behavior of the bank management was at plain sight for a long time.

https://johnhcochrane.blogspot.com/2023/03/silicon-valley-bank-blinders.html

SVB bondholders and shareholders have no excuse for not seeing it. And still they choose to pick this risk, why do you think they did? to better serve society?

vince

Mar 13 2023 at 8:32pm

The best answer I can give is to look into the Greenspan put. Managers and executives are different, but bonuses and incentive compensation are often based on recent deals and short term results, and can be so large those employees care much less about long term results. On the future of the company, I once worked with a general manager who openly said “who cares, we’ll all be working somewhere else in five years.”

Jose Pablo

Mar 13 2023 at 6:20pm

other managers, shareholders, and bondholders can now learn from this

Taking into account that this is far from being the first bail in US finantial history, it seems to me that they have not learned that much from past “lessons”. Why do you think this time would be different?

On the other hand you don’t need any lesson to understand the risk of duration missmatches on your balance sheet. That is a preliminary banking course (not even a 101 one).

As Scott points out, it seems more likely that the “lesson” investors do learn is that they can adjust up the risk they can take, considering the FED tendency to rescue them if things go wrong. This is an extremely valuable free put that investors learn very quickly how to benefit from.

An even worse, this “eager to learn” investors can crowd-out the more sensible and more prudent kind, and with them, the more stable system that could be, absent the wrong incentives. The cost of this distortion is, very likely, huge.

nobody.really

Mar 13 2023 at 6:54pm

Again, here’s the quote at issue:

I doubt the merits of this assertion. How does backing up SVB’s and Signature’s depositors “bail out” the managers, shareholders, and bondholders of other banks? And if it does, what harm?

If you claim that the fed policy regarding SVB and Signature will NOT benefit other banks, then you join me in doubting the merits of the assertion.

Not sure I understand who “investors” are in this context. Up to this point, we’ve been discussing bank managers, shareholders, and depositors. I don’t see how the fed’s policy “rescued” them. Rather, the fed policy rescued depositors–and specifically, people with more than $250K on deposit. And yeah, it might well skew their behavior in a more risky direction–specifically, parking more than $250K in a bank account rather than spreading it over multiple accounts in multiple banks. But depositor behavior was not the behavior addressed by the original quote (unless you’re discussing depositors who are also managers, shareholders, or bondholders?)

vince

Mar 13 2023 at 7:09pm

“How does backing up SVB’s and Signature’s depositors “bail out” the managers, shareholders, and bondholders of other banks?”

What would bank stocks have done today if the Fed hadn’t intervened? I wish I could answer, but I suspect the market would have punished them much more than the current closing prices did.

Jose Pablo

Mar 13 2023 at 7:11pm

Investors = debtholders and bondholders

[And in our banking system who is and who is not a “debtholders” is a pretty grey line (they are any number of hybrid securities). Actually, depositors are also “debtholders”. It is bad enought they are not aware they are, they just needed to look at what side of the bank balance sheet their deposit is accounted for]

To say “This intervention prevents the contagion of this problem to other banks” and to say “We are bailing out the shareholders and bondholders (and not interest bearing debt holders, aka depositors) of other banks” is to say EXACTLY the same as Peter-Conti Brown correctly points out.

Scott Sumner

Mar 13 2023 at 11:31pm

“How does backing up SVB’s and Signature’s depositors “bail out” the managers, shareholders, and bondholders of other banks?”

I’d make two observations:

Depositors at other banks are clearly going to be covered as well.

The Fed’s new loan facility will allow bank bond assets to be valued at par value when used as collateral. That’s a huge benefit in a depressed bond market.

nobody.really

Mar 14 2023 at 1:56pm

Yeah, that looks fishy to me, too. Wisely or not, the the Financial Accounting Standards Board does not require mark-to-market accounting, but rather allows for asset valuations to be based on a price that an asset would receive in an orderly market rather than a forced liquidation. In this case, however, the long-term bonds in SVB’s portfolio arguably WOULD command a price lower than par value even in an orderly market, because interest rates have increased. So I don’t get this.

That said, because federal bonds trade freely, I surmise that this policy bolsters the value of federal bonds generally, not merely bonds held by banks.

nobody.really

Mar 14 2023 at 1:41pm

Pablo, Sumner, and vince each make the argument that federal policy regarding SVB will tend to bolster the stock price of other banks. They neglect to follow up by explaining what harm results.

