Market monetarists favor a policy regime where the instrument setting creates a policy stance that the financial markets believe will achieve the Fed’s policy goal. Thus, if the Fed’s goal is 2% inflation, then the monetary base (or the fed funds target) should be set at a level that the market believes will result in 2% inflation.

Here’s Yahoo.com:

Is the Federal Reserve beholden to short-term volatility in the financial markets?

A handful of Fed-watchers argue that the answer is yes, based on language from the Federal Open Market Committee’s meeting minutes released Wednesday. They point to two words: “premised importantly.”

“Revealingly, participants noted that low borrowing costs and high equity prices were ‘premised importantly’ on expected Fed rate cuts,” Capital Economics’ Michael Pearce wrote on Wednesday. “Translation: The Fed is petrified of upsetting the markets and will therefore continue cutting rates.” (emphasis added)

Here’s the full quote from the July FOMC minutes for context: “Participants observed that current financial conditions appeared to be premised importantly on expectations that the Federal Reserve would ease policy to help offset the drag on economic growth stemming from the weaker global outlook and uncertainties associated with international trade as well as to provide some insurance to address various downside risks.“

Rather than say the Fed is “petrified of upsetting the markets”, it would be more accurate to say the Fed increasingly recognizes that market forecasts are superior to its failed Phillips Curve models. The markets expect sub-2% inflation over the next 5 years, and also predict several more rate cuts.

In other words, the markets are saying that Fed policy is likely to be too tight to hit their inflation target, and also that this excessively tight Fed policy will involve several more rate cuts. In that case, it would be a huge mistake for the Fed to be tighter than the market currently expects. Indeed, the Fed may wish to be even more expansionary than the market expects.

While I wish the Fed was even more beholden to the financial markets, this is clearly a positive step toward a more market monetarist policy regime.

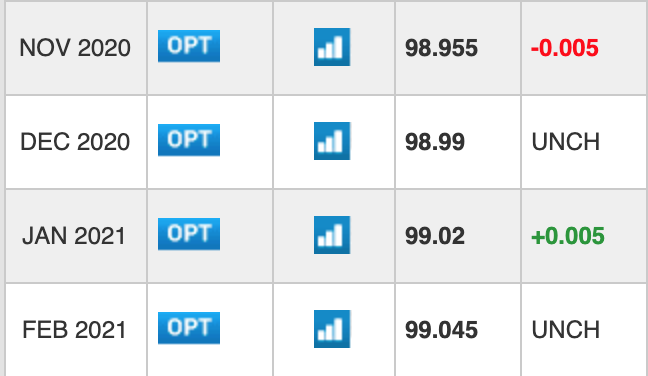

PS. Fed funds futures currently show that investors expect T-bill prices of roughly 99 by the end of 2020. That implies a market consensus that T-bill yields will have fallen to roughly 1% by that date:

READER COMMENTS

Benjamin Cole

Sep 8 2019 at 8:33am

Interesting topic. I think Scott Sumner is right (with the proviso that no one is ever wrong in macroeconomics).

But….

I wonder if “the market” is picking up on signals sent recently by central-banker types, and also major Wall Street players.

Two high BIS officials recently issued speeches and papers that more or less said central banks have done all they can do, “the ball is not in our court” and that fiscal stimulus will be needed.

See, for example, https://www.bis.org/speeches/sp190905a.htm

Then we have BlackRock (world’s largest asset manager), Pimco (world’s largest bond manager) and Ray Dalio (world’s largest hedge manager) all have said that some type of money-financed fiscal programs, or something muddy but similar, will be needed, as monetary policy has tapped out. Wall Street thinks central bankers have tapped out.

Larry Summers is saying we will need fiscal stimulus again, citing WWII, and has revived thinking that the Great Depression would have never ended except for WWII spending.

It could be the BIS, Wall Street thinkers and Summers are wrong, that monetary policy can work, just by going deeper into negative interest rates and bigger on QE.

Whatever the reality on the efficaciousness of monetary policy, Market Monetarists now face a couple of curveballs:

What if “the market” does not believe in conventional (including QE) monetary policy, thanks to misinformation from the people cited above? People believe central bankers are armed with popguns.

What if central bankers believe the BIS, and absolve themselves of responsibilities going forward?

It seems even Market Monetarists may be forced into the MMT camp, or the Keynes crowd, or into the “send in the choppers” group.

If “the market” concludes central bankers are weaklings, or if central bankers say that have done all they can do (“We are weaklings!”)….new policy tools should be considered.

Thaomas

Sep 9 2019 at 6:10am

If markets do not believe that central banks can buy enough stuff to get inflation up to a 2% average, then central banks will just have to buy more stuff to persuade them they are wrong than if markets were less pessimistic.

Whether or not we need more fiscal stimulus depends on the returns on public investments discounted at the borrowing rate. The more stuff central banker have to buy (the lower rates on public sector bonds go) the more “fiscal stimulus” will be income maximizing.

Benjamin Cole

Sep 8 2019 at 8:42am

Add on (sorry):

What do we make out of the sacred canon “central bank independence” if the views of the BIS (see my comment above) are in fact the views of central bankers?

Should we grant independence to a group of monetary policymakers who declare, “The ball is not in our court”?

Thaomas

Sep 9 2019 at 6:14am

Why not. Political authorities just tell them, “Sorry, we hired you to maintain full employment and prices rising a whatever you figure is the optimal rate, so get back to work and quit whining!”

Brian Donohue

Sep 9 2019 at 9:16am

“Indeed, the Fed may wish to be even more expansionary than the market expects.”

May? If the Fed is trying to achieve their stated inflation target, I think you mean MUST.

Scott Sumner

Sep 9 2019 at 9:37am

Ben, Not sure why you keep repeating the same misinformation, when I’ve answered your questions dozens of times. Do you read my replies?

Comments are closed.