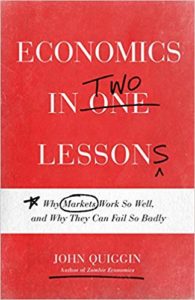

Does Economics Need More than One Lesson?

By Michael D. Thomas

Quiggin rewrites Hazlitt’s book from his own perspective. Like the original, Quiggin’s book is part polemic, part business book, and part armchair speculation. This last component feels much like Steven Landsburg’s The Armchair Economist, and at times drifts into sections that sound like Robert Heilbroner’s The Worldly Philosophers. These features make it a fun book to read, and its prose is good. The book presents a bit of a conundrum though. While the book aims at a lay audience, at times its scholarship seems to move past casual descriptions of economics to assert final authority on particular academic debates. In these cases, Quiggin is sufficiently heterodox to make assertions that must be backed up by his own research. For example, his 2000 book (with John Chambers),3 is cited as a rejection of the concept of moral hazard as a distinct type of asymmetric information (page 227 and 236). A casual reader might expect that Quiggin’s own unorthodox approach to economics would make him sympathetic with what he sees as Hazlitt’s attack on the orthodoxy of Keynesian economics. If that is the case, however, that aim was lost on this particular reader. By the end, Quiggin succeeds in adding a leftist perspective for neophyte economists on the conversation started by Frederic Bastiat and joined by Hazlitt in 1946.

The book is divided into two sections. The first part establishes some common ground with Hazlitt’s work. Given that the book is pitched as a corrective to Hazlitt, developing Hazlitt’s core contribution is an important part of the rhetorical approach. Quiggin agrees with Hazlitt that opportunity costs are a defining point of economics. The second part of the book structures a response to situations where people get those opportunity costs wrong: when economies are not at full employment, have systematic market failures, or when agents are imperfectly rational. An additional gripe that Quiggin adds under lesson two, part II is a normative defense of positive rights based on both his political leanings and a principle that he attributes, with explicit irony, to Friedrich Wieser. This use of Wieser highlights a supposed inconsistency in the thought of early Austrian economists (page 27).

Wieser’s distinction is about the diminishing marginal utility of a dollar. A decreasing marginal utility would give rhetorical force to the idea of redistribution as an efficiency improving move. “One Lesson Economists” are cast as uniquely unwilling to see this truth and as hiding at various times behind denials of this truth. Quiggin is willing to label these economists as polemic or ideological but seems comfortable using polemics himself to his own advantage. In a footnote on page 2, Quiggin lets us know that his use of “One Lesson Economists” is meant to be pejorative similar to the use of the terms “Chicago School Economics”, “Neoliberalism”, “Thatcherism”, “Washington Consensus”, and his own term in a prior book, “Market Liberalism”. This makes for a big tent. He introduces another term that he applies frequently throughout the book, “Propertarian” that he takes from Ursula LeGuin’s science fiction novel, The Dispossessed. This term bolsters his own reading of right-wing economics as based on egoist conceptions of rationality which have largely been undermined by empirical economics (see Quiggin 1987). The implication of this term is that anyone in this group that calls themselves libertarian is doing so with the knowledge that property rather than liberty is their principle. To underscore this claim, Quiggin points out that Friedrich Hayek and Ludwig von Mises were “working for murderous regimes” citing a relationship between Hayek and Augusto Pinochet of Chile as well as flagging that Vilfredo Pareto was rewarded with a ‘royal’ nomination by Benito Mussolini (page 147). The implication is that right wing economists are sometimes explicitly fascists. These observations are clearly meant to discredit the ideas without engaging the substance.

By casting Ludwig Mises and F. A. Hayek on the wrong side of this normative position, he also implicates a whole range of economists influenced by these thinkers and gives them the label “One Lesson Economists.” Lionel Robbins is included in this list as is Hazlitt. At times Milton Friedman is on the wrong side of this normative position, and a blanket dismissal all of Real Business Cycle Theory is impugned with this same label (page 302). Ronald Coase’s 1962 article, “The Problem of Social Costs,” is also dismissed because he “did not analyze [property rights] very satisfactorily but observed that unspecified ‘transactions costs’ might prevent the parties from reaching an agreement” (page 199), however, Coase’s 1937 article, “The Nature of the Firm,” is treated with authority (page 325).