Moreover, WHY would a policy of backstopping deposits cause bank stocks to rise (inappropriately)?

Theory 1: This federal policy shields well-managed banks from public panic. With this protection, shareholders/bondholders are free to evaluate the extent to which the bank will generate revenues exceeding costs, subject to all the other risks that businesses face. If this theory holds, then yay! Policy worked as intended.

Theory 2: Federal policy shields badly-managed/high-risk banks from public panic. Admittedly, this is (arguably) not the goal of public policy. But is public panic a useful tool for culling badly-managed banks? Is it a necessary tool?

As other commenters noted, public policy did not really conceal SVB’s investment risks, nor did it keep SVB’s stock price from falling. If public policy does not shield shareholders and bondholders from the risk of their stock price falling or their own bank failing, why shouldn’t that risk suffice to discipline these investors?

Below, I argue for the merits for recognizing that banks are businesses and are prone to close much as any other business does. Markets discipline business typically through the mundane process of generating revenues that are insufficient to cover expenses. If we never observe “a run on the hardware store,” we don’t thereby conclude that market forces are failing to discipline hardware stores. Why should we require bank runs to discipline banks?

vince

Mar 14 2023 at 3:29pm

If all the goods in a hardware store were consigned to it by customers, we *would* see runs on them.

nobody.really

Mar 14 2023 at 4:36pm

Right. But they aren’t, and we don’t–yet we still believe that market forces are sufficient to discipline shareholders and bondholders of hardware stores. If the FDIC backs 100% of deposits, then the risk of running a bank starts to look more like the risk of running a hardware store. Can we have the same faith that markets would discipline a bank’s shareholders and bondholders as we have regarding a hardware store’s shareholders and bondholders?

Perhaps this is the problem: If the bank makes risky bets and wins, shareholders/bondholders may pocket 100% of the winnings. If they make risky bets and lose, they get wiped out–but a portion of their loss gets socialized through the FDIC. As I understand it, historically this hasn’t cost very much because bank regulators have generally found other institutions to buy up the assets of the failed bank. In any event, I have to suspect that there are other ways to discipline this kind of risk-shifting than relying on bank panics. But maybe not…?

nobody.really

Mar 13 2023 at 9:10pm

Thanks for the Money & Banking class from Pablo, Sumner, and vince; I give them *****. (Cochrane goes into detail about the specific problems of SVB–it’s long-term bond investments, uninsured “hot” depositors, and neglectful bank examiners–but I’m less focused on those specifics.) With the benefit of your (and others’) tutelage, here’s the picture that I’m developing:

The division between various financial institutions (“banks”) and investment funds is … less distinct than might appear. Certain banks run abnormally high risks and offer abnormally high returns to shareholders, bondholders, and especially depositors. Arguably, consumers should celebrate having a diversity of banking/investment opportunities. But in this scenario, we should also expect high-risk banks to fail more often than lower-risk banks, and expect those who stood to win big to also stand to lose big.

However, panic can ensue when people do not recognize that the failure of these high-risk banks does not reflect badly on the rest of the banking/investment sector. Arguably, the failures of not-too-big-to-fail banks provide opportunities for the public to see that bank failures, like other business failures, are normal and should be expected, and they pose little threat to the larger economy. If we had let the chips fall where they may, endured the panic, and let it subside, appropriate lessons could have been learned by investors and the public.

Instead, government intervenes to feed the public’s Norman Rockwell image of banks as supernaturally stable institutions. This may have political benefits in the short-run but can only result in inappropriate risk-taking and greater disillusionment in the long run. This dynamic reflects an externality, wherein the decisions of a current generation of government agents will permit them to reap a benefit now and transfer the cost to a future generation.

I was operating under the assumption that government should strive to limit contagion. A contrary view holds that contagion has natural and beneficial effects of disciplining risk-takers. This all seems quite rational. But given that panics are notoriously irrational and tend to over-shoot their objectives, I still appreciate the urge to manage them.

