There’s been a lot of recent discussion about the budget deficit, which is growing rapidly. Some argue that this is not a problem, while others see a crisis coming. I believe that both sides are wrong. I don’t believe the deficit will lead to high inflation, nor do I expect default. There may be some increase in interest rates, but probably not very large. Nonetheless, it is a problem.

All government spending must be paid for with taxes (if one treats inflation as a tax). But it does not all have to be paid for with current taxes—governments often borrow money and then future taxpayers repay those debts. In the standard model of public finance, you want to minimize the deadweight cost of raising a given amount of tax revenue over the long run. And the best way to do that is by keeping tax rates relatively stable over time. Thus you might want to run a budget deficit during wars, and repay the debt with surpluses after the war has ended and spending has decreased. Deficits help to smooth out tax rates, when spending is unstable.

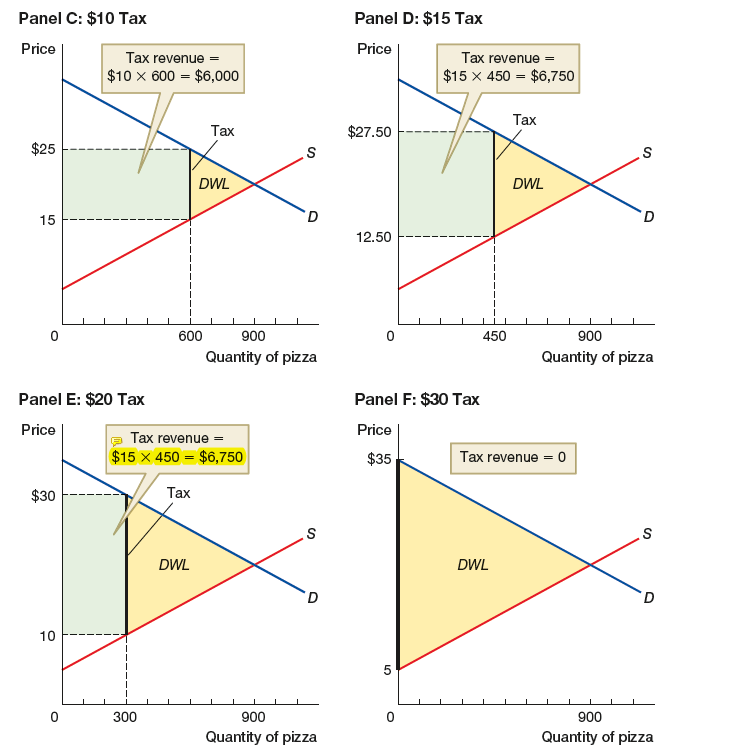

The following graphs show that the deadweight loss (DWL) from taxes rises with the square of the tax rate:

Thus if a 10% tax rate results in a deadweight cost of $1 billion, a 20% tax rate results in a deadweight loss of roughly $4 billion. It’s better to have a 10% tax rate every single year, rather than alternating between a 20% tax rate one year, and then 0% the next. Budget deficits are good if they help a country to smooth out tax rates, and bad if they lead to more unstable tax rates. Thus budget deficits are usually good during wars and depressions, and bad during booms. As an analogy, borrowing by individuals is good if it helps to smooth out consumption over time, as there is diminishing marginal utility to increased consumption at a point in time.

One also needs to account for the fact that in a growing economy the government can support a gradually increasing national debt. This is especially true for the US, which produces low risk securities that are valued all over the world. Even so, there are limits to how large that debt should be. And if you are a Keynesian who believes that the world should have a lot more Treasury debt (a good problem to have!), you should favor issuing that new debt during the next recession, not right now.

One reason I worry about the recent increase in the budget deficit is that I expect higher tax rates in the future–closer to European rates. (I hope I am wrong.) If I am correct, then our deficits will cause the already expected increase in tax rates by mid-century to be even steeper than otherwise, which will slow the economy in the future. This is especially bad if you buy Tyler Cowen’s argument that the welfare of future Americans is just as important as the welfare of current Americans.

When it comes to government borrowing, people disagree about almost everything: Ricardian equivalence, the relationship between “r” and “g” (interest rates and growth rates), MMT, Fed independence, Fiscal Theory of the Price Level, Keynesian stimulus, crowding out, intergenerational burdens, the “twin deficits” hypothesis, and a hundred other theories.

But taxes are bedrock to this debate. I know of no economic model that denies that it’s best to smooth tax rates over time, at least to some extent. You can argue about where we are right now, whether future taxes will have to be higher or lower, but the value of smoothing tax rates is almost undeniable.

PS. High-powered money creation (printing currency) pays for only a trivial portion of government spending, and money creation is also a sort of tax, as it dilutes the value of existing currency notes. Bank reserves at the Fed now pay interest, and hence from a public finance perspective are part of government borrowing, not money creation.

Today, when people talk about money creation as a way of financing federal spending, they are talking almost exclusively about printing $100 bills, even if they don’t understand that this is what they are talking about. The growth in high-powered money is overwhelming composed of “Benjamins”.

PPS. The optimal size of the national debt is very hard to estimate, as it’s hard to predict future interest rates and future growth rates for the economy. One way to think about the politics of the past decade is as follows. After the Great Recession, it became clear that the “new normal” of interest rates was lower than before. This meant that the optimal size of the national debt was now larger than before. Sharply increasing the debt is LOTS OF FUN. The GOP decided not to allow President Obama to take credit for the fun times, and instituted austerity in 2013. Then, when President Trump was elected, the GOP immediately decided that it was the right time to START THE PARTY.

Of course I’m half-joking here. But only half.

READER COMMENTS

Benjamin Cole

Mar 28 2019 at 12:30pm

Why did Ben Bernanke advocate money-financed fiscal programs for Japan in 2003 ? Did Ben Bernanke know he was only advocating the printing of paper ¥10,000 notes? Would Ben Bernanke agree with this assessment of his policy advice?

Suppose the economy is moving into deflation or is already in deflation. Then does resort to money-financed fiscal programs result in an “inflation tax?” Suppose the amount of money financed fiscal programs is enough to offset deflation, but not generate much inflation. Does that still qualify as an inflation tax?

Why is the Treasury printing money to execute a money-financed fiscal program inflationary, but the endogenous creation of an equal amount money by banks not inflationary?

Benjamin Cole

Mar 28 2019 at 12:40pm

Germany and Japan can already borrow at 0% interest, or so close you can hardly tell the difference. Should they tax citizens or issue permament bonds at 0%?

David S

Mar 28 2019 at 11:52pm

I’m on the fence about ideal debt ratios for governments, but I do believe that in general is someone offers you an unsecured loan at 3% you should probably take it. It is not hard to beat a 3% rate of return.

The real question is why the government doesn’t take out a $200T loan and invest it in the SP500 – and then we never have to pay taxes again! (I kid, I kid!)

Thaomas

Mar 29 2019 at 7:27pm

Higher tax rates in the future may be undesirable, but they need not lead to slower growth if the are levied with retrogressive taxation of consumption, not income. The could even be associated with higher growth if the deficits are incurred in investments that have positive NPV’s but negative fiscal impacts.

Comments are closed.