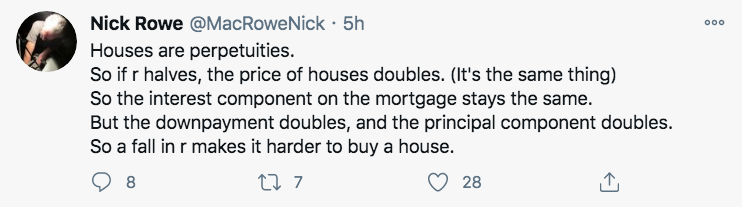

David Beckworth directed me to this Nick Rowe post:

Let’s start with land, and assume we are not living in the Netherlands. The supply of land is fixed and hence the price is 100% demand determined. If consumer preferences do not shift, then the affordability does not change at all. But the concept of “price” is tricky, as it may be a composite variable that involves both the size of a required down payment (a function of the price of land) and the annual cost of a loan to buy land.

Now assume the interest rate falls in half for reasons unrelated to the land industry (to avoid reasoning from a price change.) If the price of land were to double, then land would be less affordable for the reasons suggested by Nick. But if consumer preferences did not change, then this cannot be the equilibrium outcome. Instead, price will rise by less than 100%, and the added negative of higher down payments will exactly offset the added benefit of lower monthly loan payments (due to lower interest rates.) The price of land will rise, but the composite cost of owning land (down payment plus interest) doesn’t change.

Now let’s think about how lower interest rates affect the price of mobile homes. Assume these homes are manufactured in industries where the long run supply curve is perfectly elastic. (That’s actually a reasonable assumption.) In that case, cutting the interest rate in half has no long run effect on mobile home prices. But it reduces the total cost of owning a mobile home and thus demand shifts right, which in the long run means higher quantity sold at the same price per unit.

Now think about “housing” as a house/land hybrid. The land is fixed in supply, and the house can be produced in the long run at constant cost. Now when interest rates fall in half there is some net decline in the total cost of housing (down payment plus interest) and some net rise in house prices and house output. In Texas, the effect of lower interest rates mostly shows up as higher quantity. In California, the main impact of lower rates is to increase house (i.e. mostly land) prices.

PS. This is not an academic exercise. Lower interest rates are the new normal.

PPS. Yes, it matters why rates fall. In this example, assume the fall in rates is caused by some combination of more saving and fewer opportunities for business investment.

READER COMMENTS

Market Fiscalist

Jan 22 2021 at 4:00pm

I’m looking at this from the perspective on the rental values on land v mobile homes and not coming to the same conclusions.

In the long term the risk-adjusted rate of return on both land and mobile homes should be the same. If the supply of mobile homes is perfectly elastic then following the interest rate change (assumed to be cut in half) the quantity of mobile homes will expand until the rental value is also half what it was before.

The supply of land is fixed and on the reasonable assumption that demand to rent land (and therefore rents) stays the same then the price of land will have to double to maintain the same rate of return as on mobile homes (arbitrage will ensure this outcome).

Is there something wrong with my logic ?

Scott Sumner

Jan 22 2021 at 6:15pm

Nick Rowe’s analysis suggests that land prices would not double, as that would make land less affordable.

Market Fiscalist

Jan 22 2021 at 7:47pm

I think Nick is saying that if r falls by half and prices double then houses become less affordable because mortgage payments are now higher (same interest payments but a bigger principal) and a bigger down-payment is needed.

While this is true I don’t why it would stop this price increase from taking place in any case (I think you claim that prices would less than double ?). People would bid the prices of houses up to the point where the return is the same as on other assets irrespective of the fact that houses are less affordable for mortgagees.

Scott Sumner

Jan 23 2021 at 12:48pm

You have not told me what’s wrong with Nick’s argument.

Market Fiscalist

Jan 23 2021 at 2:07pm

There is nothing wrong with Nick’s argument. It was your statement “But if consumer preferences did not change, then this [land prices doubling] cannot be the equilibrium outcome. Instead, price will rise by less than 100%, and the added negative of higher down payments will exactly offset the added benefit of lower monthly loan payments (due to lower interest rates.)” because this outcome would leave arbitrage opportunities for land renters.

