In the 50 years since The Limits to Growth was published in 1972, its grim Malthusian message has gripped the social consciousness. Its central thesis was that since the earth’s resources are finite, it would not be able to support the exponential rates of economic and population growth and would collapse before the end of this century. This proclamation has become the fountainhead behind calls for growing centralization and the establishment of limits to curtail the freedom of individual choices.

Global institutions such as the World Health Organization, the World Economic Forum have pointed to air pollution, climate change, overpopulation, and water scarcity as some of the biggest threats to human well-being. The consensus among policy-makers, politicians, and environmentalists seems to be that entrepreneurs and firms good will use the cheapest means of production possible, even as they degrade the environment. Therefore, any reliance on market mechanisms to solve the problem of environmental degradation and to provide sustainability are automatically ruled out.

Similarly, the consensus that consumers are driven by personal desires to overconsumption implies consumer sovereignty must be put on hold in pursuit of a sustainable world in which the needs of today are met without compromising on the needs of future generations.

It follows from such consensus that the solution must be global, as there are potentially massive consequences for failure, and that a centrally planned approach is the only feasible solution. The centralized approach to solving the problem of environmental degradation assumes rational, well-informed people with massive resources will deal with the massive issues of environment conservation in a well-intentioned and efficient manner for the public good.

This approach in practice would mean doing away with civil liberties if they interfere with the plan of environment conservation. But as sovereign individuals who desire a free world and who hold values of liberty and dignity of human beings sacred, we must pause before making such a Faustian bargain. Stop and think carefully about the true nature of environmental degradation, the effects of scarcity on the economy, and how a spontaneously ordered system such as the market might deal with it.

Apart from the intellectual stimulation that history provides, it can also provide us with lessons from past experiences, and we have enough evidence from the experiments of centralized planning to make us intellectually suspicious of it.

Markets Deal with Scarcity.

The economy consists of huge numbers of buyers and sellers who respectively supply and demand vast quantities of goods and services. Therefore, there is an enormous amount of information available to them in a decentralized manner- but this information about demand and supply are important for everyone as it impacts the decisions they make in their day to day lives. This is where monetary valuation comes in. Based on competition between buyers and sellers through a bidding process, prices are formed which convey information about such things.

Prices in the market act as coordinating signals which convey information about important economic data scattered in a decentralized manner. The role of prices in coordinating actions in the market was one of the core arguments advanced by Fredrick Hayek on why centralized planning could never allocate resources as effectively as markets do.

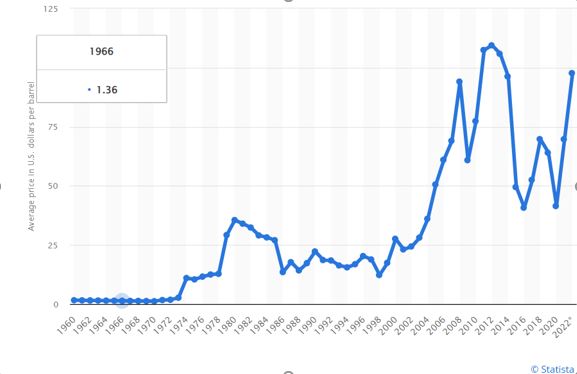

When something is scarce in the market, a large number of its users compete in the market over its possession which leads to the increase in its prices initiated by the seller to economize on its existing stock. The increased price is a signal in the market reflecting its scarcity. If the claims of The Limits to Growth are true, then prices of natural resources which are used heavily in energy consumption should increase.

This increase in the price is necessary to substantiate the claim that this resource scarcity limits to economic growth, as energy consumption is bound to increase with increases in economic activity. If the resource prices today were exponentially higher than they were in the past,

But the reality has been much different. Despite the fall in the purchasing power of the dollar and the cartelization of oil, an item that cost 50 dollars in 1970 would theoretically cost 335.5 US dollars in 2020 (50 x 6.71 = 335.5). But the increase in the rice of oil is quite low relative to the fall in the value of the dollar, which suggests that the real increase in the price of the oil barrel is negligible. Might this convince people to change their minds?

Vibhu Vikramaidtya is a scholar with research interests in capital theory, monetary theory, and business cycles writing about events in the economy from a legal and economic standpoint. His other works can be found at the Austrian Economics Center, the Libertarian Institute, and beinglibetarian.com.

READER COMMENTS

Everett

Nov 5 2022 at 7:41pm

What are your thoughts on regulations focused on halting Red Queen’s races?

With respect to market signals, what are your thoughts on monopolization of natural resources or vertical integration vis-a-vis scarcity? A monopolist doesn’t have to price based on scarcity. They can sell it all at a fixed price, and once it’s gone, it’s gone (this is effectively what happened with gold mines when the price of gold was fixed to the currency, wasn’t it?)

Is it appropriate to calculate the cost of oil in terms of barrels, or the cost of oil in terms of fractions of total oil production? After all, I can go to a scrapyard and get a bunch of formerly $2000 items for nothing. High durability commodities (fossil fuels, metals) have to have a different price change effect than low-durability commodities (food, smartphones).

And, of course, every environmentalist’s favorite bugaboo: externalities. Is it plausible to say that the externalities of a barrel of oil today are more so than in the past? And that the socialization of these externalities, if accounted for, would dramatically increase the cost of that barrel of oil? The world has paid a lot for geopolitical stability of oil producing countries, and continues to do so. A ton of quid-pro-quo happens to keep oil market prices from being too chaotic.

