David Beckworth recently asked former Fed governor Randal Quarles why the Fed didn’t move last fall to stop inflation. Here’s how Quarles responded:

Quarles: This is maybe an eccentric belief. I don’t think that it’s universally shared or even widely shared on the FOMC. But my belief is that it’s a separate element of the Fed religion that resulted in not moving in the fall, and it became clear that it was time to pivot to withdrawing accommodation, and it’s a long-standing kind of Fed principle that you shouldn’t step on the gas and the brake at the same time; meaning that you shouldn’t be raising interest rates at the same time as you are still increasing the size of the balance sheet. And so we had decided that we needed to taper the balance sheet purchases. The lesson of the taper tantrum under Bernanke was that you’ve got to telegraph that well in advance. You’ve got to do that gradually, in order to avoid disrupting markets. And you have to have completed that before you can start raising interest rates so that you’re not doing two conflicting things. So that was the sequencing.

Macroeconomics is full of myths. There’s a widely held (false) belief that the US ran unusually big budget deficits during the 1960s, and that the high inflation of the 1970s was due to supply shocks. The idea that there was a “taper tantrum” in 2013 that “disrupted markets” seems to be another popular myth. Where is the evidence for that claim?

FWIW, here is the S&P500 in the year after Bernanke’s May 22, 2013, speech on the need to eventually taper bond purchases (a rather obvious point, BTW):

Notice that the speech did not cause any stock market turmoil, either immediately or over the next 12 months. Nor was there any major market reaction to Bernanke’s speech in the bond market, although long-term rates did trend upwards due to a stronger than expected economy in late 2013. (The policy was unwise, but that’s because inflation was too low at the time.)

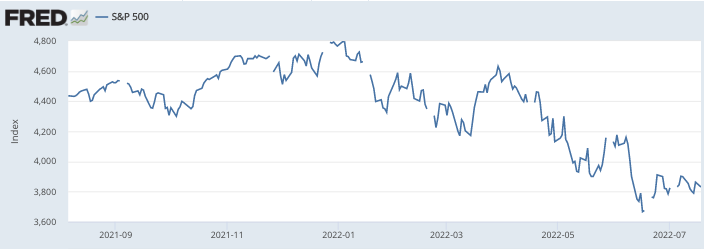

Quarles suggests that in the fall of 2021, the Fed responded to this phony “lesson” by doing nothing to restrain inflation. Today, frustrated stock and bond market participants must be grumbling “thanks for nothing”, as the Fed’s inaction ended up causing a market tantrum in 2022, with the economy surging to high inflation and as stock and bond prices falling sharply:

As I keep saying, the Fed should not focus on stabilizing financial markets; they should focus on stabilizing expected NGDP growth. Stable financial markets cannot be engineered artificially; they result from stability in the broader economy.

The Fed needs to keep its eye on the ball:

READER COMMENTS

Kevin Erdmann

Jul 19 2022 at 7:57pm

“The idea that there was a “taper tantrum” in 2013 that “disrupted markets” seems to be another popular myth. Where is the evidence for that claim?”

The cat doesn’t know why I suddenly jumped up from my chair and started clapping.

robc

Jul 19 2022 at 8:48pm

I had never heard the term until last week.

Rajat

Jul 19 2022 at 11:34pm

I don’t disagree, but I think you haven’t appreciated the time horizon that traders, commentators and the Fed watch financial markets. The S&P500 closed at 1669 on 21 May 2013, and then fell to 1573 by 24 June, a fall of nearly 6% in about a month. That’s hardly a crash, especially after a steep rise of more than 20% over the previous 6 months, but it was obviously enough to create nervousness. Especially after several years of excessively tight policy, maybe that was understandable at the time, if not now.

Scott Sumner

Jul 20 2022 at 1:39am

If markets are efficient, why wouldn’t the immediate decline be the one to look at? And if the right approach is to look at the longer term impact of Bernanke’s speech, why look at 30 days? Why not look at 60 days, or 120 days?

More broadly, even if the 6% fall is the right way to look at the impact of Bernanke’s speech, why should the Fed care about that decline when deciding what’s best for the economy? Stocks have always been quite volatile.

John Hall

Jul 20 2022 at 8:50am

“Nor was there any major market reaction to Bernanke’s speech in the bond market, although long-term rates did trend upwards due to a stronger than expected economy in late 2013. (The policy was unwise, but that’s because inflation was too low at the time.)”

US Ten-year yields went from 1.94% before Bernanke’s May testimony (he gave it on May 22, this is from May 21). By June 25, yields had risen to 2.60%. By the end of the year, they had risen to 3%. The big movement happened in the month following the speech. Conveniently, this period is also when the alleged “taper tantrum” also happened in equity markets.

