I was almost going to write “dead”, but then thought that this would give readers the erroneous impression that I don’t expect any more recessions. Rather I believe the term ‘cycle’ is no longer descriptive.

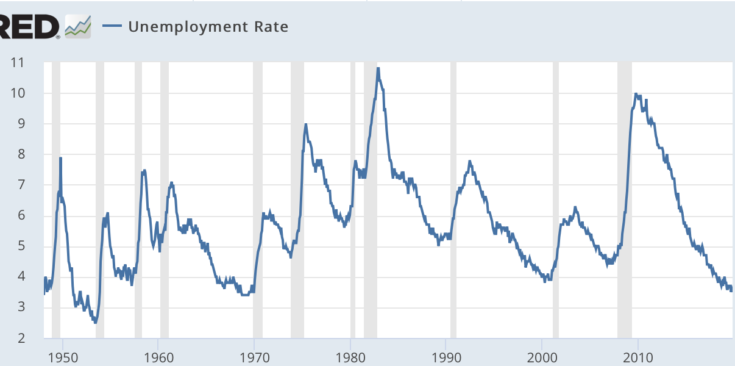

In November 1982, the unemployment rate hit 10.8%, the highest rate since WWII. The US had experienced 8 recessions over the previous 37 years (9 recessions over the previous 38 years), and they seemed to be getting worse (1974 and 1981-82 were the two worst.) No one expected that the US would experience only 3 recessions over the next 37 years. What went right?

During the postwar period, monetary policy was under the influence of a rather simplistic Keynesian model. The problems of the 1970s and early 1980s led to a Keynesian/monetarist synthesis called “New Keynesianism”, which incorporated monetarist ideas such as the Natural Rate Hypothesis and the importance of the Fisher effect. It also incorporated Keynesian ideas such as interest rate targeting and policy activism. The Taylor Rule is a simple way of thinking about this synthesis.

As monetary policy became more effective, recessions became much less frequent. Importantly, this process is likely to continue. If we achieve America’s first ever soft landing over the next 2 or 3 years (as I anticipate), then I would expect only one recession during the next 37 years.

The economics profession has not yet fully absorbed the implications of improved monetary policy. Here’s Noah Smith:

It’s impressive how well the U.S. economy has held up during the past year. As early as 2018, leading indicators were suggesting a heightened risk of recession in 2019 or 2020. Then early this year the yield curve inverted, a traditional signal that recession is imminent (the inversion has since reversed, but this typically happens before growth actually goes negative). The trigger for a downturn wouldn’t be hard to identify — a slowing China, combined with President Donald Trump’s trade war. Already, countries such as Singapore and South Korea, which export lots of manufactured goods to China, are slowing down.

But despite all the pieces that seem to be in place for a recession, it hasn’t happened. This expansion is now the longest in postwar history, having recently surpassed the long boom of the 1990s.

That’s all quite reasonable, but I have a slightly different take. Smith is quite right that real shocks are often a “trigger” for recessions—recall the housing/banking crisis of 2007-08. But they are not the cause of recessions. Instead, recessions are caused by tight money policies that result in a sharp slowdown in NGDP growth. As monetary policy improves, real shocks become increasingly unlikely cause bad monetary policy, and hence less likely to trigger recessions. More likely, real shocks will trigger RGDP growth slowdowns, as in 2015-16.

But 2015-16 wasn’t even close to being a recession, as the unemployment rate continued to fall. America has never even had a mini-recession where the unemployment rate rose by only 1.0% to 2.0% and then starts falling, so a period where unemployment declines is radically different from a period where the unemployment rate rises by more than 2.0%.

Just as the bad period of the 1970s and early 1980s led to improvements in monetary policy, the Great Recession has led to further improvements. The Fed now understands that the natural rate of interest is in long-term decline. The past three recessions were partly caused by the Fed overestimating the natural rate of interest, and hence not cutting rates rapidly and deeply enough to prevent recession when trouble developed. They are less likely to make that mistake in the future. The Fed also has a better understanding that inflation shocks like 2007-08 are not worth worrying about in an environment where NGDP growth is slowing. They also understand the need to commit to something like level targeting in a slump. The one negative, of course, is that the Fed is more likely to face the zero bound problem going forward.