I agree though that if one looks at houses as “house/land hybrid[s]” then a halving of interest rates would not lead to a doubling of the price of the “house/land hybrid”

Scott Sumner

Jan 24 2021 at 1:36pm

But Nick’a claiming that arbitrage is constrained by “down payments”.

john hare

Jan 22 2021 at 4:21pm

The supply of buildable land is finite, but not fixed at this time. Here in Florida, tens of thousands of acres of former swamp and citrus grove is being developed. And there is far more available with a bit of travel.

Scott Sumner

Jan 22 2021 at 6:10pm

I was discussing the supply of land, not the supply of buildable land.

Market Fiscalist

Jan 24 2021 at 3:36pm

I’m not seeing that. Both in his tweet that you link to and his comment below he says that with fixed supply of land prices will double and yields half. By implication higher down payments will not prevent this from happening so whatever ‘constraints on arbitrage’ these higher down payments may impose they will be ineffective.

Alan Goldhammer

Jan 22 2021 at 5:37pm

The biggest factor IMO is location. Our 1955 split is inside the Capital Beltway and walking distance to Metro (assuming no pandemic, it is a 15 minute subway ride to downtown DC). Our land is 3/4 of the assess valuation by property tax standards and our home will likely be torn down by who ever purchases it. Interest rates in our region make no difference at all. Houses sell within a week of being put on the market and there was a lot of buying between April and September in our area.

If and when we move, selling to a builder might be the best bet as we can get an all cash deal without a broker’s fee.

Scott Sumner

Jan 22 2021 at 6:11pm

You said:

“Interest rates in our region make no difference at all.”

What evidence do you have for that claim?

Jose Pablo

Jan 22 2021 at 7:33pm

If you are a Real Estate investor, the value of a house is the annual Net Operating Income that you get from that house, divided by your discount rate. And the house is a perpetuity since it will be providing income “forever”. So, if the investors discount rate halves the value of the property doubles.

The fact that you own your house should not change that valuation in principle since “owning” your house basically means that you are saving that very same Net Operating Income (in this case the difference between the rent you will be paying for a similar house and the actual costs of the house you own).

The ability to build new houses can, for sure, affect this … but by not that much, since the supply of “the house you like” is very inelastic. After all, it is just impossible to build a new house in the same place and exactly like the one you like no matter the price you are willing to pay.

Scott Sumner

Jan 23 2021 at 12:56pm

You said:

“The ability to build new houses can, for sure, affect this … but by not that much, since the supply of “the house you like” is very inelastic.”

Not in Texas! Sure, no two houses are perfect substitutes, but they are close enough that new construction substantially holds down price increases. The population in Texas has soared, and yet house prices remain far lower than in NY or CA.

Jose Pablo

Jan 23 2021 at 3:11pm

Roughly 6,0 million homes were sold in USA in 2019 of which only around 11% (682k) were newly constructed. In Texas, the % of newly constructed homes sold was about 33% (108,074 out of 357,238). So you are, very likely, right: newly constructed homes have a great influence in Texas housing prices. But at the same time, it does not seem very representative of the average American housing market.

But in any case, it is still true that if you halve the “real estate investors discounting rate”, prices will double “ceteris paribus”. In this “model” the offer of new houses will influence the rental prices but for a given rental price (or more precisely for a given Net Operating Income) prices double when discount rates halve (in Texas and everywhere).

There was an article in The Economist a couple of years ago (if I remember well) making reference to an analysis performed for the English housing market, trying to separate the effect on prices for different local markets of the interest rate and the supply-demand situation for that particular market. The conclusion was that interest rates changes were, by far, the biggest influence in the observed price evolution (I am sorry for the very vague reference. Will try to find it).

Residential real estate investments provide a very stable income and are highly leverageable. It makes financial sense prices being (very) influenced by the debt interest rates available for the asset.

Todd Ramsey

Jan 23 2021 at 10:01am

Help please.

“Instead, price will rise by less than 100%, and the added negative of higher down payments will exactly offset the added benefit of lower monthly loan payments (due to lower interest rates.) ”

Could you possibly explain in lay terms why down payments would NECESSARILY increase?

