The government recently announced that the 12-month rise in the CPI slowed from 8.5% in March to 8.3% in April. But this is not good news, as inflation is actually getting worse.

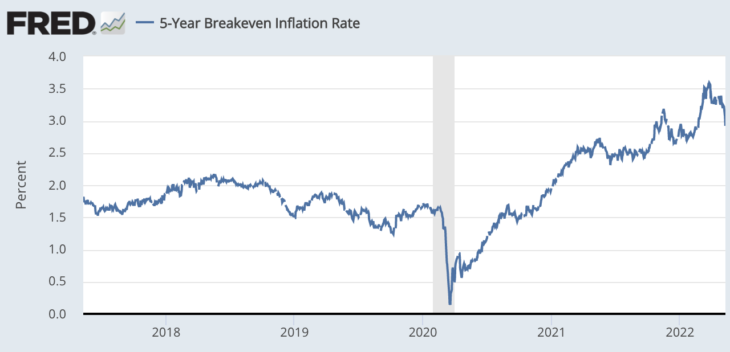

People have become used to thinking of inflation in a “let bygones be bygones” fashion. Don’t cry over spilled milk; let’s focus on the inflation rate going forward. That might be appropriate under the Fed’s old inflation targeting regime, but is not appropriate under average inflation targeting. Consider the following graph of 5-year TIPS spreads:

With the recent decline, 5-year TIPS spreads are about the same as 6 months ago, albeit still higher than a year ago. But the situation is much worse than it looks. To see why, consider the following example:

Suppose that in 2021, 5-Year TIPS spreads were 3%, and they remained 3% in 2022. Also assume that inflation was 8% during 2021-22. Then investors in 2021 would have been forecasting a total of roughly 15% inflation over 2021-26. In 2022, investors would be forecasting a total of roughly 20% inflation over 2021-26 (8% + 4*3%). In that case, the forecast inflation rate for 2021-26 would have risen from 3% to 4% [(8% + 4*3%)/5] between 2021 and 2022. That’s not a big problem under inflation targeting, but it is a big problem under average inflation targeting where past inflation rates matter. This is why the inflation problem is getting steadily worse, even as inflation forecasts stay around 3%.

Today’s report showed a 0.6% jump in the core CPI, perhaps the single most discouraging data point in the past year, so it’s not just food and oil. The Fed remains behind the curve. This reminds me a lot of the 1970s; where during the early stages of the Great Inflation there was lots of excuse making, lots of people denying the reality of excess demand. There was also a (false) perception that Fed policy had tightened because interest rates had increased, even though interest rates do not measure the stance of monetary policy.

Christopher Waller recently suggested that it wasn’t just the Fed that failed to predict the surge in inflation. That’s true. But the problem with Fed policy is not that they failed to anticipate the rise in inflation, it’s that they’ve (de facto) abandoned FAIT. Under a credible FAIT regime, the market will do the forecasting. Even if the Fed is behind the curve, the markets will tighten policy by pushing up rates in anticipation of the future Fed tightening required to produce an average inflation rate of 2%. Without that commitment, the markets will not engage in stabilizing speculation and the Fed’s job will become much harder. Without FAIT, the Fed actually does have to become a sort of Nostradamus. It does have to accurately predict inflation and know exactly when to raise rates.

PS. Yes, FAIT is not the same as simple average inflation targeting of 2%. But using any reasonable interpretation of FAIT the Fed has abandoned its new policy regime. For instance, James Bullard once suggested that FAIT was sort of like NGDP level targeting, but NGDP growth is also far too high relative to trend. And given the recent decline in the labor force, one could argue that NGDP should be below trend.

READER COMMENTS

Qian

May 12 2022 at 10:56am

What is the alternative monetary regimes if Fed cannot overcome the problem of the commitment failure?

Is free banking a better regime in stabilizing NGDP?

Scott Sumner

May 14 2022 at 12:22pm

I don’t see free banking as an alternative monetary regime, rather it’s an alternative banking regime (which I favor).

