The title of this post lists three macro models that I believe are wrong. But they are not all wrong in the same way.

I’m not even sure I understand MMT, as when I try to engage with proponents of that theory they keep telling me that I’ve got it wrong. I say, “So you’re saying A, and here’s why that’s wrong.” They respond, “No, we aren’t saying A, we are saying B.” I respond, so you are saying B, here’s why that’s wrong.” And they respond, “No, we are not saying B, we are saying C.” Then I explain why C is wrong. It never ends.

Perhaps it’s just me. But here’s the problem for the MMTers. Paul Krugman is sympathetic to many of their policy preferences. He’s also “on the left”. He likes some politicians who like MMT. But he has exactly the same reaction to the model as I do:

Now, arguing with the MMTers generally feels like playing Calvinball, with the rules constantly changing: every time you think you’ve pinned them down on some proposition, they insist that you haven’t grasped their meaning.

I don’t expect everyone to be able to explain their models in a way that a slow mind like me can understand. But they should be able to explain it to one of the half dozen most brilliant economists in the world.

It seems to me that the problem with macro is that the underlying problems are so complex that there are a wide variety of ways to address these problems. For instance, just in the field of money you have the interest rate approach, the quantity of money approach, and the price of money approach. Within each of those you have varying assumptions about price stickiness, Say’s Law, crowding out, rational expectations, Ricardian equivalence, market efficiency, and a host of other issues. The possible approaches quickly multiply, each developing different frameworks and even different languages. C + I + G = PY. MV = PY. IS/LM. AS/AD. Etc., etc. You end up with a sort of Tower of Babel.

To me, MMT seems like a more extreme version of Keynesianism, having all of its flaws and none of its virtues. In contrast, NeoFisherism takes one of the flaws in Keynesianism, reasoning from a price change by assuming that lower interest rates are expansionary, and inverts it into the opposite error of assuming that lower interest rates are contractionary. Here’s Krugman:

Figure 1 illustrates my point. Suppose that the Fed or its equivalent in another country can set interest rates, and that a lower interest rate leads, other things equal, to higher aggregate demand. Then at any given point in time there is a downward-sloping relationship between the interest rate and GDP, as shown by the lines IS1, IS2, IS3.

Other things equal? Hold on there! Just how does the Fed achieve lower interest rates while holding “other things equal”? I claim that there are two ways for the Fed to drive rates lower, with an easy money policy or with a tight money policy. Neither involves holding other things equal. This post shows what each of those policy options might look like.

Now obviously Krugman meant “lower rates created by an easier money policy.” He’s a Keynesian. But then instead of simply saying lower rates, he might have said “Lower rates resulting from the liquidity effect from an increase in the monetary base.” In that case, it’s the bigger base that’s actually having the expansionary effect. Lower rates slightly reduce velocity, and make the expansionary effect smaller than otherwise.

Or he could have said “Lower rates produced by a policy that reduced the demand for base money, such as lower reserve requirements or lower interest on reserves”. That would work too.

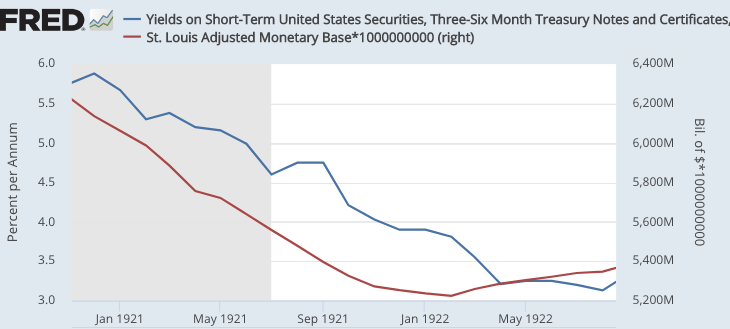

If he doesn’t specify, how do we know that he doesn’t mean, “Lower rates via a Japanese style monetary policy that produces the slowest NGDP growth (over 25 years) in modern history.”? Or lower rates via the methods used by the Fed in 1921, when they contracted the monetary base so sharply that we had double-digit deflation.

The Keynesian model is more prestigious than the NeoFisherian model, but it’s not any better. Indeed during 2008-15, the NeoFisherian model was giving better advice as to whether monetary policy was too tight or not, even as the Keynesian model did a better job of explaining real time market reactions to unexpected changes in the Fed’s target interest rate.