The Paul Samuelson quotation used for the introduction to the book gives the basic exercise Quiggin undertakes. The quotation reads: “Moral: To understand economics you need to know not only fundamentals but also its nuances. Darwin is in the nuances. When someone preaches ‘Economics in One Lesson,’ I advise: Go back for the second lesson.” (emphasis added). This quotation also appears on page 149, and both mentions of Samuelson in the book are in reference to this point. Quiggin offers his second lesson, introducing externalities, but rather than treating the concept like a great debate, known as the Public Interest Theory of Public Finance, the lesson is offered as much more conclusive than is the scholarly literature in economics. It is confusing to this reader that Quiggin omits perhaps the strongest defense Hazlitt has to his criticism. In chapter IV of Hazlitt’s original book in particular, Hazlitt clarifies that the central fallacy of opportunity costs is to apply the concept too narrowly, either by over emphasizing the benefit to one group or focusing on the short run or long run only. Not only would the inclusion of this nuance somewhat redeem Hazlitt from a charge of overly simplistic thinking, but it would also be a great place to mention the more scholarly arguments that have been made by Hazlitt’s close acquaintances.

It is important to note that Quiggin’s argument removes any tension in current economic thinking by offering a litany of dismissals of people who disagree with his normative position. William Easterly is grouped among those economists that are heretical (pages 93-96). That dismissal comes immediately after Quiggin introduces the first element of his institutional critique that he returns to in chapter 11. In neither place does he mention Nobel laureate Douglass North, and in a passing reference to Elinor Ostrom he falsely claims that she refuted the role of property rights in institutional economics (page 105). The Chicago School’s noteworthy collection of Nobel recipients and all of Public Choice theory is dismissed with an opportunistic reference to a YouTube video by Philip Mirowski suggesting a right-wing bias in the founding of the Nobel Prize in economics. These omissions and errors have the cumulative effect of isolating Quiggin from the strongest arguments that would preserve necessary complexity in his analysis. Quiggin’s scholarship suffers as a result of these omissions, but his polemic is energized.

While there are plenty of frustrating rhetorical moves in the book, there are also redeeming features. Chapter 8 introduces a very interesting description of economists’ writing on the business cycle, explaining the importance of John Maynard Keynes. Quiggin’s position is that an economy is very unlikely to be at full employment because of the complexity of aggregate economic activity. In this case, “one lesson economics” is far less applicable any time the macroeconomy is off of its long-term average growth path. This description of macroeconomic equilibrium has the benefit for Quiggin’s theory of both placing Keynes at the center of macroeconomics and Arthur Pigou at the center of microeconomics. Both of these theories are thought of as externalities, or second lesson economics, and this is really clear in the section “8.6. The Macro Foundations of Micro” (p. 165). Such a move ignores the essential non-equilibrium nature of Austrian economics which nowhere assumes full employment.4 Quiggin asserts that “involuntary unemployment” is proof that “one lesson” micro assumptions are flawed (page 166).

Other welcome contributions include a rather full-throated defense of the least-well-off that places their own agency at the center of the argument (page 92). This is an important defense of markets, and a point of common ground between Quiggin and Hazlitt. Quiggin’s critique of monopoly power is that it impedes the functioning of the economy, which is a point well taken. His specific call for reform of intellectual property and corporate bankruptcy laws is welcome (page 240). Both of these are well articulated reasons why a concerned citizen should be interested in supporting reform of property rights. As Quiggin expands his defense of these insights, however, he shows that his normative position is driving his thinking. In a well-articulated history of unions (pages 242-249) Quiggin does little more than suggest that union membership is falling, implying but not offering a concrete justification for the claim that a return to union power would improve conditions for workers. This invokes sympathy for workers, but little else. Despite the lack of substantive argument, Quiggin makes increased union power a central part of his correctives for current policy (page 285). The owners of capital do not come off well in this book’s polemic. In a discussion of financial markets Quiggin states, “… high incomes derived from financial markets do not reflect an economic contribution” (page 277). This observation does not offer much subtlety, and it is stated with the authority of an empirical observation. The observation follows a discussion of the Laffer curve, which dismisses the “incentive effect” for high income earners to work more as a result of lower tax rates (page 276) and only sees reduced revenue from “tax avoidance” as a corruption in an improperly governed global financial market (page 284). The idea that growth rates and redistribution are inversely related is dismissed without examination by impugning the character of high-income earners as ego-driven parasites.

