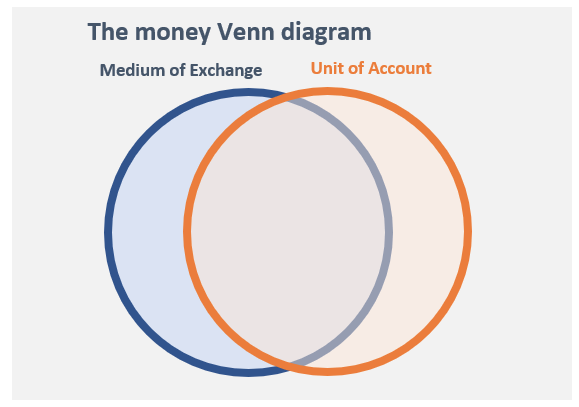

JP Koning has a proposal for simplifying the teaching of basic monetary economics. He starts with this Venn diagram:

Which he explains as follows:

Monetary economists such as Nick Rowe and George Selgin have proposed, and I concur, that we just chuck store of value from the definition of money.

But we are still left with two useful definitions for money, unit of account and medium of exchange. Which gets us to the money circle.

Note that the two circles in the diagram, medium of exchange and unit of account, don’t perfectly overlap. About 99% of the time the things we use as media of exchange are also the things we use as a unit of account. So the contents of our wallets or our bank accounts, dollar banknotes and dollar deposits are functionally equivalent to the $ units displayed in signs in grocery aisles.

But for the remaining 1% of the time, the unit of account and medium of exchange are separated. The idea of a separation is tough to get one’s head around. Luckily we’ve got a nice example. In Chile the prices of many things, particularly real estate, are expressed in terms of the Unidad de Fomento. But no Unidad de Fomento notes or coins circulate in Chile. It is a purely abstract unit of account.

I have a slightly different view. Because I define “money” as the monetary base, and because most base money is held as a store of value, I view that use as more important than the medium of exchange role. Nonetheless, I’d also drop “store of value” from the key characteristics of money, and just go with “medium of account”, where the medium of account is defined as the good in which other goods and labor are priced. In Chile, peso currency notes (and bank reserves) probably best meets that definition. Here’s Koning again:

The differences between Chile’s monetary system and those of other nations only emerges when we begin look at the unit in which goods are priced. Most nations have one unit-of-account, but Chile has two. While many Chilean prices are expressed in terms of the peso, or P, a broad range of prices are expressed in an entirely different unit, the Unidad de Fomento, or UF. Real estate, rent, mortgages, car loans, long term gov securities, taxes, pension payments, and alimony are all priced using UF. As examples, this real estate website sets prices in UF terms, and this car rental business levies insurance in UFs. On the other hand, wages, consumer good prices, and stock prices are expressed in peso terms.

In the end, I see no reason to focus on money’s role as a medium of exchange. Money is important because the nominal prices of goods, services and labor are priced in money terms, and because those prices are sticky. Thus when a shock to the supply and/or demand for money changes its value (i.e. its purchasing power), it will cause disequilibrium in the markets for goods, services and labor.

[It might also cause a financial crisis. But not necessarily in Chile, where financial contracts are not priced in terms of ‘money’ as I define money. Chilean financial contracts are not denominated in peso terms.]

The easiest way to teach money to students is with a supply and demand model for the medium of account (which might be gold or cash), where the value of money is defined as 1/Price level, or better yet 1/NGDP. All that’s left is to explain how and why the supply and demand for money changes over time. That can’t be so hard!! (Just kidding.)

HT: David Beckworth

READER COMMENTS

Arnold Kling

Dec 10 2020 at 6:58pm

You think this helps???

“Base money” is well defined. Fine.

But trying to treat a “medium of exchange” as the same thing as a “medium of account” is too weird for me. It’s like saying that a 12-inch ruler is the same thing as a foot. One is a physical object and the other is a concept.

Scott Sumner

Dec 10 2020 at 7:28pm

I’m not saying that the two concepts are identical; I’m saying that what matters is the medium of account, even if the medium of exchange is different.

It just so happens that in most countries, maybe all, the two are nearly identical. But my point is that money matters because it’s the medium of account, not because it’s the medium of exchange.

Perhaps you are thinking of “unit of account”, which is an abstract concept. Medium of account is no more abstract than medium of exchange.