Of course the market monetarist model can explain both, which is why it’s the best.

READER COMMENTS

Benjamin Cole

Feb 26 2019 at 7:51pm

I agree with this post. I think.

Still, in the modern economy, what is debt but a blip on a computer chip?

It is a claim on future production, held in abeyance.

A national government can borrow digitized money and spend it to charge up present output. Or a government could simply digitize money and spend it to charge up output.

Why should a government incur debt if it has a better option?

When a government digitizes (prints) money, should that be more inflationary than when commercial banks digitize money ( the endogenous creation of money)?

The MMT crowd may be onto something, but they need a lot of refinement. They probably think the same thing about me, but in spades.

Brian Donohue

Feb 27 2019 at 10:15am

Good post.

Is there any benefit to replacing talk about interest rates with talk about “real interest rates”. Real interest rates were very high in the 1920s.

Perhaps there is too much noise in TIPS yields (you’ve mentioned oil prices and the market is probably a lot less liquid) for them to provide a reliable signal. I don’t know.

Assuming CPI does more or less track purchasing power, TIPS are a revolutionarily honest way for governments to borrow money, protecting investors against the chief risk associated with such lending.

As such, the TIPS curve should exhibit greater stability than the Treasury curve. Higher TIPS yields are a sign of market bullishness and/or Fed restraint. Like the Treasury curve, TIPS can take on a variety of shapes with “normal” being modestly upward-sloping, and changes in the shape reflect changes in real time preference. Isn’t this the curve that is trying to track the unknown Wicksellian interest rate?

Michael Sandifer

Feb 27 2019 at 10:47am

Scott,

I personally have much more sympathy for the Keynesian perspective, especially New Keynesianism. While I think it’s ultimately wrong, I don’t think it’s unreasonable to think the ZLB is a real problem, beyond just a bad monetary policy regime.

That is, while I personally favor the Market Monetarist perspective, I don’t think the empirical case for the framework is close to settled. When we see large monetary base expansions with only slight pickups in NGDP growth, we appeal to hidden variables like money demand to explain why the “concrete steppes” shouldn’t distract us. We explain that the monetary policy regime is bad, with empirical some merit, in my view.

But, while it would be easy to imagine an occasional excused ZLB problem here or there, the sheer number of countries that have struggled with this should give us pause and not allow us to be too proud.

Yes, the US escaped the ZLB and I think QE worked to a limited degree. But, New Keynesian theory also allows this to be true, does it not? Also, I’m not sure the Market Monetarist perspective is empirically more sound than Jason Smith’s IT approach to economics, which models macro very differently, and not without empirical success.

There is too little data and too little solid modeling to cling to any model with what I would begin to call certainty. The Market Monetarist model fits my intuition best, but perhaps that’s primarily due to my bias.

Scott Sumner

Feb 27 2019 at 1:11pm

Brian, you asked:

“Is there any benefit to replacing talk about interest rates with talk about “real interest rates”.”

A bit, but not much.

Michael Pettengill

Mar 5 2019 at 1:26pm

The past decade has produced drastically lower velocity.

A simplistic explanation or model for velocity is the rate money is paid to workers.

Since circa 1980, paying money to workers is no longer of importance to economists, its approaching evil. As in, paying workers costs too much, and high costs kill jobs.

I have concluded modern “capitalism” requires the repeal of the 13th amendment to make job creation economically feasible, ie, have low costs. Once white people become property owned by non-white people, we will see Keynes theory and policy regain popularity. Keynes argued for paying both men and women of all ages to labor to build capital assets until assets cost less than the labor costs, and are thus no longer scarce.

And money is merely a proxy for labor performed in the past or to be done in the future. Venezuela has demonstrated the folly of all versions of monetary theory in regard to creating jobs, increasing production, or “wealth”. In Venezuela, an egg creates massive wealth in 24 hours, with 25-100% capital gains in response too the vast money printing presses. Printing money results in no increase in workers tending and feeding egg layers.

Lorenzo from Oz

Mar 7 2019 at 7:34am

Cameron Harwick has a post which seems to make sense of MMT (not to be confused with agreeing with it).

https://cameronharwick.com/blog/whats-radical-about-mmt/

Comments are closed.