David Henderson directed me to a new paper by Greg Mankiw, which discusses principles of economics textbooks. Having taught for many years using Mankiw’s principles text, and then more recently writing my own (with Steve Rubb), I was naturally interested in taking a look.

While there is lots of good stuff, my favorite part discusses why the classical long run model should be taught before the short run (Keynesian) model. It’s too long to quote in full, but here are some highlights:

First, notwithstanding Keynes’s famous quip about asymptotic mortality, long-run issues are extraordinarily important for human welfare. Consider: In 1900, Japan had less than half the income per person of Argentina. Now Japan has more than twice the income of Argentina. . . . Second, classical macroeconomics is more closely linked to the lessons of microeconomics. After students have learned about how the forces of supply and demand govern market economies, they are ready to apply these tools to the questions of macroeconomics. . . . Third, the theory of short-run fluctuations is more easily understood after a solid grounding in the economy’s long-run equilibrium. According to standard theories, the business cycle represents a transitory deviation of the economy from its trend growth path. . . . Fourth, short-run fluctuations are more complex than long-run growth. This follows simply from the classical dichotomy—the theoretical tenet that nominal variables (such as the money supply and the price level) do not influence real variables (such as real GDP and unemployment). . . . Fifth, the macroeconomic theory of the short run is more open to debate than the macroeconomic theory of the long run. Although I believe that the traditional model of aggregate supply and aggregate demand remains the best framework for understanding the business cycle, not all economists concur.

I really like that summary.

I just finished writing a long paper on currency manipulation, although I assume I’ll have to spend time revising it after comments. My next two projects are papers on “never reason from a price change” (NRFPC) and NeoFisherism vs. New Keynesianism. Because I first need to find someone good at mathematical econ to help me with the second paper, my next project is NRFPC.

Previously I’ve argued that the Great Recession was caused by two types of reasoning from a price change. One is the Phillips Curve, which sees high inflation (as in mid-2008) as a signal of economic overheating. The second mistake was assuming that sharply falling interest rates (as in 2007-08) represent an easing of monetary policy.

At first glance these seem like very different mistakes. But in each case the right approach was to look at NGDP. And when you start to think about it, it becomes apparent that the economics profession missed a golden opportunity when they decided that NGDP would not become the central organizing principle in the education of our macro students. Regardless of the question, the answer is often “NGDP”. Just think about the following:

1. If we had taught the Phillips Curve model with NGDP growth (or more precisely the level relative to trend) rather than inflation, the model would have done far better after 1970.

2. If we had used expected NGDP growth as a measure of the stance of monetary policy, then lots of the confusion would have been removed. Why were rates so high in 1980? High interest rates suggested tight money. Rapid NGDP growth suggested easy money.

3. NGDP growth provides a near perfect way of talking about financial crises, which are generally correlated strongly with NGDP growth, but not as strongly with inflation. And that can be explained by the fact that financial contracts are not indexed to either inflation or RGDP. Or they can be explained by the fact that nominal income is the resource available to repay nominal debt.

4. NGDP growth is a good way to think about labor market instability, given that wage contracts are generally in nominal terms. Students can understand the musical chairs model. Try explaining to students that low inflation hurts workers. And we would have gotten far better results talking about nominal wages deflated by NGDP rather than deflated by the price level.

5. Lender/borrower redistribution can be more easily explained with the idea that unexpected NGDP growth favors borrowers and an unexpected decline in NGDP favors lenders.

6. The Fisher effect could have been taught with expected NGDP growth rather than expected inflation, as faster RGDP growth also tends to boost nominal interest rates.

7. The aggregate demand curve could have simply been set equal to a given level of NGDP (i.e. a hyperbola, or unit elastic). This makes it super easy to explain its downward slope. Instead our textbooks (including mine) have three explanations, which not one student in a thousand will understand.

8. The classical dichotomy is super easy to explain with NGDP. Nominal (monetary) factors determine NGDP, and real factors determine the P&Y split in NGDP growth.

NGDP is the proper way of thinking about the stance of monetary policy. It’s the right way to think about aggregate demand. It’s the right way to think about nominal shocks. It’s the right way to think about the welfare cost of inflation. It’s the right target of monetary policy. It’s the right way to think about recessions. It’s the right way to think about financial crises. It’s the right way to think about the Phillips Curve.