John Hall

Jul 20 2022 at 8:51am

First sentence should be “US Ten-year yields were 1.94% before Bernanke’s May testimony (he gave it on May 22, this is from May 21).”

Scott Sumner

Jul 20 2022 at 12:48pm

Yes, and the fact that equities rose during this period is a good indication that the higher rates reflected accelerating growth. Market reaction to Bernanke’s speech should not have taken 6 months.

In any case, rising interest rates during a period of accelerating economic growth is hardly “disrupting markets”.

Kevin Erdmann

Jul 20 2022 at 5:21pm

I remember listening to Bernanke on, I think it was June 18 or 19, when he was backtracking a little bit because of the supposed tantrum, and he reassured the questioners at the press conference that the Fed wouldn’t stop QE right away, that they would continue purchasing securities to keep long term yields low in the meantime, and only slowly reduce and then reverse the purchases as economic data improved. I looked at the futures market quotes, and rates went up by 10-15 basis points while he was speaking.

Scott Sumner

Jul 21 2022 at 3:43pm

Good point.

John Hall

Jul 21 2022 at 9:33am

Unfortunately we don’t have good real-time estimates of growth expectations at that frequency. The SPF 1-year ahead NGDP forecast was 4.6% in Q2 and 4.5% in Q3, which isn’t a very large change. The RGDP forecast was roughly unchanged, going from 2.75% to 2.7%. If anything, they are moving in the wrong direction, but not high enough frequency to say anything conclusively. If anything, longer-term expectations tend to be more stable, which partly drives the pricing on ten-year yields.

The critical “taper tantrum” period is May 21 2013 to June 25 2013. The spread between 10-year yields and 5-year yields was roughly unchanged over this period, suggesting that the bulk of the movement happened at the shorter end of the curve, which tends to be more influenced by what is happening by the Federal Reserve. The spread between the 5-year and the 2-year widened by 49bps, while 2-year yields rose about 16bps. That 16bps move can be largely explained by higher expectations of Fed tightening. According to Bloomberg’s OIS Implied Probability tool, Fed Funds were pricing in around 8% chance of bringing rates to 0.375% by January 2014. By June 25 2013, that rose to roughly 30%. It is hard to ignore that the expectations of additional Fed tightening is getting priced into the market.

Now it is reasonable to argue that some of those expectations are driven by what is happening in the economy, but it is hard to disentangle to what extent it is driven by the economy and perhaps a change in Fed policy irrespective of changes in the economy (i.e. perhaps the Fed changed their reaction function and communicated that to the market).

We can learn a little bit more by looking at the movement of five-year yields vs. TIPs. The upward movement over that period corresponded with jumping real yields and falling breakevens. The five-year TIPs yield rose from -1.15% on May 21 2013 to -0.16% on June 25 2013. Rising real yields at the short-end is the part that is hard disentangle between what is driven by changes in the economy vs. changes in the market’s understanding of the Fed’s reaction function. Unfortunately, we don’t really have the data to answer this conclusively, but my sense is that GDP growth expectations did not change enough to justify this movement and changes to the market’s understanding of the Fed’s reaction function is a much better explanation of it.

By contrast, five-year breakevens fell over this period from 1.99% to 1.65%. Falling inflation expectations are consistent with a positive aggregate supply shock or a negative aggregate demand shock. Your argument about more favorable growth later in 2013 implies either positive aggregate supply or demand shocks, but only the aggregate supply shock is consistent with falling inflation expectations. My argument is that a negative aggregate demand shock, caused by market participants re-evaluating the Fed reaction function gradually over the course of the month, put downward pressure on inflation and upward pressure on short-term real yields.

Equities, also, didn’t increase over this period. The S&P 500 fell from 1669.16 to 1588.03, or about a -4.8% decline. My “alleged” taper tantrum statement was a reference to your argument that the taper tantrum is a myth. Stocks did decline, roughly -5%. The more sophisticated “what taper tantrum? no taper tantrum here” argument is that stock markets decline -5% rather often and this isn’t so bad of a decline all things considered. I wouldn’t be necessarily opposed to that argument, but when you say that nothing much happened in bond markets, I would disagree quite a bit more strongly. The strong movement in both the bond and equity markets is what led Bernanke to walk back his statements later in June.

Scott Sumner

Jul 21 2022 at 3:49pm

I guess I just don’t understand what point you are trying to make. Why do you think a “taper tantrum” played out over 30 days? What evidence do you have? What model would predict that? It seems to me that you picked the 30 days by looking at market movements in interest rates and stock prices. That sort of data mining tells us absolutely nothing. I could just as well say that stocks rose strongly in the 6 months after May 2013, and my 6 months would be just as arbitrary as your 30 days. In any case, this wasn’t “disruption”; this is how normal markets behave. Why should the Fed care?

