When macroeconomists talk about wage stickiness, they are generally referring to nominal stickiness. Because nominal wages are slow to adjust, a sudden and unexpected change in NGDP will usually impact employment, often in a sub-optimal fashion.

It’s possible to construct a variable called “real wages”, but I don’t view that as a useful concept. This is partly because (like Keynes) I don’t view inflation as being a particular useful concept, except perhaps when trying to come up with ballpark figures for long run changes in living standards. The problem is not so much that inflation figures are wrong; it’s not even clear what inflation is supposed to measure.

Here’s Tyler Cowen:

The restaurant used to pay you $13 an hour, now they pay you “$13 an hour plus p = ?? of Covid-19.” That new wage is a lower real wage.

That’s a defensible claim, if you define “inflation” in a certain way. But it’s also an example where the nominal wage is “sticky”, and hence this example has no bearing on “sticky wage models of the business cycle”. Again, it’s nominal wages and nominal GDP that matter, ignore real wages.

Tyler’s post is entitled “Real wages are flexible now”. But the post does not contain any supporting evidence for that claim. A change in the real wage is not evidence of increased flexibility.

For example, real wages rose sharply in 1930. Does the big change in real wages in 1930 show that real wages were increasingly flexible? No, they rose because prices fell while nominal wages were fairly stable. A flexible real wage is one that moves toward equilibrium, not one that randomly moves around due to some price level shock even as nominal wages are fixed. As an analogy, if The Soviet Union had raised the official price of bread from one ruble to two rubles, it doesn’t mean that bread prices are becoming more flexible, just that they are fixed at a different level.

I expect unemployment levels to rise to new and scary heights, and yes I do think the government should do something about that. But if you are analyzing the status quo with “a sticky wage model,” that assumption is probably wrong. Even though it is usually correct.

It’s true that sticky wages are not the reason why unemployment is about to surge much higher. We are facing an unusually large “real shock.” Nonetheless, nominal wage stickiness remains very relevant, as it is quite likely that 12 months from today we will have an elevated unemployment rate due to sticky nominal wages and lower than trend NGDP. I hope I’m wrong, but the financial markets seem to view it as a very real threat.

READER COMMENTS

Mark Z

Mar 28 2020 at 6:35pm

“$13 an hour plus p = ?? of Covid-19.”

What is that equation supposed to mean? What’s p?

I don’t know if I’ve heard of the idea of real wages being sticky in their own right, other than due to nominal stickiness. And if someone found evidence that they were, I’d wonder if they’re not just likely miscalculating real wages. As you say, inflation is hard to define let alone measure.

Scott Sumner

Mar 29 2020 at 1:09am

P means probability

Mark Z

Mar 29 2020 at 2:09am

Oh, probability of getting coronavirus. Got it.

Daniel R. Grayson

Mar 29 2020 at 8:57am

I don’t get it yet. What would it mean to add 13 dollars per hour to a probability? They aren’t measured in the same units. Why would one do that?

Robert EV

Mar 29 2020 at 11:45pm

If I pay you in three ducks and two bolts of cloth they are not in the same units, but if I suddenly only offer to pay you in three ducks you’ll likely ask for the two bolts of cloth as well.

Robert EV

Mar 29 2020 at 11:53pm

A better example would be applying to night clerk at two 7-11 convenience stores. One in a sketchy neighborhood, one in a safer neighborhood. The sketchy one is a shorter commute from your home. You are tendered the same minimum wage offer from both convenience stores. Which offer would you choose?

Dylan

Mar 28 2020 at 6:53pm

I’ve always been a bit skeptical of nominal wage stickiness, even though I know there is a fair amount of data that supports it, but it just goes so against what I see in my world. Over the last two weeks I’ve spoken with a bunch of people who had their nominal wage cut almost immediately at the start of the crisis, and accepted it happily as the alternative was being laid off. A prominent VC told me a few days ago they are asking all their portfolio companies to reduce salary compensation by ~30%, and the preferred way is to minimize layoffs and instead do it through salary reductions (that are hopefully temporary) My nominal wage decreased during the last recession too. I realize that minimum wage laws prevent full adjustment, as do things like union negotiated wages, but in the more normal parts of the world is rapid nominal wage reduction really that rare?

Scott Sumner

Mar 29 2020 at 1:11am

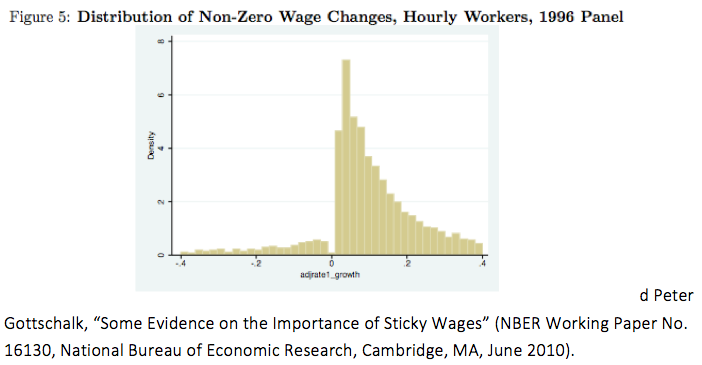

My nominal wage is downward sticky. Take a look at the wage change distribution at the bottom of the post, and try to explain it without wage stickiness.

