Recent data and analysis show two interesting facts: (1) American manufacturing output has been falling for a year; (2) the Trump administration’s tariffs have reduced manufacturing employment. One chart and one new econometric study will help understand. As a bonus, we’ll also see that, as dangerous as a central bank is, an independent one has a major benefit that is too easily overlooked.

Of course, there is nothing sacred in manufacturing. Whether what is produced is a manufactured gadget or a doctor visit doesn’t matter except for the fact that the consumer got it who wanted it and was ready to pay for it. Note also that manufacturing employment does not matter as such. If people don’t work in manufacturing, they will work in whatever industry can provide consumers with what they want at a price better than the competition.

American manufacturing has stalled (at best) despite an official White House policy of promoting it. The Institute for Supply Management’s factory index fell in December for a fifth consecutive month (“U.S. Manufacturing Shrinks for Fifth Month, Signaling Weak Start to 2020,” Wall Street Journal, January 3, 2020). It was the lowest reading of the index (which comes from a monthly survey of American purchasing and supply executives) since June 2009. Another private manufacturing index, the HIS Markit’s purchasing managers index was not as gloomy, but not uplifting either (“Manufacturing Shows Stability in U.S., Asia,” Wall Street Journal, January 2, 2020).

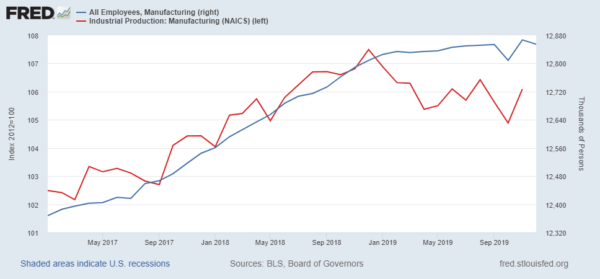

The latest hard data from the Bureau of Labor Statistics show the stagnation if not decline of manufacturing, as can be seen on the chart below. The changes date from late 2018 for output and early 2019 for employment.

Real Manufacturing Output and Employment, January 2017 to End of 2019

Not all the gloom is due to Trump, of course. The president of the United States, even if he is the paragon of knowledge and wisdom, is, thank God, not all-powerful. But economists and businessmen widely agree that (a big) part of the gloom is related to his trade wars.

A recent econometric study by two Federal Reserve Board economists, Aaron Flaaen and Justin Pierce, confirms that the White House’s trade war has hurt manufacturing employment; see “Disentangling the Effects of the 2018-2019 Tariffs on a Globally Connected U.S. Manufacturing Sector” (December 23, 2019). My chart above sets the context of Flaaen and Pierce’s inquiry. (Their own data only go up to August 2019, while my chart includes more datapoints, which do not change the trends.)

The chart shows that real manufacturing output (red line) started dropping at the end of 2018 while manufacturing employment (blue line) started plateauing, or at least crawling, in early 2019. This marked a break from an upward trend in the two variables. The employment level in manufacturing reached a summit in 1979 (its proportion in total employment has been decreasing since the 1950s) but, in December 2018, it had been recovering from the Great Recession for 10 years. The break at the end of 2018 is especially interesting since it corresponds to the first wave of tariffs on Chinese imports.

One question asked by Flaaen and Pierce is, to which extent has the stagnation in manufacturing employment been caused by Trump’s trade war and tariffs? Such tariffs on manufactured products can have three effects: they can (1) increase employment in the protected manufacturing industries because of import substitution; (2) decrease manufacturing employment because of the higher prices that manufacturing companies themselves have to pay for their tariffed inputs—such as steel, aluminum, lightning equipment, electronic components, etc.—thus becoming less competitive on world markets; and (3) decrease manufacturing employment because manufacturing exports are hit by foreign retaliatory tariffs. The net change in manufacturing employment depends on the relative strength of these three effects. (Of course, more employment in manufacturing would have meant less employment elsewhere, but this not the issue here.)