John Hall

Jul 21 2022 at 10:43pm

There’s nothing magic or special about 30 days Scott. That’s just the acknowledged period where the “taper tantrum” happened. The evidence is that’s what people referred to it as the time. I don’t recall “taper tantrum” being a term used in my macro classes at school. My post was about looking at the mechanism that the “taper tantrum” occurred in the market. Your post argued that long-term bond yields rose. I argued that long-term yields rose because of movements at the shorter end of the curve, which happens to be more influenced by monetary policy. I also provided some evidence that market expectations of future Fed policy changed significantly over this one month period. To me, it is consistent with a story that market participants re-evaluated Fed policy (most likely in my view due to the way they view the Fed’s reaction function). I don’t have a theory or model to explain why it only lasted 30 days or so, other than to note that equity markets began to stabilize a few days after the Fed meeting when Bernanke reiterated that they would be data dependent.

Whether the Fed should care or not is a different question. What matters is if the Fed has moved markets the way they intended to or not. If the Fed communicates in a way that moves markets more aggressively than they intended, then is that a good thing or not? If the Fed’s communication is inconsistent with their goals, then that’s obviously a bad thing.

Spencer Bradley Hall

Jul 20 2022 at 10:35am

re: “Macroeconomics is full of myths” Amen.

Link:

Fact Check: Was 2013’s ‘Taper Tantrum’ Actually So Tumultuous? | MarketMinder | Fisher Investments

It is now widely recognized in retrospect, that N-gDp targeting (“timed properly”) should have been deployed to counter excessive monetary expansion in the 1st qtr. of 2021. A N-gDp futures market in the 1st qtr. of 2021 would have definitely shown policy was too loose (because of any traders’ quick response to “The American Rescue Plan Act of 2021”).

I didn’t figure it out because Jerome Powell eliminated required reserves. And I didn’t back test the new time series (which vastly exceeded all pervious time periods).

Spencer Bradley Hall

Jul 20 2022 at 11:22am

Randal Quarles re: “you’ve got to telegraph that well in advance”

The “taper tantrum” represents the activation of monetary savings (where S = I), where the FDIC reduced deposit insurance for unlimited transaction deposits to $250,000.

QE3 didn’t expand the volume of money (inflationary) as much as it increased the velocity (noninflationary) of circulation. Monetary flows, the volume and velocity of money actually fell by 80 percent causing the price of oil to trough in Jan 2016 by 70 percent during the same period.

It had a number of positive effects, a dramatic rise in the real rate of interest for saver-holders, R *, a drop in inflation, and an accelerated drop in the unemployment rate from 8.0% to 5.0% by Dec. 2015.

Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis, Inflation-Indexed (FII10)

Yet Janel Yellen, presumably looking at U *, decided to raise policy rates too early on 12/17/2015 from .25 to .50%.

Jeff

Jul 22 2022 at 2:23am

The obsession with not “disrupting” markets is absurd. Markets exists to trade risk. Trades happen literally at the speed of light now. If you happen to be holding the bag when something unexpected happens, then you can lose money. That’s why you get paid an expected return. There is no advantage at all to having s central authority “smearing out” the consequences of those unexpected events in time.

That the Fed worries that their glacial pace is “too fast for markets” is risible. In reality they are the ones causing market disruptions, because they have so much power but they are forcing the rest of the world to go at their slow slow speed and wait to see what they are going to do. I don’t see any way around the implication that this makes markets a lot less efficient and exacts a lot of needless costs.

Jeff

Jul 22 2022 at 2:48am

If there were a rudimentary machine learning algorithm in charge of monetary policy it would have detected the nascent signs of overheating and started gradually tightening sometime in February or March of 2021. In fact, markets started that process of their own accord right around that time. But they were *explicitly* slapped back in the press by multiple FOMC members. See https://www.wsj.com/amp/articles/fed-s-brainard-economy-remains-far-from-achieving-fed-job-inflation-goals-11614708361

I think that event is where you can mark the transition from Covid being a health crisis to becoming a financial crisis as well. In reality, markets were 100% right and doing what they were supposed to, while the Fed was 100% wrong, clueless, and out of touch. I don’t think these people realize anywhere near how badly they suck at their jobs and how much needless economic damage they cause. They are morons at the helm of a lethargic, obsolete institution who are geniunely stupid enough to think they can do the equivalent of flying to Mars using WW1-era dead reckoning.

Comments are closed.