The reduction from 8 recessions in 37 years to only 3 recessions in 37 years is less impressive than it seems. Because of lackluster recoveries, the percentage of time with high unemployment has declined much less than you’d expect. But a further reduction to one recession in the next 37 years really would be a big deal. That would imply that the Fed has learned how to engineer soft landings, creating long periods of near full employment.

Given that we’ve never had a soft landing, why am I so optimistic that we are about to achieve the Holy Grail of macroeconomics? Because other similar economies such as Australia and the UK have learned how to achieve soft landings, and hence I see no reason why recessions won’t continue to become increasingly uncommon in the US.

In the 38 years after WWII, recessions occurred roughly every 4 years, on average. They were similarly frequent before WWII. If I’m right that we will have only one recession during the next 37 years, then the term ‘cycle’ will no longer be appropriate. In that sense, the business “cycle” is dying.

Right now, this is a “tentative prediction”, contingent on no recession over the next three years. If this soft landing occurs, then I’ll switch from a tentative to a confident prediction. I obviously won’t live long enough to see if my 37 year prediction comes true, but I hope and expect to live long enough to see if it is likely to come true, if soft landings become a normal part of the American macroeconomy.

READER COMMENTS

Steve Fritzinger

Dec 7 2019 at 2:16pm

Was the term business cycle ever applicable?

A cycle means a predictable, repeating series of events. Like a two cycle engine or night following day or spring, summer, winter, fall.

The economy does do that. It’s closer to my body. I have periods of good health followed by periods of sickness followed by the return of health. But if never call that a wellness cycle.

Steve Fritzinger

Dec 7 2019 at 2:17pm

Third paragraph should read “economy doesn’t do that”.

Scott Sumner

Dec 7 2019 at 6:54pm

You are right, the cycle was never predictable.

Alan Goldhammer

Dec 7 2019 at 3:49pm

The strange thing is the decrease in manufacturing employment. What is the breakdown of employment by sector? Does the increase in corporate debt even mean anything these days? There are so many weird signals these days that it is difficult to make any prediction about what will happen. The only thing for certain is that tariffs are bad but maybe that is not even true.

Jon Murphy

Dec 7 2019 at 8:03pm

I don’t follow. Why is that strange?

Alan Goldhammer

Dec 8 2019 at 9:04am

President Trump promised to bring manufacturing jobs back to the US as part of MAGA and his tariff imposition. Manufacturing jobs have been a key part of upward mobility in the US over the years. Their absence argues for increased economic inequality (says me as a non-economist).

I tried to look at the FRED database to see if there is a historical breakdown of employment sectors but could not. There are recent articles about the increase in warehouse employment because of the shift to e-commerce purchasing. Are these employees making a smaller salary than those at brick and mortar stores who they have displaced?

Jon Murphy

Dec 8 2019 at 11:15am

Yeah, but as any economist could tell you, that would not reverse the decline, especially since the decline is due primarily to automation.

When the economy was moving from relatively low-paying ag jobs to relatively high-paying mfg jobs, that was true. Now as the economy is moving from relatively high-paying mfg jobs to relatively even-higher-paying service jobs, that is not true. And, for much of human history, those ag jobs were upward mobile compared to hunter-gatherer. Economies change.

Not necessarily for the reason I just stated.

I still don’t get what you see as “weird.” I mean, US manufacturing employment, as a share of total employment, has been generally falling since the end of World War 2. In terms of absolute numbers, manufacturing employment has been falling since 1979. So, what is “weird”? “Weird” compared to what?

I know FRED has that data broken down by NAICS industry, but you kind of need to know what you are looking for. Their data comes from the BLS’ “Current Employment Survey,” and that is marginally easier to navigate.

nobody.really

Dec 9 2019 at 6:34pm

Is this just a throw-away line, or are you actually claiming that average/median service jobs generate more compensation than manufacturing jobs? I’d be delighted to see some data on this.

Jon Murphy

Dec 9 2019 at 9:35pm

I’m saying the median job created tends to be higher paying than the median job lost in manufacturing.

Lorenzo from Oz

Dec 7 2019 at 6:01pm

What I say to people is that Australia still has a business cycle, just a very flat one.

Todd Kreider

Dec 7 2019 at 6:08pm

Noah Smith wrote:

Neither China’s moderately slowing growth nor Trump’s tariff hikes could be large enough to affect the U.S. economy in more than a trivial way unless a real trade war developed, which hasn’t happened.