Flaaen and Pierce built an econometric model to measure the relative impact of the three effects from the 2018 waves of tariffs. Their resulting estimates are that the positive employment effect of protection (effect #1) is more than compensated by either the negative effect of increased input prices in manufacturing (effect #2) or the negative effect of foreign retaliation (effect #3). “For manufacturing employment,” they conclude, “a small boost from the import protection effect of tariffs is more than offset by larger drags from the effects of rising input costs and retaliatory tariffs.” This implies that manufacturing employment would have continued to increase (or increased more) without the tariffs.

Somewhat surprisingly, the two economists do not detect significant effects of tariffs on manufacturing output. Reasons may include that the analysis does not factor in the 2019 tariffs nor the business uncertainty generated by the trade war. Moreover, over such a short period of analysis, only short-term effects are visible.

Yet, the consequences of Trump’s industrial policy appear dismal thus far, which is not surprising as Colbertism and industrial policies typically fail.

The bonus of this post is the observation that, despite the White House’s protectionist policy, and despite the dearth of serious economic analysis coming from that shop, there are still economists working for the federal government who produce useful economic studies that contradict the government’s own intuitions and pronouncements. This is not because the President is very scientifically minded and tolerant of opposing viewpoints, but because the Fed is independent and pursues its own research with a plethora of economists. As Montesquieu argued (The Spirit of Laws, 1748),

Constant experience shews us that every man invested with power is apt to abuse it, and to carry his authority as far as it will go. … To prevent this abuse, it is necessary, from the very nature of things, power should be a check to power.

I cannot resist quoting the original French version of the second sentence above, beautiful and luminous in its concision (and note that Montesquieu wrote “the arrangement of things,” not “the very nature of things”–and that there should be a “that” before “power”):

Pour qu’on ne puisse abuser du pouvoir, il faut que, par la disposition des choses, le pouvoir arrête le pouvoir.

READER COMMENTS

Jon Murphy

Jan 12 2020 at 8:27pm

Add on to this that the US, despite being a “large country,” isn’t even getting a boost in welfare and this trade war looks even worse.

Jon Murphy

Jan 12 2020 at 8:28pm

Oops, I meant to link to this summary and update of the paper I linked to above. Both show the same thing, but this link has more updated information.

Pierre Lemieux

Jan 12 2020 at 8:44pm

Thanks for these useful addenda, Jon. If I find the time, I’ll write on the recent Amiti et al. paper.

However, I am wary of speaking of “welfare” (as opposed to income of even consumer surplus), which we cannot measure. Nobody can, although economists seem to be the only ones to know why.

Jon Murphy

Jan 13 2020 at 9:37am

Yeah, I hear you. I’m always skeptical of any welfare economics analysis (despite the fact it’s largely what I do). The method used in these papers seems conceptually straightforward as they are measuring passthrough of tariffs and they find that the tariffs are being born pretty much entirely by US consumers. I’ve not dug deep into the econometrics, but it seems solid enough.

Warren Platts

Jan 16 2020 at 5:50pm

We probably shouldn’t be jumping to a bunch of general conclusions regarding tariffs at this stage of the game. There are a lot of moving parts. Regarding Amiti’s “econometrics”, they are not without problems. Their main claim–that American consumers pretty much paid for 100% of Trump’s tariffs–comes from their tariff-price regression estimate of ln(p) = -0.003 in their Column (1), Table 1, that is supposed to mean that a 1% increase in the tariff rate will cause a price reduction of 0.003%–virtually nothing.

That price elasticity estimate of zero is not statistically significant (i.e., the p-value is greater than 0.10). Moreover, the two columns in Table 1 they consider to be the most reliable, combining low p-values with large sample sizes, are Column (3) (ln(m), the elasticity of quantity of imports supplied), and Column (5) (ln(pXm), the elasticity of the value (price times quantity) of tariffed imports).