Dylan

Mar 29 2020 at 8:06am

Is that stable over time? Theoretically, my intuition is that nominal rigidity should have lessened over time with lower percentages of people working in jobs where wage is part of a contract, and higher percentages working in gig and service economy jobs where overall wages have more flexibility.

Empirically, this research in Washington State from 2005-2015 shows that at least 20% of job stayers received a nominal wage reduction year over year.

Dylan

Mar 29 2020 at 9:25am

My last one of these before I go and do real work today. I swear that I’m not trying to cherry pick here, just looked for recent papers that discussed empirical evidence on nominal wage stickiness, and these were the first ones I found that actually tried to look at the data and not just assume wage stickiness.

This one looks at data across a number of countries using payroll records and pay slips. The relevant portion:

Scott Sumner

Mar 29 2020 at 2:16pm

There’s a difference between wage stickiness (slow to change) and wage rigidity (cannot be changed.) Wages are not rigid, and do adjust in both directions. But more slowly than NGDP.

Dylan

Mar 29 2020 at 3:48pm

I mean, I agree that wages are sticky over some time period. For most people, they’re obviously not going to adjust on a daily basis, but anecdotal observation is showing that they are adjusting pretty quickly in the face of this real shock. The data I’ve linked to seems to show that even during periods of non-crisis, about 20% of people have wage reductions over the course of a year, even while staying in the same job. That seems pretty significant, no? Honestly, when I went looking this morning, I was expecting overwhelming evidence showing downward wage stickiness, that was certainly the impression I took away from my macro classes, so I was pretty surprised to find fairly limited empirical support.

Scott Sumner

Mar 30 2020 at 2:59pm

I don’t agree that 20% of workers have nominal hourly wage cuts during a given period, not even close. Perhaps their weekly wage falls due to less hours worked, but that has very different implications.

Dylan

Mar 30 2020 at 4:10pm

Agree that there is a big difference in having hours cut vs. a nominal hourly wage cut. However, I think it is important to point out that it appears the data sources for both papers includes salaried as well as hourly workers. Surprised that both sources, using different data sources, time periods, and regions, also are around the same 20% mark for the number of employees seeing wage cuts over the course of a year.

Like I said, was greatly surprised to see this. The most I was thinking I might see was a decrease in wage stickiness over time. However, I don’t have full access to the Washington State paper, so maybe I’m misinterpreting something from the findings. Would be interested to see more empirical data that supports the wage stickiness hypothesis.

Dylan

Mar 29 2020 at 8:36am

There’s also an interesting chart at the top of page 9 from this paper showing wage changes from 1980-2014, and while it shows an asymmetrical distribution, it’s not that asymmetrical. It differs from the previous paper I linked to, in that this one includes job changers, not just people that had decreases while staying in the same job. Still, seems to provide some evidence that wage stickiness might not be quite as prevalent as some models assume. At least in areas where there aren’t other factors locking in wage rigidity.

Dylan

Mar 30 2020 at 4:50pm

Took another look at the Elsby paper linked to above. They do a review of the literature, including the Vigdor paper from Washington State that I don’t have full access to, and they mention this in regards to cuts in hourly wages:

When they are able to breakdown earnings in other countries at the hourly level the results are similar. Would love your thoughts on this paper when you have a chance, since it seems like a pretty good review of the empirical data we have on wage stickiness.

Matthew Waters

Mar 28 2020 at 9:22pm

I don’t know how much stock I would put into TIPS spreads and stock markets right now for post-2021 NGDP. TIPS show a lower break-even inflation rate when TIPS bonds trade lower due purely to illiquidity. Arbitraging the difference requires large amounts of leverage and both large brokers and hedge funds have been in a bad position due to large cash withdrawals.

AMT

Mar 29 2020 at 12:59am

It seems a lot more persuasive to me that wages are EVEN STICKIER than someone might have originally thought, if some significant work-environment change led to…ZERO… change in wages, along with a corresponding massive change in the economic environment. Or maybe the economy weakened EXACTLY as much as the risk of catching Covid-19 increased?…You’d have to be a very massive proponent of “non-sticky wages” to think such a ridiculous thing.

“”WAGES aren’t sticky, because wages remain IDENTICAL, but other aspects of work have changed!”

GENIUS! The whole point is that we inefficiently alter other aspects of compensation or work environment instead of more efficiently simply adjusting wages. This is utter stupidity by conflating wages with work environment and total compensation.”

You’d have to be mainlining Covid-19 concentrate to get high enough to think that evidence of EXTREME WAGE STICKINESS, means wages are less sticky than you otherwise thought. (facepalm)

Daniel Klein

Mar 29 2020 at 3:21am

I commented at MR on Tyler’s post, here.

Thaomas

Mar 29 2020 at 6:49am

Why do you think that the Fed will again fail to maintain at least pre-crisis trend growth in NGDP?

Philo

Mar 29 2020 at 9:49am

Because that will require the Fed to engineer high inflation, and its mandate–by law and by public opinion–is (mainly) to produce price stability.

Thaomas

Mar 30 2020 at 7:53am

Do you mean that the Fed estimates that only “high” inflation will keep aggregate demand growing at the real growth maximizing rate and that “high” means anything greater than 2% CPE?

Thomas Hutcheson

Mar 30 2020 at 8:02am

Why do we talk only about wage stickiness? Aren’t interest payments, rents, prices of inputs from a firms’s suppliers less flexible downward than upward in response to changes in NGDP? Wasn’t it Jacob Viner who held up a dollar and offered to purchases the entire real output of the economy if prices fell enough?

Comments are closed.