Singapore is a city with a very small economy, 0.3% of the world’s GDP, so not a possible trigger of anything and South Korea is also very small at just 1.6% of world GDP and has had its growth fall from 2.7% in 2018 to 1.9% this year so can’t have a more than trivial impact on the U.S. economy, either.

Jon Murphy

Dec 9 2019 at 10:31am

Lots of trivial water drops make up a flood.

But again, the point is those items are a trigger, not the cause. To keep the water metaphor going, a rainstorm that drops 1/4 inch of rain (a trivial storm) may be just enough to trigger a flood if the river is already swollen from melting snow

Benjamin Cole

Dec 7 2019 at 7:40pm

Well, maybe all true as no one in macroeconomics is ever wrong.

But, if we have globalized capital markets, and interest rates on long-term bonds are set globally, and if Fed quantitative easing purchases assets from a global asset market, then we must consider if US economic performance is related to the policies of not just the Fed but also other major central banks ( and even, for a while, the ferocious $800 billion quantitative easing program of the Swiss National Bank).

Money is fungible, and the investor class global.

Jonathan S

Dec 8 2019 at 12:40am

What is the likelihood that the US has more protectionist trade policies for at least a decade over the next 37 years? If the Republican and Democratic parties’ push back against free trade continues throughout the 2020s, would you expect your prediction to fail?

Matthias Görgens

Dec 8 2019 at 3:29am

Tariffs would fall under the ‘real shock’ category Scott talked about.

Ie they are bad, but with competent monetary policy, they want lead to a drop in ngdp, and thus also not to an increase in unemployment.

Somewhere else a market monetarist (I think it was Scott, but not sure) wrote something like: competent monetary policies makes economies approximately classical. So that eg Say’s Law becomes true.

Matthias Görgens

Dec 8 2019 at 3:30am

“they want lead” should of course read “they won’t lead”.

P Burgos

Dec 8 2019 at 1:44am

If there aren’t recessions in the US, how will US presidential elections be determined? Will it all just be a flip of the coin from here on out?

nobody.really

Dec 9 2019 at 6:41pm

Ha! That’s cute–and thought-provoking.

Historically, a strong economy helped the incumbent. But if we enter a world in which a strong economy is a given, it might cease to be a relevant factor in the elections.

After all, how often to people say, “I’m sticking with the incumbent, ‘cuz he’s maintained a steady air supply”? We all care about breathing–but nearly everyone takes it for granted, so it doesn’t become a basis for political decisions.

ChrisA

Dec 8 2019 at 4:40am

I wonder if in the past that the unemployment rate would have eventually ended up as low as today if the expansions had not been interrupted by recessions. In other words it can take a long time for unemployment to sort its self out, or another way of putting it is that people remember their highest nominal wage for quite a while and will not take the insult of a lower one, even if it means being out of work. This is another good reason to avoid these kind of shocks and have better monetary policy, unemployment for some people can be very long lasting.

Brent Buckner

Dec 8 2019 at 8:48am

c.f. https://worthwhile.typepad.com/worthwhile_canadian_initi/2019/11/boiling-frogs-slow-recoveries-are-deep-recoveries.html

ChrisA

Dec 8 2019 at 9:35am

Good link, thanks.

Thaomas

Dec 8 2019 at 6:36pm

I’d say that as long as the “improvement” in Fed policy making is in better predicting the correct interest rate, we will remain vulnerable to recession. Only if they move to level targeting of the Price level as the “price stability” portion of their dual mandate (or NGDPLT for both) will we be almost immune to recessions.

robc

Dec 9 2019 at 8:45am

Is the lack of recessions a good thing?

I mean, it is good in that moment, but I am more concerned with long term growth rates. Is it better to have an occasional short, deep purge or to continue along?

What I worry about is our options are either continuous growth of 1.5%, vs “cycles” that average 2.5%. The latter is better.

Milljas

Dec 9 2019 at 9:15am

Surprised you don’t mention less emphasis on Phillips Curve thinking today vs the past. The 2015/2016 slowdown seems to be a big moment. Perhaps that’s part of the NK decline.

Michael Rulle

Dec 9 2019 at 1:10pm

Some readers commented on whether “no cycles” are good or not if growth is slower. Good point. But, personally, I prefer less uncertainty in exchange for some small amount of growth—but I do not see why such a trade-off should occur.