So we face a trade-off: The risk that government will yield to the temptation to over-dampen reaction to bank failure vs. the risk that unmanaged panics will cause otherwise healthy banks to fail, and prompt all the remaining banks to adopt hyper-risk-averse postures in anticipation of the next panic. Neither option is costless; there are no “free lunches” either way.

Have I developed an appropriate understanding?

robc

Mar 14 2023 at 9:33am

Based on the former, the answer to the latter is No.

Henri Hein

Mar 14 2023 at 1:46pm

I don’t claim to understand the situation any better than you, but for what it’s worth, your summary made sense to me. One thing that is sub-optimal with the bailouts in the various forms is that the creditors and depositors are not expected to take a haircut. If we do take the “short term stability and after us, the flood” approach, at least reimburse on something like 80 cents to the dollar. That would provide some stability while sending a signal that investors should not want the bailout to be their salvation.

nobody.really

Mar 14 2023 at 2:25pm

Thanks.

But to be clear, creditors (in the form of bondholders) as well as shareholders do not merely face a haircut–they face decapitation. (Decapitalization?) They get wiped out completely, recovering nothing.

It is unclear to me why people argue that this risk is not suffice to discipline the market.

Jose Pablo

Mar 14 2023 at 3:04pm

Because the “risk” is way less that it would be absent the (expected) monetary authority intervention.

It is well known that if you put out quickly every small fire (this banks were supposed to be “small fires”!!), you end up making the forest more prone to devastating big fires.

Note that even with this “fire management policy”, you still get some areas burned … but way less than required for the long term health of the forest.

nobody.really

Mar 14 2023 at 4:01pm

Yup, government insuring deposits results in lower risk of bank runs, at least for the present. But that may leave depositors unprepared when the level of bank runs reaches the point that the federal government can no longer cover the deposits.

Likewise, governments intervene by socializing law enforcement which allegedly reduces the risk of violence. In the absence of police, people would invest more in managing their own risk—such as building their houses to resemble fortresses (as is more common in Central America). When civilization eventually collapses, people will finally realize that they have underestimated their risk exposure and libertarians will finally be vindicated.

In general, I believe this—in the long run. But in the short run, I believe socialized law enforcement generate efficiencies. Moreover, I operate on the assumption that the short run will last sufficiently long as to generate sufficient wealth to compensate for the eventual distortion that will occur if and when civilization eventually collapses.

Likewise, I’m not persuaded that we should design banking policy around the day that the federal government can no longer marshal sufficient resources to cover depositors in bank runs. Let government socialize the risk of bank runs (and, ok, perform the other bank monitoring roles). I’m content to let bank shareholders and bondholders be disciplined by the same market forces that discipline hardware store shareholders and bondholders.

But maybe I’m still missing the big picture….

vince

Mar 14 2023 at 3:23pm

That’s the problem, how far a panic will go and what will be the damage. Who can say? Accurate forecasting has a bad track record even without panics.

How to react to an impending panic is a different issue. IMHO the government reacts too quickly, too poorly, and too unfairly; IOW it too panics, as it benefits powerful interests and perpetuates the underlying problems.

Jose Pablo

Mar 14 2023 at 3:41pm

The best solution is to fully eliminate the reasons for the panic.

Let all the “deposits” being held at the FED (100% reserve rate), with the “comercial deposit banks” acting as pure “service providers”, collecting deposits and managing account services for a cut of the interests paid by the FED on these reserves.

Spencer

Mar 14 2023 at 8:49am

Check out Lyn’s Alden’s article

March 2023 Newsletter: A Look at Bank Solvency – Lyn Alden

The division between the small banks and the large banks.

Spencer

Mar 14 2023 at 9:32am

Japan solves all the payroll problems by guaranteeing all transaction deposits. And you wonder if short-selling should be legal for bank stocks?

Capt. J Parker

Mar 14 2023 at 10:20am

It’s one of those weeks when everything I though I knew is wrong.

A) SVB issued publicly traded stock. Shouldn’t the stock price give advance warning of trouble? If it doesn’t, is EMH wrong?

B) The Fed’s balance sheet is still at historically high levels. This should mean that the banking system is still awash with reserves. Why couldn’t SVB find lenders to cover it’s liquidity problems? I’m assuming here that SVB was solvent but illiquid.