Instead, we use a hodgepodge of different variables (interest rates, inflation, aggregate demand, real GDP, unemployment, etc.) most of which are not even the right variable for the thing we are trying to explain. Normally you add complexity to make things more accurate. We’ve added complexity and ended up making the model far less accurate. That’s just appalling!

Macro should be the study of two things:

1. The causes and consequences of long run economic growth, and its components like saving and investment.

2. The causes and consequences of shocks to NGDP.

Plus a bit of international macro.

PS. Pat Horan and I have a new piece on MMT.

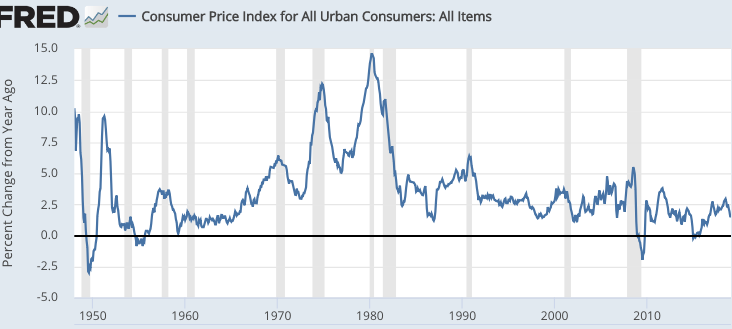

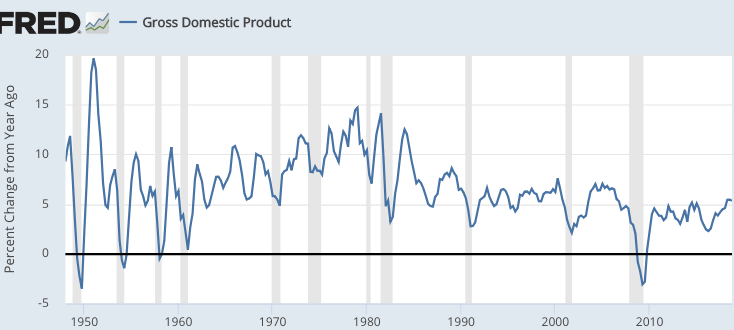

PPS. Which correlates better with the business cycle?

READER COMMENTS

Benjamin Cole

Mar 12 2019 at 8:39pm

I agree with everything in this post and yet and yet.

If you had placed 100 million Japanese into Argentina in 1900, what would you find in Argentina today? Is the success of Israel really explained by some sort of long-term macro economic models?

Also, Larry Summers March 7 paper for Brookings says that without large government deficits in the developed world, interest-rates today would be deeply negative. He even posits there is a tendency toward secular stagnation which must be offset by government action, presumably deficits. How long is the long run, but Summers is talking about decades and not quipping. Summers all but dismisses monetary policy as a stimulus, but I assume he believes monetary policy can still act as a noose.

Dani Rodrik’s views on how economies really develop are worth pondering as well.

I wonder if classic macro economics has become obsolete, or at least deficient enough to become misleading when taught as a standalone topic.

John Hall

Mar 13 2019 at 12:59pm

Interesting post. You might find the following interesting as well.

I fit an ECM model to quarterly NGDP, employment, labor force, hourly earnings, and weekly earnings. I also included population growth as a deterministic factor as well as the SPF NGDP growth expectations 1 year ahead, lagged one quarter (to account for timing of when that survey takes place). Anyway, I got the residuals and performed a PCA on the covariance matrix. I found that a factor that is highly correlated with NGDP explains about 67% of the variance. During recent periods of rising unemployment, this factor seems to be the big driver.

The general idea was that other variables like real GDP and inflation could be regressed on these variables contemporaneously. Something like the unemployment rate can be calculated from the model using employment and the labor force. This means that a relationship like the Philips curve will only show up indirectly. But it’s still there. Shocks to the 1st principal component has an inverse relationship on NGDP and unemployment.

Philo

Mar 15 2019 at 10:57am

You say that “faster RGDP growth also tends to boost nominal interest rates,” but I wonder about the causation. Maybe you should have said that *the factors that cause* faster RGDP growth also tend to boost nominal interest rates.

Comments are closed.