Of course free banking could be combined with a gold standard, or something like a Bitcoin standard. But I would not recommend going in that direction.

Michael Sandifer

May 12 2022 at 4:17pm

I take your point that being really vague with the definition of FAIT+ is a problem, with negative consequences now being manifested. However, it seems much more plausible that the Fed sees its target as asymmetric. Afterall, if it is an AIT, and Powell says inflation doesn’t have to run X% below 2% to make up for periods of X% above 2%, what else should be concluded? And this makes sense from the perspective of the Fed’s stated goal of adopting FAIT+, which was to have more effective monetary policy near the ZLB and to maximize employment.

Hence, why can’t the Fed just issue forward guidance now in the form of further definition of its target by saying that, for example, they want inflation to be X% in 10 years, which would mean the average rate over 10 years would exceed 2%?

In that case, they’re either giving up on a definite 2% average figure, or they’re just still refusing to define a time frame over which a 2% average might apply. It seems the former would make more sense, as failing to define a time frame for a mean is useless. So, they could say they aspire to 2% average inflation, unless their employment mandate calls for a higher average rate.

Of course, the employment data suggests that, if anything, employment is perhaps too low at the moment, given the supply constraints on the economy, at least, so this does not save face for the Fed. It’s hard to escape the conclusion that they’ve screwed up.

They’ve stated they plan to review “monetary policy strategy, tools, and communication practices roughly every five years.” They can’t even be precise with that time frame.

https://www.federalreserve.gov/monetarypolicy/review-of-monetary-policy-strategy-tools-and-communications.htm

Hopefully, they adopt NGDPLT in a few years.

Scott Sumner

May 12 2022 at 5:34pm

” . . . it seems much more plausible that . . . ” That’s exactly the problem. We shouldn’t have to guess.

Michael Sandifer

May 14 2022 at 1:54pm

Yes, exactly.

Michael Rulle

May 13 2022 at 9:17am

The Fed blew its inflation forecast——-they got it wrong——the biggest surprise is how large the miss has been. You have mentioned more times than I can count that if the Fed wanted to lower inflation (or raise it) they could.

If only the equilibrium rate were observable. But it isn’t. Maybe that is why he could never figure out a way to implement FAIT——as he never said how he would do it. He does not want a recession. But the longer he goes without lowering inflation the worse the recession will be.

Since we know he has denied FAIT—-is there a second best? We never had FAIT before. If we were to get back to 2% isn’t that better than what he is doing—-which appears to be nothing. I think he still believes transitory is the truth. And he is waiting for Godot.——

Grand Rapids Mike

May 13 2022 at 11:32am

The inflation discussion needs to recognize the politics involved. Powell wanted to be renominated to the Fed. This constrained him in stating the obvious. There was no way he would start increasing interest rates, reducing the MS until his renomination was in the bag. Now it’s too late, inflation expectations are imbedded and almost supported by no attempt to increase energy supplies.

Capt. J Parker

May 13 2022 at 4:55pm

If I may, I’d like to put a plug in for this podcast where David Beckworth interviews Peter Ireland. I think that Scott Sumner fans will like it. They cover a lot of the same things Dr. Sumner has been saying:

Fed seems to have abandoned FAIT

The Phillips curve still seems to cast too long a shadow.

And a point made Robert Hetzel that Dr. Sumner pointed us to, namely that the optimal way for the fed to handle the dual mandate of stable prices and full employment is to credibly stabilize the path of prices and then market forces will take care of full employment.

Beckworth and Ireland are both NGDPLT advocates.

Thomas Lee Hutcheson

May 15 2022 at 9:43am

I think I now understand your point that the Fed has changed policy away from average inflation targeting including some amount of already occurred inflation in the average.

Whether this is a good thing come down to how well the Fed CAN predict the effects of its instrument settings. And TIPS markets are valuable input into this. Don’t we WANT the Fed to “look through” surprising real shocks, that require greater than target inflation for a while.

Comments are closed.