C) One story is the steak through the heart of SVB was a downgrade by the ratings agencies. So do ratings agencies actual destabilize markets.

D) We’ve seen this movie before, the Fed raises rates then banks heavily invested in long bonds fail. And the ratings agencies gave zero warning. Does all the Dodd Frank risk management info go into a black hole? I mean, I get the whole issue of depositor insurance and bailouts remove any incentive for depositors to look into the financial stability of the bank they put their cash into. BUT if they did have incentive to do this would they do better than the ratings agencies or the regulators – given that the costs of researching the health of a bank can be high.

robc

Mar 14 2023 at 12:23pm

RE: A — SIVB hit a high of $597 last March. As of March 8, it was down to $267. And that was a pretty steady decline over that year, so how is that not advance warning?

Capt. J Parker

Mar 14 2023 at 4:38pm

Because Bank stocks were all doing really well in November 2021 and all fell steadily during the following 12 months and all had settled in back to their average 2018 to early 2020 range during Jan and Feb of this year. SVB had actually bumped up some from its Dec 2022 price.

Scott Sumner

Mar 14 2023 at 1:09pm

SVB’s problem was insolvency, not illiquidity.

Jose Pablo

Mar 14 2023 at 1:39pm

was it?

Not from an accounting perspective since the rules allow the bank not to mark to market their bond holdings (they were “not for sale”).

In fact, if the bank is allow to borrow with the nominal value of its holdings (not its market value) as collateral the insolvency problem is solved. That sounds more like a “liquidity” problem. Afterall, eventually, their bonds will be worth its nominal value (if the US government remains solvent)

Or maybe not.

[Btw, this episode left KPMG in an umpleasant position too]

vince

Mar 14 2023 at 3:53pm

Of course, you can have both problems. One definition of insolvent is the inability to meet financial obligations as they mature in the ordinary course of business. Check! Another is excess of liabilities over assets. Check!

A definition of illiquid is lack of cash to meet current obligations. Check!

Here’s a good article on detailed accounting aspects of the problem. The title has a great line, hide-til-maturity accounting.

https://blogs.cfainstitute.org/marketintegrity/2023/03/13/the-svb-collapse-fasb-should-eliminate-hide-til-maturity-accounting/

Don Geddis

Mar 15 2023 at 2:55pm

I wonder about this “insolvency” claim. It’s a little unclear, when it comes to banks.

As far as I understand, SVB had sufficient cash flow to handle ordinary operations (“indefinitely”). SVB also, from a technical accounting perspective, had a recorded value of assets that exceeded its recorded value of liabilities. So it was not technically “insolvent”.

However, once public rumors spread to a growing loss of confidence, then depositors tried to withdraw savings from their accounts. In our US bank structure, with fractional reserve banking instead of 100% reserve banking, no bank can possibly survive a classic depositor bank run. Every bank is “borrowing short” and “lending long”, and never has sufficient reserves to handle widespread customer withdrawals.

SVB lost to a classic “bank run”. It was more vulnerable than most banks, because it happened to concentrate on customers who had large account deposits well in excess of the FDIC’s $250K guarantee: 96% of all SVB deposits were uninsured (vs. 38% for BofA!). So once rumors started the loss of confidence, it became a game of musical chairs to get your money out.

A classic bank run doesn’t seem well described by either of the words “insolvency” or “illiquidity”. By that logic, every bank all the time would be in the same situation.

vince

Mar 15 2023 at 3:16pm

According to the article, at 12/31/22, with rounding, equity was $16 billion. That didn’t include fair value reporting for the held-to-maturity treasuries, which had an unrealized loss of $16 billion, wiping out equity.

Don Geddis

Mar 16 2023 at 2:04pm

According to accepted accounting principles, “held-to-maturity Treasuries” are accounted for at cost, not at fair market value. Therefore, according to accepted accounting principles, SVB was not insolvent.

You want to make up your own, private, different accounting rules. According to your special private accounting rules, you compute a negative net worth. Fair enough, you’re welcome to do that, for your own private analysis. But why should anyone care about your personal private accounting rules, that are not generally accepted in the accounting profession or the banking industry? Why should the word “insolvent” apply to your personal calculation, as opposed to the industry-standard calculation?