Trying to apply market theoreticals to cartels which, at the margin, have *always* been able to charge far more than the cost of production seems inappropriate. And then of course there’s the problem that oil is a theoretically fungible commodity (replaceable, in part, by other hydrocarbon sources, including renewables). To maintain the cartel pricing as best as possible it is required to cap the price. This may an argument in favor of market power. But you can’t overlook that oil is also used geopolitically.

I don’t know that oil is the best commodity to make this point with.

My fundamental critique of your post though is this: “It follows from such consensus that the solution must be global, as there are potentially massive consequences for failure, and that a centrally planned approach is the only feasible solution.”

The one doesn’t not follow from the other. For something like carbon, and other forms of distributing pollution, the limits must be global, but the actual solutions needed to reach those limits can take place in a distributed and competing market. It is the fundamental purpose of free governments to tell people when to stop throwing their fists around because they are coming into proximity to other people’s noses. This is the purpose of regulation. Done right regulations serve both the public welfare and the public freedom.

Another critique: “If the claims of The Limits to Growth are true, then prices of natural resources which are used heavily in energy consumption should increase.”

Does this book claim that prices will rise, and how they will rise, or simply that we’ll run out? If they don’t claim that prices will necessarily rise, or how those prices will rise (e.g. price stays the same until a particular scarcity level is hit, and then it shoots through the roof), then it’s unfair to impute a market-economics claim to the authors as an argument against their thesis.

And my fundamental disagreement with “The Limits of Growth” is on the microlevel: Industries and regions can collapse, creating room for the growth of other industries and regions. No, you can’t increase the average forever, but you can keep changing the measuring stick.

Vibhu Vikramaditya

Nov 6 2022 at 8:55am

Hey Everett, Thank you for your remarks. Let me start by asserting, My understanding of competition is vastly different from the onse espoused in the perfect competition ideal where price is necessarily equal to its marginal cost of production and hence my understanding of how the market produces efficient outcome is also different from an where production is taking place at the lowest point of the marginal cost and where prices equal such cost. The efficiency which I have in mind is a dynamic one where over time lower cost production structures are discovered and used by entrepreneurs in form of lower prices to win market shares. As long as the barriers to entry are not outlawed by legislature, if a monopoly seller of a good charges a higher price than one which another who can produce the same good at a lower cost, the entrepreneur will use initiate a new set of prices use to earn marker shares and profits. It may often be that the product produced by the new entrepreneur is the same in form or it may be in a newer form. Unfortunately, a passage from this post is missing, where I discussed how old energy forms such as wood are gradually replaced by different energy forms by new entrepreneurs. A cartel or a monopolist can this only raise prices today to their own disadvantage in the future unless there are some real constraints which are physical in nature. This is where my take on the definitive points of the book follows, i.e even if there are real constriants, higher prices would make sure there are no limits to growth, the other thing I wanted to show though that currently there are no such constriants , exemplified by the lower rise in prices relative to higher increases in its use. Regarding your point about externalities, again my conception of externalities is based on either uncharged profit opportunities in terms of positive externalities for firms or unchanged property rights violation costs which the entity producing negative externalities owes to its recipients. Regarding specific forms of CO2 problems, we should let industries develop certain machines which can detect CO2 emissions from particular places and give them a unique label like is done in supply chains, then individuals and other entities who receive such problematic CO2 emissions and charge them in court.

Thomas Lee Hutcheson

Nov 7 2022 at 1:36pm

The externality is not oil production it is in CO2 emission. The link between the two is quite tenuous.

Everett

Nov 5 2022 at 7:44pm

Please check the spam filter.

Fazal Majid

Nov 5 2022 at 10:22pm

J. K. Rowling has created billions of dollars of value out of thin air, with minimal use of non-renewable resources. The only real limit to growth is the human imagination now that capital is a commodity.

Thomas Lee Hutcheson

Nov 6 2022 at 6:46am

“policy-makers, politicians, and environmentalists seems to be that entrepreneurs and firms good will use the cheapest means of production possible, even as they degrade the environment. Therefore, any reliance on market mechanisms to solve the problem of environmental degradation and to provide sustainability are automatically ruled out.”

It seems that the exact opposite conclusion holds. Only market solutions — Pigou taxes on negative externalities can solve problems of environmental degradation?

Thomas Lee Hutcheson

Nov 6 2022 at 6:52am

“air pollution, climate change, overpopulation, and water scarcity as some of the biggest threats to human well-being.”

Biggest? Who knows? Big enough to justify investment in reducing their impact? Yes. But either way it has little relevance to growth.

Thomas Lee Hutcheson

Nov 6 2022 at 7:01am

After a good start criticizing the silliness of the “running out of resources” idea becasue markets will price scarce resources, the author, unfortunately, fails entirely to actually address the issue of externalities where, so far at least, transaction costs have failed to allow the development of a market in the CO2 concentration of the atmosphere.

Walter Donway

Nov 6 2022 at 9:20am

Footnote: I made the point in an OLL article a couple weeks ago that Malthus did not predict inevitable doom. He believed that popular education could arm people to deal with the problem of runaway population growth. He was a Church of England cleric and argued that government could not provide such education; he wanted the church to take on universal primary education. The chief positive result he expected: sexual restraint.

The characterization of economics as “the dismal science” may not have referred to Malthus; it was used much later by Thomas Carlyle, who was criticizing John Stuart Mill for advocating emancipation of slaves.

Comments are closed.