I don’t follow your analogy with rulers and feet. The usual analogy is to imagine if the length of “a foot” was constantly changing over time, in which case you’d have measurement inflation or deflation.

marcus nunes

Dec 10 2020 at 7:10pm

Scott, 8 yrs ago the MOE/MOA discussion took place. My example of Brazil brought attention to the country´s temporary MOA (akin to Chile´s UF – I don´t know why they have kept it for so long).

https://thefaintofheart.wordpress.com/2012/10/31/two-kinds-of-money/

Scott Sumner

Dec 10 2020 at 7:30pm

Interesting.

Arnold Kling

Dec 10 2020 at 11:05pm

I have never heard the expression “medium of account.” The first time you used it in the post I thought it was a typo or a slip of some sort.

When I think of accounting, I think of writing down entries in a ledger. A ledger is the medium through which an account is presented. But then you talk about the supply of the medium of account. Surely you do not mean the supply of ledgers.

So until I understand what the phrase means, I cannot say that I find this at all clarifying.

Scott Sumner

Dec 12 2020 at 1:28am

Sorry, I thought “medium of account” was a well known term. It means the good in which other goods are priced. Some people use the term “numeraire”.

Back in 1920 is was gold, and today it’s base money.

If wages and prices were measured in zinc terms, and nominal prices were sticky, then I’d devote my whole life to studying the market for zinc.

Ahmed Fares

Dec 11 2020 at 1:10am

re: “medium of account” versus “unit of account”

Rodger Malcolm Mitchell had a post out today with this true or false question:

Question: A dollar bill is a form of money. ________

Answer: False. A dollar bill is a title to a dollar. Just as a car title is not a car, and a house title is not a house, a dollar bill is not a dollar. It is a non-interest-paying bearer instrument, that indicates the bearer owns a dollar.If you happen to own a bond, and you have a piece of paper in your safe deposit vault, that piece of paper is not in itself, a bond. It is just evidence you own a bond.The actual dollar (or bond) is merely a number on a balance sheet. Numbers, dollars, and bonds have no physical existence. They all are merely data. One day, the dollar bill may become totally obsolete, and we will pay all our debts online with invisible, non-physical dollars.

George Selgin

Dec 11 2020 at 10:52am

“The actual dollar (or bond) is merely a number on a balance sheet.” Tell it to someone running on his or her bank!

Scott Sumner

Dec 12 2020 at 1:38pm

You said:

“Answer: False. A dollar bill is a title to a dollar. Just as a car title is not a car, and a house title is not a house, a dollar bill is not a dollar.”

That’s amusing. See what happens if the title to your house is accidentally destroy in a fire. Now see what happens if a dollar bill you own is accidentally destroyed in a fire. Do you still have the house? Do you still have the dollar?

George Selgin

Dec 11 2020 at 11:08am

“In the end, I see no reason to focus on money’s role as a medium of exchange.” Well, for starters, it would allow you to define it the way most economists have done for some time now, that is, as including bank deposits of various kinds, and not just the monetary base.

Of course this is a matter of semantics, but that doesn’t seem to me to make it unimportant. Your attempt to revert to an old-fashioned definition reminds me of Austrians who still insist on defining “inflation” as an increase, not in P, but in M. I believe instead that when it comes to definitions, whichever prevails is therefore (w/ rare exceptions) best.

Nor is this just a question of what most economists choose to treat as “money” for statistical and other purposes. It goes for common usage also. As I pointed out recently on Twitter, when I was in Brazil in ’92 (or thereabouts), the USD had come to be widely used as a MofA, while most actual payments were still made using cruzeiros at the going USD/cruzero rate. Few (indeed, hardly anyone) then regarded the USD as Brazil’s “money.” Instead, that term was used to refer to the actual MofE. I believe this has been so in most cases where monetary separation occurs.

Scott Sumner

Dec 12 2020 at 1:22am

George, You said:

“Your attempt to revert to an old-fashioned definition reminds me of Austrians who still insist on defining “inflation” as an increase, not in P, but in M. I believe instead that when it comes to definitions, whichever prevails is therefore (w/ rare exceptions) best.”

I’m afraid you are wrong on this point. I accept your claim that it’s silly to define inflation as an increase in the money supply. But there are multiple well known definitions of money, including the base, M1, M2, etc. I almost always clearly specify when I am talking about the base, and when I am talking about the broader aggregates. So I don’t believe there should be any confusion.

On your other point, are you saying that wages and prices in Brazil are mostly denominated in US dollar terms?

George Selgin

Dec 12 2020 at 6:18am

Scott, you are perfectly clear; I didn’t mean to suggest otherwise. But I do think your definition of money here as B is not standard today as it once was. Maybe I’m the outlier!, but I used to teach my students that while M1, M2, etc. are measures of the public’s money holdings, B is not. Only that part of it consisting of public currency holdings is so. The remainder, reserves, belongs to banks.