Vivian Darkbloom

Mar 16 2023 at 4:15pm

There are many definitions of “insolvent” or “insolvency”. It’s not a matter of making up a personal definition, but in choosing the standard most appropriate to the situation. Generally Accepted Accounting Principles as applied to US banks may allow US Treasuries which are intended to be held to maturity to be carried on the books at cost rather than current market value; however, those same accounting principles don’t themselves contain a definition of “insolvent”.

The most appropriate definition here is probably the one used in the US Bankruptcy Code. The Code indicates that a person or entity is “insolvent” if the liabilities exceed the assets “at fair value”. A presumption of insolvency is created if a person is unable to meet debts when they become due. For a bank, that would mean failure to be able to meet the demand of depositors for their money. That presumption as well as the standard definition of “insolvent” would apply to SVB. Most importantly, US bankruptcy law does not require that acceptable accounting rules by applied in determining “fair value”.

Never reason from an accounting identity!

Don Geddis

Mar 16 2023 at 8:20pm

Vivian: A reasonable reply. But SVB was not “unable to meet debts when they become due”. As to your second definition, that all depends on how many depositors choose to demand their money. If enough make that choice, then every bank is “insolvent”. It’s a kind of strange and not particularly helpful definition if “insolvency” cannot be determined from the bank’s internal financials, but instead depends on the whims of the external public.

That said, I appreciate the “bankruptcy code” perspective. And extra bonus points for your final sentence.

Ted Durant

Mar 17 2023 at 11:05pm

Scott is absolutely right. As of 12/31/22 SIVB could have liquidated its entire AFS and HTM portfolios, assuming the HTM portfolio valued at 85% of par, and covered 68% of their total deposits. Their entire HTM portfolio was agency MBS and CLO, i.e. highly liquid. Even if they got par for the HTM portfolio they could only cover 76%.

Richard W Fulmer

Mar 14 2023 at 11:33am

As with the Great Depression and the Great Recession, populists, politicians, and the media will portray this government-created panic as a market failure. The result will be more government intervention, which will lead to future crises that will be used to further increase government intervention. Eventually, the problem of periodic economic downturns will be “solved” by the imposition of a permanent economic downturn.

Scott Sumner

Mar 14 2023 at 1:09pm

Unfortunately, this is correct.

Jose Pablo

Mar 14 2023 at 2:44pm

Bank failures are not a “market failure”, actually you could say that they happen mostly because markets “work”. And because they work, some assets change their value.

The fact that some events (ie an increase in interest rates) affect the value of assests and your liabilities in a differen way, can not be labeled as a “market failure”.

Sure , there are “manager’s failures” and “auditor’s failures” and “supervision failure” in a banking crisis. Markets are not a vaccine against ineptitude (well, they kind of are, but only thru a painful mechanism that only works if the political authorities let it work).

What banks are is very fragile (thus the very real and unfortunate need for a “heavy” supervision). The question is why this inherent fragility has not been solved yet. Particularly when economist have had, for a very long time, a very neat and elegant solution to this: narrow banks + lending funds).

The need of bundling the “deposit” and “lending” services is overrated and causes way more pain than joy.

Richard W Fulmer

Mar 14 2023 at 3:11pm

It seems to me that markets are working, in part, to deal with government interventions including:

Erratic fluctuations in the money supply

Deficit spending, which can lead to inflation and higher interest rates that can, in turn, reduce the value of a banks’ assets

Bailouts that create moral hazard

Regulations that create perverse incentives (e.g., encouraging giving loans to individuals and small businessmen who may not be able to afford to pay them back)

Overly complex and burdensome regulations

Encouraging the buildup of debt through tax policies and by suppressing interest rates

Restrictions on bank mergers

The fact that, occasionally, some banks fail to negotiate the government-created obstacles and distortions is not surprising.

vince

Mar 14 2023 at 3:58pm

Haven’t you just stated the solution?

Jose Pablo

Mar 14 2023 at 6:08pm

Surprisingly enough the FED does not like this solution.

Maybe they love being the firemen for the arson prone bankers. Who knows.

https://johnhcochrane.blogspot.com/2019/03/fed-vs-narrow-banks.html

nobody.really

Mar 14 2023 at 4:08pm

What vince said. I’m not acquainted with this remedy (and I apologize if my other comments were unresponsive to this proposal).

