A new NY Fed paper from Martin Almuzara, Richard Audoly, and Davide Melcangi has some interesting findings regarding nominal wages. This is their conclusion:

We estimate the latent persistent component of aggregate nominal wage growth by combining worker–level data with time series filtering and smoothing methods. This measure, which we label CoWI, is purged from noise and short–run fluctuations. We propose a novel approach to account for the monthly-to-yearly temporal aggregation present in CPS data. In a real-time forecast comparison, we show that it outperforms a random walk benchmark and, as such, that it can provide reliable signals for turning points in wage inflation. CoWI moves substantially during the three episodes of largest macroeconomic relevance in our sample: the 2001 and 2008 recessions, and the wage inflation episode of 2021. In all episodes, we find that changes in CoWI are driven by its common component. In accounting for these changes, no specific job or worker characteristics matters to a first order. Finally, our results suggest that the common component of CoWI seems especially important during inflationary episodes. It contributes more than 75% of the increase in aggregate nominal wage growth during the post-pandemic episode of inflation.

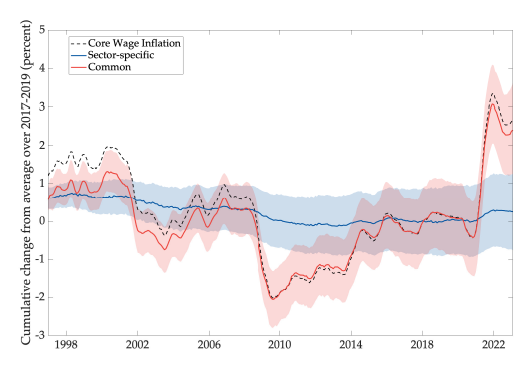

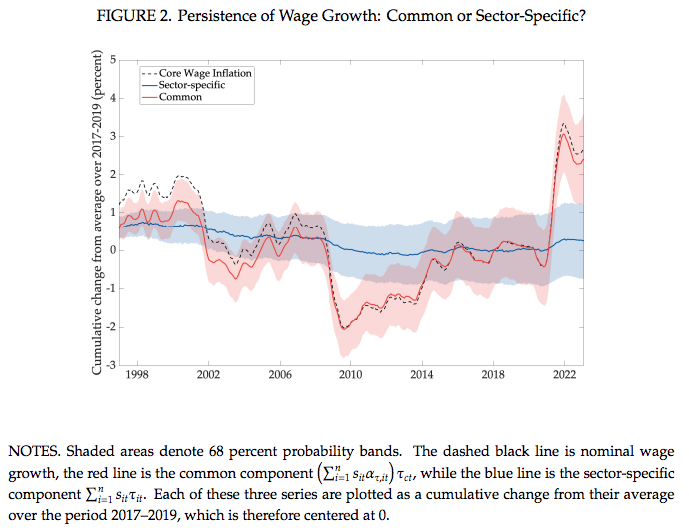

In my view, that common component is monetary policy (which can be proxied by nominal GDP growth.) Expansionary policy drives up almost all nominal wages, and contractionary policy reduces wage growth. In the following graph, you can see the effect on wages of the small undershoot of NGDP after 2001, the big undershoot after 2008, and the big overshoot after 2021:

If excessively high wages discourage employment, then why does unemployment tend to be high during periods of slow wage growth, such as 2009?

This puzzle is resolved if we recall that nominal wages are sticky, or slow to adjust to changes in equilibrium wages. Thus when slow NGDP growth after 2001 reduced equilibrium wage growth; the actual nominal wage growth fell more slowly, raising unemployment. When NGDP growth fell sharply after 2008, equilibrium wages fell very sharply. Although actual wage growth slowed a bit, the shock ended up pushing wages above their (rapidly falling) equilibrium value, creating high unemployment. After 2021, fast rising NGDP pushed equilibrium wages much higher. Actual wage growth sped up, but not enough to eliminate “worker shortages”.

This comment also caught my eye:

The estimated common factor matters even more during the 2021 inflation surge. We find that it accounts for at least 80% of the increase in CoWI over this period, regardless of the cross-sectional variable we use in the estimation. This finding suggests that a form of asymmetry might be at play between recessionary and inflationary episodes, with potentially more worker heterogeneity in downward than in upward nominal wage rigidity.

Just thinking out loud, I wonder if this reflects the varying degree of cyclicality across industries. Workers are very resistant to nominal wage cuts, which probably makes wages a bit stickier on the downside. In addition, rates of unemployment vary greatly between sectors during recessions, with much higher unemployment rates among factory workers than teachers or nurses. Perhaps workers are more willing to accept wage cuts in those sectors with high unemployment. During periods of expansionary monetary policy (fast rising NGDP), unemployment is fairly low in most sectors of the economy—thus not as much wage growth variation between sectors. In that case, wages rise rapidly across all sectors.

READER COMMENTS

David S

Jul 19 2023 at 12:50pm

I wonder what will happen moving forward, because although there are still a lot of “help wanted” signs out there, there are cooling trends on the overall job growth numbers. If persistent labor scarcity forces firms to compete on wage levels to retain staff then some degree of wage growth will persist–which is a good thing if NGDP growth is kept at a sustainable level. I’ll be optimistic and claim that things are stabilizing because job-hopping is exhausting and the current generation doesn’t have the expectations, or unions, of a 1970’s workforce that demanded 5% pay raises each year.

Notwithstanding the harm done between 2009 and 2014, the pandemic inflation surge could be viewed as a compressed version of events that occurred between 1950 and 1983.

spencer

Jul 20 2023 at 9:59am

There’s a shortage of workers just like there’s a shortage of houses. Something can be done about both problems. But it much more likely to get even worse.

Robert EV

Jul 22 2023 at 12:51pm

Wages for current employees are obviously sticky, but shouldn’t wages for new workers, as well as raises for current employees, be unstuck?

Jobs with historically high turnover should have better employment growth than jobs with low turnover (even in a period of recession when people tend to stick with all jobs for longer). Is this seen?

Is this seen? The examples you chose are also blue-collar versus pink-collar, which have additional socio-factors to consider beyond the solely economic factors.

Even child care?

Comments are closed.