Of course I know you know this. I point it out only to explain why I consider treating B as just one of several alternative measures of M to be unorthodox.

George Selgin

Dec 12 2020 at 6:37am

On Brazil, I was referring to the situation in 1992. Many (not all) sellers were then posting prices in USD, though payments were made in cruzeiros. This was mainly to avoid menu costs. My impression is that this is the main reason for separation of functions in modern times.

I wonder what you’d say about the British case when the guinea was the upper class UofA and the pound was for the rest. Two distinct monies, or just one?

Scott Sumner

Dec 12 2020 at 1:49pm

I have no problem with people claiming there are two monies in a given country, or two media of account. But I’d say the one that is important for issues like inflation and business cycles is the one in which most wages and prices are denominated.

I’ve never really given much thought to a case where a significant share of wages and prices are quoted in two different units of account. According to JP Koning, even in Chile the wages and prices are generally in pesos. How about wages and prices in the UK when the guinea was used? BTW, As I recall there was usually fixed exchange rate between the pound and the guinea, is that right?

As far as the monetary base, I have no objection to people saying that M1 is money and the base is not. Then I’ll just relabel myself “monetary basest” and discard the label “monetarist”. Leaving that term for you and Nick Rowe and David Beckworth and anyone else who thinks I’m wrong in ignoring the medium of exchange role of money.

Now my theory is not “Monetary policy determines NGDP”, it’s “Monetary base policy (both supply and demand) determines NGDP”. That’s fine.

JP Koning

Dec 11 2020 at 11:51am

Hi Scott,

You say that in Chile, peso currency notes (and bank reserves) probably best meet the definition of medium-of-account.

But let’s say Chileans were to start setting wages and goods prices in UF terms, not pesos. What would you describe as the medium-of-account?

Scott Sumner

Dec 12 2020 at 1:18am

Good question. In that case, I’m not sure there would be a medium of account. But I don’t know enough about the system to say that with any confidence.

Benoit Essiambre

Dec 11 2020 at 12:52pm

Instead of striking “store of value” from the definition of money, I would strike it from the purpose of money.

Being a store of value is an unfortunate consequence of being the medium of account/exchange but it’s nevertheless a defining characteristic.

We can’t underplay this characteristic as it is money’s most dangerous aspect. When central banks turn fiat into too good of a store of value, it crowds out real investment as a store of value, indirectly incentivizing and subsidizing economic inactivity at an economy wide scale.

It pushes the world towards everyone hoarding government promises and few building things to be purchased with these pieces of paper.

It puts the world in a massive prisoner’s dilemma where the first ones to build real stuff are forced to lose.

Being too good a store of value is where money can cause civilization collapse. Money being a store of value should haunt your dreams.

Mike Sproul

Dec 11 2020 at 2:11pm

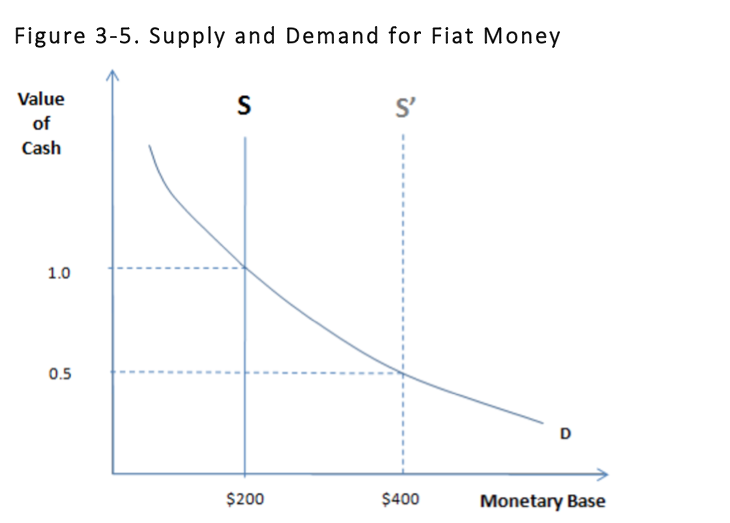

Figure 3.5 sweeps aside a million important issues, but I’ll focus on one:

Start with a gold standard, where the dollar is both backed and convertible (Say, at $1=1 oz of gold). Then suspend convertibility, with the money-issuer’s assets unchanged. At this point, the dollar is backed and inconvertible. But fiat money, by definition, is unbacked and inconvertible. Believers in fiat money make the mistake of claiming that ‘inconvertible’=’unbacked’.