I certainly take Quiggin’s point about the limits of Hazlitt’s original work. At times, it seems as though Quiggin is responding to a broader set of Hazlitt’s writing. Keynes, for example, plays a much bigger role in Quiggin than he did in Economics in One Lesson. There, Hazlitt specifically mentions Keynesian policy in the introduction in order to state that he will not address it explicitly in the book. To be fair to Hazlitt’s original, its task was much more circumspect than is Quiggin’s project. Hazlitt did take on Keynes inspired economics later in his 1959 The Failure of the ‘New Economics’. This later book was a detailed response to Keynes, which went beyond the popular writing of Economics in One Lesson, and was a more abstract intramural debate between economists. More influential for the way that economics is practiced were the ideas of John Hicks and Alvin Hansen as well as Nobel Laureate Paul Samuelson’s principles of economics textbook. At this level of abstraction and complexity relatively few readers will wade into the weeds. Hazlitt’s continued popularity is for his more approachable contribution, which is an excellent motivation for Quiggin’s rebuttal. Quiggin’s book serves more readily as an alternative popular piece. It positions itself as a book for the more advanced layperson reading about economics, which is a difficult niche to fill. The book is too advanced for a casual read, but not sophisticated enough to be scholarly (which is a shocking assertion given that this is Princeton University Press). I worry that Quiggin’s rhetorical strategy follows the same flawed thinking of cable news networks. By expanding the content available for laypersons without demanding greater levels of sophistication, the general debate is full of gadflies whose critiques know no correction for their many obvious errors.

I would have loved to see, in this book, what economists call behavioral symmetry. By holding human nature constant between the marketplace and government, a better picture of the limits of government could be presented. “[G]overnment failure” makes it into a footnote on p. 184, but it is not clear that Quiggin fully appreciates that government failure arises from the same kind of limitations in government that he critiques in markets. Without clearly asserting why he thinks behavior is superior in government, he simply abstracts from reality. Quiggen’s 1987 dismissal of public choice theory5 is into this thinking. By pointing to market failures that result from lack of full employment, externalities, and failed rationality, Quiggin is opening the door for expanding the scale and scope of government. This requires some more explicit opportunity cost thinking, which was the main point of Hazlitt’s original text. Behavioral economists are already drawing on various laboratory experiments to suggest systematic failures of rationality. These theories require various forms of intervention ranging from nudges, like altering choice architecture, to taxation; and in some cases prohibition of choices. There is no evidence in the book that Quiggin, who is so quick to point to the diminishing return to financial market arbitrage, recognizes any limits to or systematic problems with government growth in scale and scope.

These arguments about the limits of government are the vital ones to have and are also clearly important enough for readers of polemic, business books, and armchair speculation to really sink their teeth into. To address the level of complexity required for these important issues we need books that are less normative and more helpful in communicating the complexity of the scholarly literature for people who don’t have a scholarly background in these particular areas.

If Hazlitt’s book failed because it was too polemical, Quiggin’s response in this book serves to take a relatively more sophisticated audience down an even more polemical path. He asserts his own normative positions and pejorative descriptions of others’ as mere alternatives to Hazlitt and does not succeed in offering a corrective that is more intellectually generous. Where Quiggin backs up his assertions, he is unorthodox. Where he is in the mainstream, he generally fails to build bridges of common ground with thinkers he attacks elsewhere. The footnotes and end of chapter notes could have been wonderful places to point readers to further depth on the live debates in economics. The book is overly resolved on issues that need careful articulation. If Hazlitt’s book gave the impression that articulating opportunity costs was simple, then Quiggin has imitated this failure to a fault.

Footnotes

[1] Henry Hazlitt, Economics in One Lesson: The Shortest and Surest Way to Understand Basic Economics. Currency, 2010.

[2] John Quiggin. Economics in Two Lessons: Why Markets Work So Well, and Why They Can Fail So Badly. Princeton University Press, 2019.

[3] Robert G. Chambers and John Quiggin, Uncertainty, Production, Choice, and Agency: The State-Contingent Approach. Cambridge University Press, 2000.

[4] Peter Boettke, W. Zachary Caceres, and Adam Martin, “Error is Obvious, Coordination is the Puzzle,” Hayek and Behavioral Economics, Palgrave Macmillan, 2013.

[5] John Quiggin, “Egoistic Rationality and Public Choice: A Critical Review of Theory and Evidence,” Economic Record, 1987.