Critics of the Biden administration’s Ukraine policies have pressed for major changes in the country’s energy policies to impair Russian aggression in Ukraine. Most notably, the critics seek a restart of the Keystone XL pipeline.

To date, the Biden administration has been unwilling to do that. If President Biden wants to help Ukraine by inflicting economic damage on Russia over and above what can be achieved by current sanctions, he should take the critics’ advice, and the sooner the better.

The Administration’s Case for Not Reversing Its Keystone Policy

When pressed by a reporter at a March 3, 2022 press conference, White House Press Secretary Jen Psaki staked out the Biden administration’s reason for opposing a policy reversal on the pipeline:

Ms. Psaki—and her boss—must have missed some key Econ 101 lessons. An announcement to restart the Keystone pipeline as soon as possible would put immediate downward pressure on current global oil and gasoline prices, which would reduce European countries’ dependence on Russian oil and increase their willingness to impose more damaging sanctions.

Ms. Psaki has clearly failed to understand how current and future oil supplies are interconnected through anticipated future oil supplies, prices, and profits. She understands that pump prices in February were 50 percent higher than when President Biden took office, but she and the President confidently deny the gasoline price hike has anything to do with the administration’s restrictive energy policy. She is also dead wrong on the impact of a Keystone-restart announcement on today’s gasoline prices.

The Tie between Current and Future Gas Prices

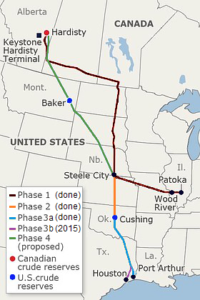

When the Biden administration took over on January 20, 2021, it immediately began a “war on fossil fuels” under its green agenda, heavily weighted toward substantially reducing U.S. greenhouse gas emissions. One of President Biden’s first acts was to terminate by executive order construction of the Keystone XL pipeline. He wrote, “Leaving the Keystone XL pipeline permit in place would not be consistent with my administration’s economic and climate imperatives.”[ii]

What Ms. Psaki and the President have overlooked is that termination of the pipeline construction reduced the anticipated domestic and global supply of oil in the future and, therefore, increased future oil prices above what they would have been (as economists Dwight Lee and David Henderson argued years ago[iii]). The hike in anticipated future prices likely caused producers in the United States and around the globe to hang on to their current oil reserves in anticipation of higher future profits. They can do this by reducing their current and future drilling, leaving their easily accessible known reserves in the ground, and holding on to a greater fraction of their stored output.

The resulting domestic and global market outcome from the pipeline cancellation? Higher current gasoline prices than Americans (and everyone else) have faced since President Biden first occupied the Oval Office.

If the Biden administration announced a restart of the Keystone pipeline, oil producers would reverse their thinking, because anticipated future oil prices would fall with the greater future supply at lower cost, which can be expected when the Keystone becomes operational. This means they could anticipate that they future profits would fall below levels previously anticipated. Producers could be expected to increase current market supply drawn from reserves, which would put immediate downward pressure on the current price of gasoline at the pump.

To the extent that current and future oil prices fall (or rise by less than otherwise) from the administration’s reversal of its current restrictive policy on oil, Russian President Vladimir Putin’s war machine would be impaired as its oil revenues decline. This means President Biden’s Keystone-policy reversal will add to the expected economic damage from the growing count of sanctions imposed on Russia by nations that span the globe. A Keystone-restart announcement would also dampen the decline in Americans’ real incomes suffered during President Biden’s first year in office, at least partially attributable to the administration’s energy policies.

Of course, the administration must include in its restart announcement guarantees that it will hold to its more lenient energy policies long enough for investors to recover their added current fossil-fuel investment in the Keystone pipeline and other drilling projects. This means that the Biden administration must be willing to postpone progress on its green goals, which it has been reluctant to do. If the administration doesn’t provide the needed guarantees for investors, it might as well not bother with a policy reversal and suffer the political consequences of what now appears to be an ever-rising pump price.