It is remarkable that at least for the second time in recent months you have written this same essay—which I interpret as your increasing–even if already strong—confidence in it. Putting aside whether policies can change for a variety of bad reasons–(bad and ignorant new Fed appointees for example)—-your hypothesis is truly extraordinary—–groundbreaking—(unless there are many more like you out there).

I would love to read your ideas on how our seeming untenable fiscal path (underfunded pension funds/SS and medicare) at the State, Corporate, and Federal level impacts your ideas. My view is it merely lowers growth overall–(or increases work requirements in the future) not that it should increase the number of cycles.

To repeat—-your hypothesis is the equivalent of a new extraordinary scientific discovery. And all new discoveries should be required to have extraordinary evidence to back it up. Economics, however, is a tough subject to crack—-still I assume you are aware of the importance of your prediction.

nobody.really

Dec 9 2019 at 6:54pm

I gotta say, a mere ten years after the last massive recession, predicting that we’ll go another 27 years until the next one seems insanely optimistic to me. To the contrary, I’d guess that political forces will gradually erode the various safeguards put in place since the last recession (Sorbanes-Oxley?), and that innovations will create unprecedented markets in this or that which Enron-type people will be able to exploit for short-term profits, all leading to another collapse eventually.

Are there any prediction markets about when the next recession will occur?

I also gotta say, notwithstanding everything I’ve read hear over the years, I still have not internalized the rationale for targeting NGDP. Every time I read that term, it goes into my “gotta learn about that someday” box. In short, perhaps Sumner understands some secret sauce that I just don’t.

P Burgos

Dec 10 2019 at 2:42am

Re: SOX

The big accounting firms have offices in nearly every metro in the US with a population greater than 1 million people. The partners of those firms probably all give to local congress representatives and all would vociferously oppose watering down SOX. Way too much money for them to lose.

Scott Sumner

Dec 11 2019 at 10:43pm

You said:

“predicting that we’ll go another 27 years until the next one seems insanely optimistic to me.”

I did not make that prediction. I said one recession during the next 37 years.

Fred Foldvary

Dec 9 2019 at 8:13pm

This cycle is still spinning:

http://www.foldvary.net/works/cycle.html

Jeff Hallman

Dec 10 2019 at 9:53am

Scott attributes the improved monetary policy this century to better theoretical understanding of the economy, and yet at the same time laments how most of the profession, including policymakers, continues to espouse vulgar Keynesian models that were discredited more than 50 years ago. Economic policy arguments seem to never change: we still have people arguing about minimum wages, rent controls, fiscal vs. monetary policy, socialism vs capitalism, and on and on. No one but Scott Sumner and Peter Temin apparently learned anything from the FDR devaluation, and that includes FDR himself. But this century monetary policy has finally gotten better. My contention is that it’s not that theory has improved, but rather that improved data in the form of TIPS yields now constrains the Fed to behave more appropriately.

TIPS were first issued in 1997, but the five-year TIPS note, which has the most relevant information content for monetary policy, has only been around since 2004. They were still new enough and low-volume enough in 2008 that not many people at the Fed were paying much attention to what the TIPS yields indicated about the appropriateness of monetary policy. But Scott Sumner and other Market Monetarists did a lot to make the Fed start paying attention, and the result is that even inside the Fed, if TIPS yields start indicating monetary policy is off target, someone will bring it up and ask questions. Formal targets are not actually necessary: embarrassing the professional staff seems to be enough to get reasonable monetary policy.

Milton Friedman used to point out that the reason business cycles all look alike is they are all driven by bad monetary policy. With the TIPS market finally providing a real-time check on the Fed, recessions may actually be a thing of the past.

Lorenzo from Oz

Dec 10 2019 at 4:16pm

That seems very plausible.

Lawrence Ludlow

Dec 11 2019 at 9:07am

MEASURING ONLY ONE ASPECT OF ECONOMIC BEHAVIOR.

I’m no economist, but doesn’t the thesis of this article require limiting one’s vision to a question that is too small? It’s one thing to examine business downturns as this article does, but it seems to ignore what may (or may not) be the trade-off: anemic economic growth. In other words, what good is it to prevent recessions if economic growth is so disappointing? Isn’t monetary management of this kind a bit like administering lithium to bi-polar folks? True, they never hit those extremes, but they function within a really narrow range.

Scott Sumner

Dec 11 2019 at 10:44pm

Why would moderating the business cycle cause slower long run growth? Isn’t money neutral in the long run?

Comments are closed.