Since ln(x) + ln(y) = ln(xy), then ln(x) = ln(xy) – ln(y). Thus we can back calculate an estimate for the price elasticity based on the two reliable columns: ln(p) = ln(pXm) – ln(m). In this case, we get -6.466 – -6.026 = 6.026 – 6.466 = -0.440, implying that a 1% increase in tariff causes a 0.44% decrease in the price the exporter gets. This is actually more in line with historical, empirical estimates going back to the 1950’s for U.S. imports.

As for welfare, I agree it is problematic to quantify the welfare of a family whose laid-off breadwinner who drinks himself to death because he can’t stomach emptying bed pans for a living. However, in the context of these sorts of tariff models, “net welfare” is precisely defined as the terms-of-trade (TOT) gain (the amount of tariff revenue paid by foreign exporters in the form of squeezed margins) minus the home country’s deadweight loss (DWL).

Amiti provided an estimate of the deadweight loss $6.9 billion, against tariff revenues of $12.3 billion. However, they were assuming full passthrough of the tariff to U.S. consumers. Since there is no TOT gain, the net welfare loss = the DWL of $6.9 billion.

But if we go with the back-calculated price elasticity of -0.44, then we get a TOT gain of 44% X $12.3 billion = $5.4 billion–free tax money paid by foreigners. Moreover, the DWL must also be reduced. Since the DWL is the area of a triangle where the height represents the tariff proportion paid by home consumers (56% in this case) then the DWL = 56% X $6.9 billion = $3.9 billion. Thus we obtain a modest net welfare gain of $1.5 billion ($5.4 billion – $3.9 billion).

It is not my claim here that Amiti et al. did an incorrect analysis and that there really were net welfare gains. My point is merely that these numbers are sketchy. Note that the R-squared estimates for their Table 1 columns were on the order of 0.1, indicating that ~10% of the observed variation in their data is explained by tariff increases.

As for U.S. exports it is the same story (Table 3): Amiti finds about zero price reductions for U.S. exporters, but if you do a similar back-calculation–column (3) – column (5)–you obtain the same tariff-price elasticity of -0.44. Moreover, you gotta wonder if they did their weighting correctly given the stylized fact in the MSM narrative that China’s 25% tariff on U.S. soybeans caused a 20% reduction in soybean prices–implying that U.S. farmers ate 100% of the cost of the Chinese tariff ($100 – 20% = $80; $80 * 1.25 = $100)–and that soybeans are about the biggest export to China.

As for Amiti et al.’s latest paper, again, the results are puzzling. They find that steel import prices declined, as predicted by “large country” considerations, but also that prices increase more than the tariffs, apparently implying a tariff-price elasticity > 1, that is not predicted by any standard tariff model. If we accept those results at face value, I guess if foreign supply curves sloped downwards (as might be expected if major economies of scale were realized) you might get that effect: an increase in price caused by the tariff causes a reduction in quantity demanded that in turn causes the suppliers’ price to rise that in turn further reduces the quantity demanded that in turn causes a further price rise until an equilibrium is finally reached where the price increase is well above the tariff rate.

Or could it be that unscrupulous, adverse-selecting suppliers are using Trump’s tariffs as an excuse to price-gouge gullible consumers?

Dismayed Customer: “When I researched this washing machine a few months ago, it was $300 cheaper!”

Shrugging Salesman: “Don’t blame me! Blame Trump’s tariffs!”

Dismayed Customer: Remind yourself to vote for Biden…

nobody.really

Jan 14 2020 at 3:12pm

Thanks for this post. I figured the trade war was bad economics, but it’s nice to have some numbers to back that up.

That said, there may be more economic merit in Colbertism than you acknowledge.

Pierre Lemieux

Jan 15 2020 at 4:57pm

OK, nobody.really, you’ve persuaded me about Colbertism. I am all in favor. And thanks for the video (which I recommend to all our readers).

Comments are closed.