Scott Sumner

Jan 23 2021 at 12:54pm

The assumption is that down payments are positively related to the size of the loan. That seems plausible to me.

Todd Ramsey

Jan 24 2021 at 9:27am

Thank you. I was searching several layers too deep for the explanation.

Nick Rowe

Jan 23 2021 at 10:28am

Hi Scott!

Let’s start with a simple model, where a fixed stock of land is the only asset.

Now everyone lives twice as long in retirement, so wants to save twice as much for retirement. (It’s only approximately true they would want to save twice as much, but let that pass.)

So the price of land doubles, and the yield on land halves.

Now let’s add in the Dutch, who create new land, in response to that higher price. (Mobile homes are like the Dutch).

The only difference that makes is that the price of land wouldn’t rise as much, so yields wouldn’t fall as much.

But then I could get back to my original thought-experiment, by assuming an even bigger increase in longevity, big enough that the price of land still doubles, and yields still halve, despite the Dutch creating new land.

Nick Rowe

Jan 23 2021 at 10:56am

Though, it’s true: land rents would fall, if the Dutch created new land. So yields could halve, while land prices would rise by less than double.

Scott Sumner

Jan 23 2021 at 12:53pm

Thanks Nick. I was mostly try to flesh out some implications of your claim that you left unsaid. If something becomes more “unaffordable”, doesn’t that impact the equilibrium price?

Based on your second comment, I think we agree.

Ted Durant

Jan 23 2021 at 5:27pm

First, Scott’s dead on with treating “houses” as packages of land and structure. Structure is a depreciating long-life consumption good, as Alan noted with his comment about his house being a likely tear-down. Land is an asset whose returns (therefore value) depend on how it’s being used (“consumed”). The distinction between “buildable” and “not buildable” is very important when talking about home prices. Texas is a good example … Arizona another … where the marginal cost of turning vacant land into a buildable lot is quite low. The total supply of land is roughly fixed, but land can also be made unavailable for building (for example, bury a bunch of toxic waste in it).

Second, houses and money are complementary goods. Not everyone who buys a house has enough money, so they have to borrow some in order to buy a house. (Note, however, that a large number of house purchases are made without loans…and in certain markets at certain times, cash buyers are the predominant marginal buyers.) Everyone who owns a house with sufficient equity, income, and credit score has the ability to borrow money at a reduced rate (relative to someone with no assets as collateral). The mortgage interest rate is the price of money, in this context, NOT the price of housing.

The general interest rate is also a) an input into the discount rate used to value assets from the stream of value one derives from owning them; and b) the cost of consuming now vs saving and consuming later.

All relationships between interest rates and home prices flow from there. Any statement about the relationship between interest rates and home prices needs to be able to explain the early 1980’s … especially in Texas (West South Central, in general).

robc

Jan 24 2021 at 8:28am

The distinction between buildable and unbuilable land is important. The dutch arent creating new land, they are just converting it to buildable by getting rid of the excess water.

Brandon Berg

Jan 24 2021 at 11:10am

I’m not sure that the assumption of the required down payment being a fixed percentage of the sale price holds. Historically a 20% down payment was expected, but my understanding is that this is no longer the case, and that houses can be purchased with a 10%, 5%, or even lower down payment, probably as a response to the difficulty of saving up a 20% down payment with prices inflated by low interest rates.

Scott Sumner

Jan 24 2021 at 1:39pm

You don’t need to assume a fixed percentage, just a positive correlation between price and down payment, which seems likely.

Jose Pablo

Jan 24 2021 at 4:43pm

Although the basic assumption makes sense: assuming a fixed Loan to Value, increasing prices of the asset mean increasing down payments, real mortgage markets frequently depart from this.

When the mortgage market is very active, financial institutions soon start competing in two fronts: more “generous” appraisals and higher Loan to (appraised) Values … and it kind of make sense, since rapidly rising prices mean the market alone will bring Loan to Value back in line in a short period of time.

These dynamics resulted in not down payments at all required in the 2007-08 housing boom.

bill

Jan 24 2021 at 6:10pm

A new land regulation regime in California would change things up. The zoning regulations are creating an artificial scarcity.

Comments are closed.