Scott Sumner

Dec 12 2020 at 1:24am

But how does that relate to figure 3.5?

Mike Sproul

Dec 12 2020 at 12:03pm

It relates because

(1) Fig 3.5 presumes that the money in question is fiat money, when a good argument can be made that the money is backed but inconvertible.

(2) Fig 3.5 presumes that the value of money is set by the supply and demand for that money, rather than the plausible alternative that the value of money is determined by the issuer’s assets and liabilities.

Scott Sumner

Dec 12 2020 at 1:55pm

The value of money is determined by supply and demand, the only question is whether the “backing” as you call it (a concept I don’t view as important in the US) has any bearing on the demand.

If I’m not mistaken, I think you are saying that if the Fed doubles the base and the increase is fully backed with assets like T-bonds, then this backing causes people to be willing to hold the extra money at the existing price level, and hence the demand curve shifts to the right by an equal amount–due to confidence in the backing of the new money.

I don’t believe that’s the case when interest rates are positive, and probably not even when rates are zero (at least not in the long run).

Mike Sproul

Dec 12 2020 at 2:49pm

Supply and demand is a fine model for apples and oranges, but not for financial securities. Imagine a slip of paper that reliably promises “IOU 1 oz of gold”. The demand curve for those IOU’s is a horizontal line with height of 1 oz, and so is the supply curve. Supply and demand did not determine the 1 oz price. Rather, the 1 oz. price was determined by the assets and liabilities of the issuer, which in turn determined the shapes of supply and demand. Modern paper money is the same. It’s value is determined by the assets and liabilities of its issuer (just like stocks, bonds, etc), but it can give a false impression of having been determined by supply and demand.

Yes, if the Fed doubles the supply of paper dollars from $100 to $200, then the Fed’s backing assets will rise from (say) 100 oz to 200 oz, and it will remain true that $1=1 oz. It’s important to add that the extra $100 would only issued if people want the dollars badly enough to hand over 100 oz. worth of assets in exchange.

Scott Sumner

Dec 13 2020 at 6:00pm

When interest rates are positive, the demand for base money is unit elastic with respect to the value of money (1/P). To get people to hold twice as much cash in nominal terms, you need to have the price level double. That’s why open market purchases are inflationary.

When deciding how many US dollars to carry in their wallets, no one cases about the “backing” of currency notes. All they care about is purchasing power.

Mike Sproul

Dec 13 2020 at 7:58pm

You could just as well claim that nobody cares about the backing of shares of GM stock. It’s true that some investors know little or nothing about GM’s balance sheet, but look through any finance text, or watch any stock market analyst in action, and you will see that backing matters for GM shares, and no competent professional would be caught dead drawing supply and demand curves for GM shares.

Continuing the stock/money analogy, the “demand” for GM shares is horizontal at the market price, as is the “supply”. No serious financial economist would claim that the demand for GM shares is unit elastic. Similarly, if GM issued and sold new shares, so as to double the number of shares outstanding (while causing a commensurate rise in GM’s assets), nobody would claim that GM’s share price would have to drop by half in order to induce people to hold the new shares.

Scott Sumner

Dec 14 2020 at 1:06pm

The empirical evidence suggests that backing for GM shares matter. The same evidence suggests that backing for base money doesn’t matter in the US.

Mike Sproul

Dec 14 2020 at 4:34pm

Here’s a link citing papers by Calomiris, Bomberger and Makinen, B. Smith, T. Cunningham, etc., showing cases where the backing theory fits the data better than the quantity theory.

http://www.csun.edu/~hceco008/nofiatmoney110807.doc

Not to mention other episodes, like, for example, when the Fed tripled both sides of its balance sheet without causing inflation.

Malthus John

Dec 11 2020 at 7:38pm

Unfortunately, when we dumb things down to make it easier to teach, we usually just end up with inferior learning. “Keep it simple, but not too simple.”

What knowledge are you lopping off?

I notice you’ve already left out one of the traditional legs of the defining characteristics of money: the standard of deferred payment. To then remove the store of value from the discussion means you’ve eliminated all traces of time, and the fundamental effects it has on what we consider to be money.

I suggest, rather than trimming you might consider going even deeper. Draw out the connections between the 4 properties, and how they relate to & reinforce each other. How time & space play important roles of limits and constraints. How one money interacts with money from another issuer, and with what consequences for these 4 attributes.

We’re entering a time when there will be 1000’s of new currencies, and the Fiatanosaurus Rex may be on the endangered species list. We should be working on a general theory of money to replace this special case.