Conclusion

Granted, the administration and its green allies are committed to reversing climate change, and a reversal on the administration’s pipeline policy will likely delay the achievement of their emissions goals. However, the administration is now facing both practical and moral dilemmas. The United States and the world are witnessing an enormous and growing humanitarian crisis from Russia’s invasion of Ukraine that seems, at this writing (mid-March 2022), to be growing in its savagery.

Moreover, the Biden administration must now cope with the unfathomable designs of a power-obsessed autocrat who, if successful in Ukraine, could be emboldened to seek annexation of other nations, especially if the United States and NATO continue to be unwilling to risk starting a wider war by pulverizing the Russian army’s conventional war machine. The administration must now include in its green-policy calculus the prospects of growing greenhouse-gas emissions from an expanded war with, perhaps, the advent of World War III with nuclear exchanges.

[i] Press Briefing by Press Secretary Jen Psaki, March 3rd, 2022, James S. Brady Press Briefing Room, The White House, Washington, D.C.

[ii] As quoted by Rob Gillies, 2021. “Keystone XL Pipeline Halted As Biden Revokes Permit,” ABC News, January 20.

[iii]See Dwight R. Lee, 1978. “Price Controls, Binding Constraints and Intertemporal Decision Making,” Journal of Political Economy, Vol. 86, No. 2 (April 1978), pp. 293-301; and David R. Henderson, 2018. “Why Bryan Caplan Won His Gasoline Bet,” EconLib, February 14.

Richard McKenzie is an economics professor (emeritus) in the Merage Business School at the University of California, Irvine. His latest book is The Selfish Brain: A Layman’s Guide to a New Way of Economic Thinking (2021).

READER COMMENTS

Thomas L. Knapp

Mar 22 2022 at 12:49pm

It’s unclear what the price effect of Keystone XL would be.

Keep in mind that its purpose is to serve as an eminent-domain-powered corporate welfare subsidy to a (partially-state-owned) foreign company for the purpose of moving Canadian oil to US refineries and ports for export to third countries, not to increase supply in the US. In fact, it might decrease domestic supply to the extent that US refinery capacity goes to refining that oil to be sold elsewhere instead of refining oil to be sold here.

Globally, it presumably wouldn’t affect total oil supply much at all. The Canadian oil is still being extracted and exported abroad, just not via pipeline through the US.

Jon Murphy

Mar 22 2022 at 3:28pm

Recall that oil is a fungible, globally traded commodity. Crudely speaking, increasing its supply anywhere increases its supply everywhere. If Canadian oil is pumped through the United States, refined, and sold elsewhere, then that frees up oil that is produced and refined in the United States (or elsewhere) to be sold in the US.

J Mann

Mar 23 2022 at 10:54am

“Crudely speaking”

If we have to resort to puns, could we try to be a little more refined about it?

Jon Murphy

Mar 23 2022 at 11:17am

Sometimes my puns are sweet and sometimes they are sour.

J Mann

Mar 23 2022 at 11:53am

Given that no one can stop the pipeline of oil puns, I’m just going to do my best to stop glistening.

zeke5123

Mar 23 2022 at 2:50pm

I think this well of jokes is all dry.

Alan Goldhammer

Mar 22 2022 at 1:38pm

The amount of oil coming into the US from the Keystone XL, assuming it was completed, is negligible compared to the total world market. The countries in the Middle East can do more to influence oil prices than letting tar sand oil from Canada flow into the US. As noted by Thomas Knapp, the pipeline is a corporate welfare subsidy.

A more serious argument would be more electrification via nuclear power.

MikeW

Mar 22 2022 at 10:29pm

I don’t think I understand why you say it’s corporate welfare. The company has already spent billions of dollars on the pipeline, which is likely never to open.

Thomas Lee Hutcheson

Mar 22 2022 at 4:19pm

Keystone XL should be approved becasue it has an NPV >0.

Everything else is political posturing.