Spencer

Mar 14 2023 at 12:06pm

Barnie Frank, who chaired the House Financial Services Committee, was on the board of directors.

Ted Durant

Mar 17 2023 at 11:07pm

To be clear, Barney Frank was a director at Signature Bank, no SIVB.

nobody.really

Mar 14 2023 at 3:15pm

Merle Hazard: How long (will interest rates stay low)? (2016?)

Jose Pablo

Mar 14 2023 at 6:29pm

I am not a fan of Krugman. But maybe he is right (to some extent).

When it comes to “making deposits” there is a huge different between what people think they are doing and what they are really doing.

They believe they are putting money in a safe. They can go to this safe an get their money whenever they want.

What they are really doing is a mixture of parking their money at the FED (maybe the closest you can get to this imaginary safe) + investing in a money market fund + investing in a debt mutual fund. And they are doing so without having any idea of how much of their money goes into each instrument.

And they have never discussed all the relevant issues for this kind of funds: which type of debt (counterpart risk), which duration, which leverage is the fund going to use, liquidity windows, …

Even more, and even worse, the bank keeps the return on this “unwilling investment” for itself partially to pay for the services provided to the “depositor that is not really a depositor”, sometimes offering him a “cut” on this returns.

Maybe this “perception gap” could be reversed in the absence of FDIC but it is also plausible to believe, with Krugman, that it will not.

Scott Sumner

Mar 14 2023 at 8:46pm

But people didn’t think this way before we had FDIC. So why would they if we abolished FDIC?

Jose Pablo

Mar 14 2023 at 9:44pm

Not sure of getting what you mean.

There were bank runs before the “moral hazard creating mechanism” (MHCM) that you discuss in the post. As a matter of fact, the FDIC (and even the FED) were created as a “respond” to banking crisis.

One reason is that banking as we know it (highly leveraged and partially financed with zero duration demand deposits) is inherently fragile.

The question is if clients, in the absence of the existing MHCM can “discipline” the banking sector. My point was that the difficulties of a proper understanding of the product by most bank clients (which are almost 100% of the population) would make this objective very difficult. So yes, you are right “we don’t buy a more stable finantial system with MHCM” but we won’t buy a stable finantial system withouth them, either

Ted Durant

Mar 17 2023 at 11:14pm

The vast majority of SVB depositors were corporations who were parking very large amounts of cash there for a variety of reasons. Some were lazy and couldn’t be bothered to diversify. A great many of them were tied to SVB historically, by SVB providing startup debt financing and, maybe more importantly, by providing introductions to important people who could help get them more financing and other, apparently salacious, enticements. IMO the biggest part of this story is that in 2021 SVB doubled in size, taking in over $100 billion in new deposits. In 2022 they shrank slightly, and a very large chunk switched from noninterest to interest-bearing. “Ponzi Scheme” is overused, but an influx of $100 billion of cash can cover a multitude of bad decisions that come to light when the cash starts flowing back out.

T Boyle

Mar 17 2023 at 6:14pm

Scott is right: there’s a lot of nonsense written about moral hazard in banking.

This article is one of them.

Deposit banking involves the bank borrowing short and lending long. This creates a mass game of Prisoner’s Dilemma for the depositors (from whom the bank borrows short): if they (mostly) cooperate, they get interest on their deposits; if they (mostly) defect, they may not get all their money back; but those who defect first do better than those who defect later.

Prisoner’s Dilemma is an insightful piece of game theory. It is not an example of moral hazard, and it can’t be solved by the prisoners doing more diligent research. The key piece of information, in this case, is whether – for good OR BAD reasons – your fellow depositors are going to defect en masse. You can’t know that, and researching the bank’s finances provides only limited protection: the banks that failed recently were well-capitalized days before they failed; do you really think a depositor could have foreseen $42 bn in withdrawals in a single day through any amount of diligent research?

This is why deposit insurance can – and probably does – reduce the propensity for bank runs: any fool rumor could cause a run, so without deposit insurance it is best to defect first and not wait to verify the rumor – thus causing the run regardless of the truth of the rumor.

I’m not saying deposit insurance is the best solution. But “let the bank runs happen and let the depositors lose their money” is a pretty bad one.

Comments are closed.