The Economist has an article on what the 1980s can teach us about solving the inflation problem:

So the experience of the 1980s may become instructive. And once you dig into the history, the decade holds three tough lessons for today’s policymakers. First, inflation can take a long time to come down. Second, defeating inflation requires the participation not just of central bankers, but other policymakers too. And third, it will come with huge trade-offs. The question is whether today’s policymakers can navigate these challenges.

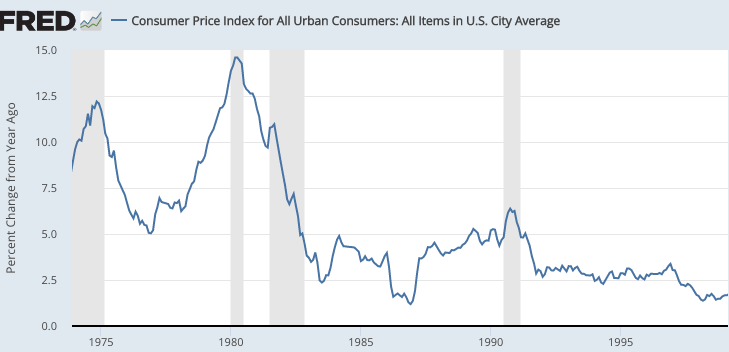

The first two points are incorrect, at least for the US. Inflation was brought down relatively quickly after Paul Volcker finally adopted a tight money policy in mid-1981. The 12-month inflation rate fell from 14.3% in June 1981 to 3.8% in December 1982. And this was done with no help from fiscal policy, as the newly elected President Reagan slashed taxes and boosted military spending. Some Keynesian economists (wrongly) suggested that this fiscal stimulus would lead to high inflation. (There was a modest payroll tax increase in 1983, but by that time the inflation problem had already been solved.)

The Economist is right about the trade-offs. When inflation has become entrenched, bringing it down to much lower levels can cause a recession. It’s too soon to know what will happen in 2023 (our current inflation problem is less severe than in 1981), but the risk of recession is clearly higher than during a normal year.

PS. You can argue that Reagan’s tax cuts made the disinflation less painful than otherwise, but they did not cause the disinflation.

READER COMMENTS

zeke5123

Dec 21 2022 at 10:46am

Maybe the problem is equivocation in terms, but I think how inflation is used in the everyday sense is that prices are rising. The general formulation of this is too many dollars facing too few goods.

So, it follows there could be two ways to tackle inflation: (1) reduce the number of dollars in circulation keeping goods constant or (2) increase the number of goods keeping dollars constant.

The argument I’ve heard is that Regan’s policy increased supply while Volcker’s policies decreased money in circulation. Now, either (or both) may be wrong factually. But can you explain why as a matter of theory that is wrong?

Scott Sumner

Dec 21 2022 at 12:19pm

Once can certainly make that claim, but it’s factually false in this case. Inflation came down after 1981 because NGDP growth slowed sharply, RGDP growth under Reagan wasn’t much different from during previous administrations.

Thomas Lee Hutcheson

Dec 22 2022 at 7:38am

Plus the increase in the deficit from the tax cuts reduced long term growth

Spencer

Dec 22 2022 at 10:09am

N-gDp growth came down sharply because of the 2-year distributed lag effect of money flows. You could see the stock market bottom 1 1/2 years before it took place.

Spencer

Dec 21 2022 at 11:01am

Beautiful. And Volcker screwed up again in 83, supplying an excessive volume of required reserves.

You have to be deaf, dumb, and blind, not to see causation. The “time bomb” which Dr. Pritchard predicted, the widespread introduction of NOW accounts, etc., vastly accelerated the transactions velocity of funds in the 1st qtr. of 1981 forcing N-gNp up to 19.2%.

Then Volcker applied legal reserves to NOW accounts in April 1981. All the decreases in the volume of legal reserves forced AD immediately down. I.e., monetarism has never ever been tried.

Under monetarism, the FED’s monetary transmission mechanism is legal reserves, not interest rate manipulation.

Spencer

Dec 21 2022 at 12:16pm

re: “Volcker’s policies decreased money in circulation”

The DIDMCA of March 31st did that.

…

Professor emeritus Leland James Pritchard (Ph.D., Chicago Economics 1933, M.S. Statistics) never minced his words, and in May 1980 pontificated that:

“The Depository Institutions Monetary Control Act will have a pronounced effect in reducing money velocity”.

…

The error in macro is that banks act as intermediaries: “None of this would matter if the Fed acted as an efficient savings-investment intermediary, as commercial banks are able to do, at least in principle.” And: “This is nonsense, Spencer. It amounts to saying that there is no such things as ‘financial intermediation,’ for what you claim never happens is precisely what that expression refers to.” And: “Yes, I hold that commercial banks are credit intermediaries and not just credit creators” — George Selgin

…

35 years ago, Dr. Pritchard said the same thing as Dr. Philip George’s: “The Riddle of Money Finally Solved”. To wit: “For nearly a century the progress of macroeconomics has been stalled by a single error, an error so silly that generations to come will scarcely believe that it could have persisted for as long as it has done.”

George: “The logic was that such precautionary holdings are not intended to be spent and hence do not qualify as money.”

…

It’s stock vs. flow. Banks don’t lend deposits. Deposits are the result of lending. It is hard for the average person to believe that banks do not loan out savings or existing deposits – demand or time. But the DFIs always create money by making loans to, or buying securities from, the non-bank public.

Comments are closed.