Scott Sumner

Dec 12 2020 at 1:57pm

I certainly would tell students that money is used as a medium of exchange and a store of value. My point is that the role that deserves the most emphasis is it’s role as the medium of account. That’s where I’d spend 95% of my time.

Kurt Schuler

Dec 11 2020 at 10:32pm

Serving as a store of value is an important aspect of money. It’s the difference between the U.S. dollar and the Venezuelan bolivar.

Scott Sumner

Dec 12 2020 at 1:25am

Yes, it’s an important use of money. But the thing that makes money super important is its role as the medium of exchange.

Kurt Schuler

Dec 12 2020 at 5:19pm

Your statement that “the thing that makes money super important is its role as the medium of exchange” seems to contradict your desire to reduce money to the unit of account. Be that as it may, money has the most “moneyness” when it combines the unit of account, medium of exchange, and store of value functions. A unit of account not based on a reasonably good store of value gains few adherents in open competition, and sometimes, as in the case of countries that are heavily dollarized unofficially, a poor local unit of account loses out to a better foreign unit of account despite the advantages that national law gives to the local unit. Units of account based on different stores of value have different implications for the way prices adjust and, indeed, the efficiency of the price system itself.

Scott Sumner

Dec 13 2020 at 6:03pm

Here I was thinking about the US dollar. If something like cigarettes are used as money then you might want to spend more time on it special characteristics.

Lord Canes

Dec 12 2020 at 1:03am

Is modern macroeconomics imploding? What is money? It is disputed.

Are higher or lower interest rates inflationary? It is disputed.

You can win a Nobel Prize for efficient market theory in the same year they give out a prize for a method of beating markets over the medium-term (2013).

Is MMT valid? Why are conventional economists wrong for decades in succession on the direction of inflation and interest rates? No one knows.

Scott Sumner

Dec 12 2020 at 2:01pm

There’s no dispute over what the monetary base is.

That’s a meaningless question, like asking whether higher prices boost output. It’s what economists call reasoning from a price change.

Only the EMH theory was deserving; the Shiller model has not performed well in recent years.

MMT is based on a series of fallacies, as I pointed out in a more recent post. The EMH says economists are not able to predict the direction of interest rates.

Lord Canes

Dec 12 2020 at 8:03pm

Q: Are higher or lower interest rates inflationary? It is disputed.

A: “That’s a meaningless question, like asking whether higher prices boost output. It’s what economists call reasoning from a price change.”–Scott Sumner.

It may in fact be a meaningless question, but not to many of your professional colleagues.

My limited understanding is that “Neo-Fisherians” believe that lowering interest rates is ultimately disinflationary, and raising interest rates is inflationary while monetarists (at least certain stripes) hold the opposite.

Scott Sumner

Dec 13 2020 at 6:05pm

I have a new paper discussing why you should never reason from an interest rate change, if you are interested:

https://www.mercatus.org/system/files/sumner-critique-interest-rate-mercatus-working-paper-v1.pdf

This shouldn’t even be controversial; it’s EC101.

Mark Brady

Dec 12 2020 at 9:46pm

Scott writes, “BTW, As I recall there was usually fixed exchange rate between the pound and the guinea, is that right?”

Since December 1717 a guinea coin was worth twenty-one shillings. From what I can make out, the latest coinage of guineas took place in 1813, and guineas were withdrawn as everyday currency in 1816. Since then it was just a posh name for a pound and a shilling, the denomination in which lawyers and doctors charged their clients and patients. I know. I’m old enough to remember saving up my money to buy The Handbook of British Birds, all five volumes, for seven guineas!

Scott Sumner

Dec 13 2020 at 6:07pm

Thanks Mark. The British always make things complicated, don’t they? I can’t imagine the French having that sort of system.

But then that’s why Britain is a charming country.

Michael Pettengill

Dec 15 2020 at 5:56pm

This is nonsense.

Money must start with labor, and its zero sum complement, production.

Money is work done in the past, present, or future.

Gold, silver were long term stores of value because over thousands of years, the labor to produce marginal units was constant. They also are durable goods with utility that substitute for other products of work.

I was puzzled in the 80s by what I call free lunch economics. Free lunch economics rejects zero sum, and at least implies products can be produced without labor.

Further, it argues consumer incomes is unimportant, so a robot economy of robots building robots to produce will result in high gdp growth because production does not require consumption. If consumers do not work in the aggregate to produce exactly the quantity they consume, the economy can’t work.

Gold production is a collective action involving thousands on the smallest scale, million in the normal cash. Money measures the labor contribution of a million workers in a gold ring or gold bar.

But it all comes down to labor production, work.

If robots replace human labor, everything must be free, priced at $0.

Comments are closed.