Dylan

Mar 22 2022 at 5:04pm

I think you’re missing one point, any announcement of Keystone restarting would have to be credible. For such a long-term and politically charged program, that’s difficult to do. I’d expect the market to heavily discount the odds of Keystone ever being completed, and therefore not have a meaningful impact on fuel prices over the short to medium term.

Richard McKenzie

Mar 22 2022 at 6:17pm

I must have been unclear to a degree in my argument. I never meant to suggest that a Keystone restart would itself immediately increase oil supply in the current market. I agree with Psaki that the pipeline is not now operational and it would take time to make it operational. My point is that the restart would change the anticipated oil supply in the future, which can affect expected future prices and profits—which, in turn, can cause current producers to adjust the allocation of their reserves between the current and future markets, which is how current gasoline prices can be dampened.

Of course, the extent of the effect on current prices depends not so much on the pipeline restart itself, but also the extent to which the restart would signal a broad reversal of Biden’s energy policies. I tee off from Psaki’s dismissal outright of a restart effect, because the pipeline is not now “operational.” She misses my points.

Dylan

Mar 22 2022 at 7:57pm

Hi Richard,

I think it was me that was unclear. I think that an announcement from Biden along the lines of “Given the extreme duress the current Russian aggression towards Ukraine has put on the American family, due to escalating fuel prices, I’m announcing that, starting today, I’m directing my administration to study the feasibility of relaunching construction on the Keystone Pipeline” would not be taken credibly by the market, because of course, even if construction was to start again today, it could just as easily be stopped tomorrow.

Your next paragraph suggests why, because any such statement would not be a broad reversal of the Biden energy policy. Biden cannot come right out and say this, but high fossil fuel prices are the main leverage point for encouraging that energy policy. Of course, a way to signal to the market that they will remain high, and won’t just fluctuate broadly due to geopolitics would be preferable for longer term planning, as short term prices don’t do a lot to spur longer term investment.

MikeW

Mar 22 2022 at 10:31pm

Since the Republicans already support it, the Democrats coming out for it would seem to settle the matter.

Ted

Mar 24 2022 at 6:16pm

By what magnitude would you expect this to lower gas prices?

My understanding is that Keystone XL would act as slight lowering in cost, as oil could be transported by pipeline instead of train. A slight lowering of cost for a slight fraction of the world’s oil seems unlikely to materially move gas prices today. It’s not like the oil can’t already be exported. And with high prices, it will be exported regardless of whether it’s by train or pipeline. Right?

Richard McKenzie

Mar 25 2022 at 5:24pm

In my short piece, I didn’t seek to present a quantitative estimate of the price effect of a Keystone restart. The thrust of the essay is to present arguments on how the Biden/Psaki argument that a restart would have no short-term price effect, which I grant is a modest ambition, is wrong. The effect could be small or consequential, depending on the extent to which Keystone restart would be assessed by the market as a reversal of the Biden’s restrictive energy policies.

I grant people that the effects of the restart might be muted by Biden’s ability to make credible assurances that his reversal will hold, which has an inherent problem: the reversal would cause the market to worry that there could easily be a reversal of his reversal. I wish I had had room to make these point clearer, but I hardly was oblivious to them.

Larry Feldman

Mar 26 2022 at 11:43am

If the price of oil in the U. S. is below $70 (give or take) producers pack up their gear and go home. The oil stays in the ground. If the government supports policies hostile to the oil industry, that sends a message to the future markets that no new oil is coming on line and the price of oil rises. Drillers go back to work. Eventually more oil comes on line and prices fall. But it seems like there are two conflicting ideas at work here. The price of oil has gone up so producers should be drilling but the Biden energy policy is so hostile to the industry that the futures’ market is encouraging them to keep the oil in the ground and wait for even higher prices. Further complicating that is the idea that they can only have those higher future prices as long as they never drill because as soon as they start producing more oil, the price will go down. So Biden says the problem is with the industry because they are not drilling and the industry says the problem is with Biden’s hostile policy which makes drilling now less profitable than drilling later.

Comments are closed.