The Economist has an interesting article discussing central bank independence:

Mr Trump has already appointed a majority of the sitting governors of the Federal Reserve Board. Had he kept his mouth shut but appointed more doveish types, he might have achieved the same end without the outcry.

That sounds reasonable at first glance, but there are some tricky issues here that need to be disentangled. First of all, what is “the same end” that President Trump achieved? Conventional wisdom says that he failed to get Jerome Powell to adopt a low interest rate policy. Yet the article refers to a dovish policy, which might or might not be the same thing.

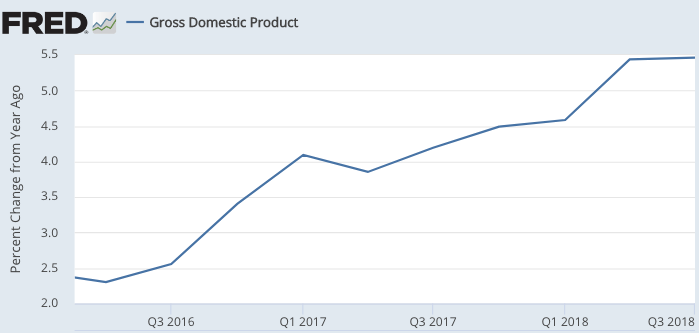

Also note that while Trump replaced Janet Yellen with a slightly more hawkish person, Fed policy has actually become more dovish under Powell’s leadership, as NGDP growth has accelerated sharply since 2016. (Inflation has increased more modestly.) Recall that Ben Bernanke suggested that interest rates were not the way to judge the stance of monetary policy; rather we should look to NGDP growth and inflation. He’s right.

The ironies keep piling up. Trump says he’s a “low interest rate guy”, and everyone seems to assume that he favors easy money. On any given day those two objectives line up. But over the months and years they move in opposite directions. Easier money leads to faster inflation and NGDP growth, and higher interest rates. So what does Trump “truly favor”? Hard to say. It’s not clear that he’s even thought about this distinction. Indeed even well informed people often gloss over this issue.

And it gets even more complicated when you consider the Fed’s inflation target. What does it mean to talk about hawks and doves in an institution that is committed to a 2% inflation target? Is it likely that a “dove” like Janet Yellen would have pushed inflation up to 3%, or higher? That sort of outcome was plausible when President Nixon was pressuring Arthur Burns back in the early 1970s, but today it seems highly implausible.

Much of the discussion of Fed interest rate policy is misleading. Under a 2% inflation target, any victory for the hawks or doves is fleeting. They can nudge rates higher or lower, but unless they are willing to shift the inflation target down to 1% or up to 3%, any success will be temporary. A rise in rates will slow the economy, forcing a subsequent cut in rates. You see that in the way the yield spread responded to last month’s Fed announcement. Short-term rates rose and longer-term rates fell.

Trump appointed a slightly more hawkish Fed chair, who has delivered a somewhat more dovish policy, which is considered by most pundits to be a somewhat more hawkish policy. In such a confusing world, how likely is it that Trump will get what he really wants? And what does he really want? A slow growing low interest rate economy like Japan, or a higher interest rate faster growing economy like the US? Your guess is as good as mine.

The markets are now scaling back their estimates for future rate increases, due to slower expected NGDP growth. Is that a victory for Trump’s pressure tactics, pushing the Fed toward lower rates? Or a failure–pushing the Fed toward tighter money?

READER COMMENTS

Benjamin Cole

Jan 3 2019 at 7:22pm

Well, yes, but the Fed could treat its 2% inflation target as a target and not a ceiling.

The Reserve Bank of Australia as an inflation band target. But in the decades since Australia has not had a recession, the RBA has endured some periods of 3% and even 4% inflation. Rather than accelerating from the 4% apex, inflation receded back to RBA target zones. Evidently, the RBA did not have to induce a recession to get back to inflation target zones— thus dispelling the myth that higher inflation rates must end in recession or hyperinflation.

To further muck things up, there are highly intelligent macroeconomists who contend that when the Fed lowers interest rates that actually signals lower inflation ahead— see the Fisherians, or is it the neo-Fisherians?

And of course there is the example of Japan where the Bank of Japan has kept interest rates at zero and they have inflation at 1%. They seem stuck there.

So why is the Fed raising interest rates? Because, it is normalization!

Benjamin Cole

Jan 3 2019 at 7:49pm

Add-on: if there are disinflationary biases present in the modern economies, perhaps central banks should shoot for inflation rates a little bit above target rates, and then watch as inflation inevitably slips down into target zone. This seems to be the situation often in Australia, where inflation has been at or below target recently despite exploding house prices.

Presently, house prices in Australia are crashing and may fall as much as 20% to 30%. It was a 25% decline in house prices, and a 40% decline in commercial property values in the US that led to the Great Recession of 2008.

Asset values in Australia may reflect large capital inflows, due to chronic trade deficits. The IMF has posited that such asset values are unsustainable and lead to instability.

Has the RBA been too tight? Or must the RBA constantly validate higher asset prices born of capital inflows?

At least until Hyman Minsky enters the room…

Thaomas

Jan 4 2019 at 7:50am

Maybe the Fed is “less dovish” but it is still “hawkish” until the price level has returned to it’s 2% pa trajectory (or even better NGDP to its 5% pa level). We still have not made up for the period of inflation at less than 2% (or NGDP was less than its 5% pa trajectory) during the recession. “More dovish” in the present circumstances would be about how much above the 2% pa trajectory of the price level (or 5% pa NGDP trajectory) to go before raising ST interest rates/doing QE or whatever tool the Fed chooses to use for monetary stimulus.

Mark Z

Jan 4 2019 at 12:09pm

Could you clarify your last sentence? Why would markets scaling back estimates for futures rate increases push the fed toward tighter money? Also, might a possibility be that markets just expect the Fed to be responsive to changes in NGDP growth now, regardless of what the president wants?

Brian Donohue

Jan 4 2019 at 1:24pm

Too much rearview mirror in your thinking. TIPS spreads tightened 0.20% at long maturities and almost 0.4% at the short-end during 2018, and are now well below the Fed’s supposed 2% target. If you can’t see that monetary conditions tightened in 2018, I don’t know what to say.

Scott Sumner

Jan 4 2019 at 8:11pm

Mark, I meant that Trump’s comments might have pushed the Fed toward tighter money, to avoid looking like they were being pressured. I’m not saying that happened, but it’s possible.

Brian, TIPS spreads are currently being distorted by falling oil prices, although I agree that inflation expectations have recently fallen.

Comments are closed.