I’ve never seen much merit in Real Business Cycle theory. I’ve long accepted the standard Keynesian view that high unemployment is a grave evil – not an optimal response to adverse conditions – and that recessions are almost entirely caused by declines in Aggregate Demand. The Great Depression was not a Great Vacation; it was a disaster caused by the fatal combination of nominal wage rigidity and falling Aggregate Demand. Yes, Aggregate Supply matters too; indeed, Aggregate Supply is virtually the only thing that matters for long-run prosperity. Yet Aggregate Supply explains little about short-run business fluctuations, because Aggregate Supply rarely sharply changes in a year or two. Even the infamous 1970s oil shocks were tiny relative to GDP.

I hate to say, “This time it’s different.” I’ve repeatedly bet against such claims. Alas, this time probably is different. The sudden shutdown of enormous sectors of the U.S. and global economy clearly constitute a massive short-run fall in Aggregate Supply. While Aggregate Demand is going to fall too, this time Aggregate Supply fell first. This time, tens of millions have effectively begun a Great – but Sad – Vacation.

This combination is almost unprecedented. Countries at war have often faced a combination of falling Aggregate Supply and rising Aggregate Demand – primarily when they’re being invaded. But falling Aggregate Supply and falling Aggregate Demand simultaneously? Weird indeed.

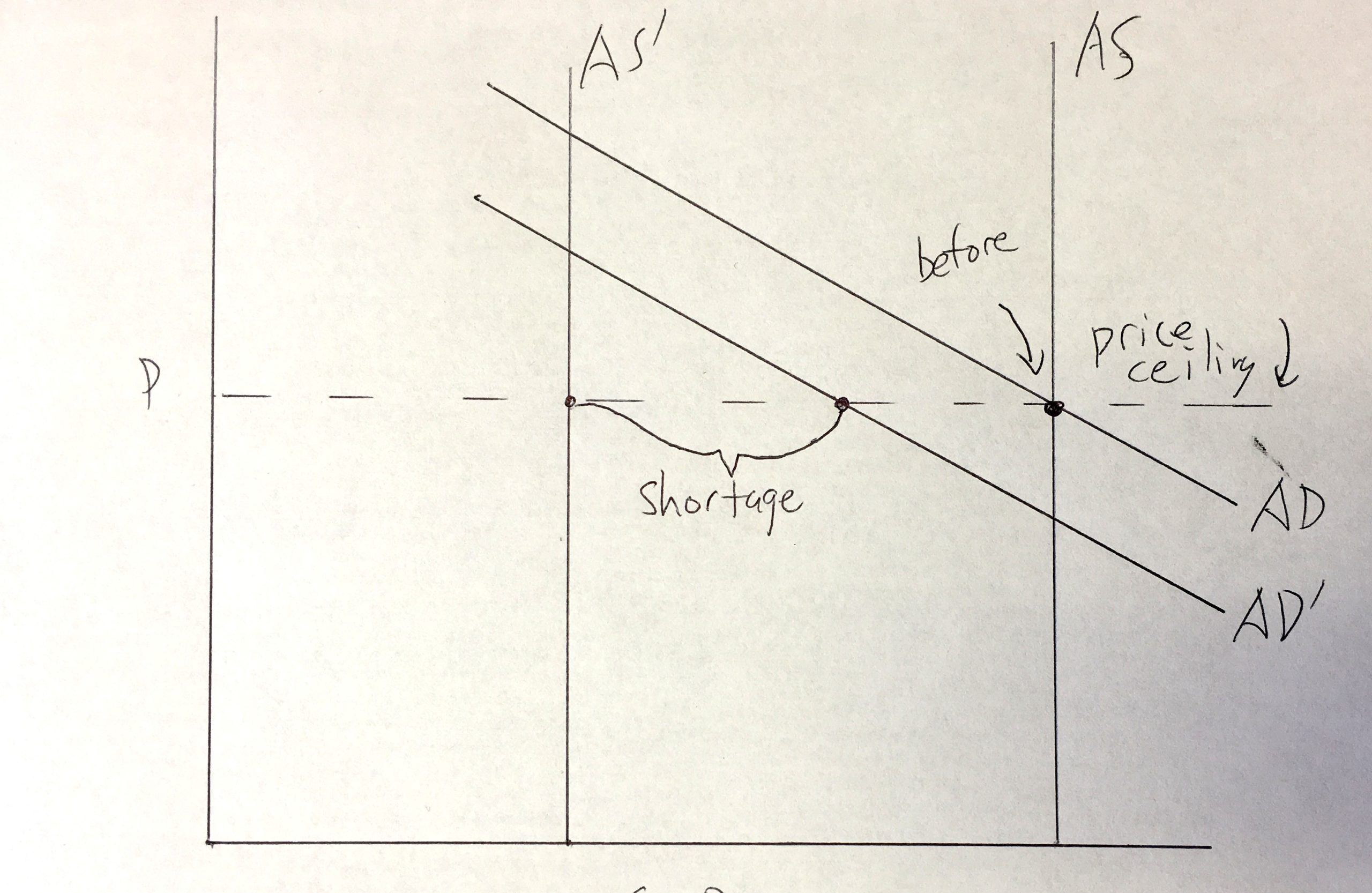

Weird, but not exotic. We can analyze it with the standard textbook model. When AS and AD both fall, GDP definitely falls. Theoretically, however, inflation could either rise or fall. This in turn largely depends on the relative size of the shifts. If AS falls a little and AD falls a lot, we can count on the familiar pattern of low inflation or even deflation (which we briefly experienced last time around). If AS falls a lot and AD falls a little, in contrast, we should expect a return of stagflation – high unemployment and high inflation simultaneously. The same holds if AS falls enormously and AD “only” falls a lot. Like so:

The upshot: Though I’m not ready to bet on it, I fear that in 2021 we will see not only high unemployment but high inflation as well. (Complication: Official statistics may classify disemployed workers as “out of the labor force” because they’re too scared to hunt for a job). At this point, I would not be surprised by 10% unemployment and 6% inflation for 2021.

Yes, we should never forget base rates. Stagflation hasn’t happened for decades, so we should be skeptical about its imminent return. And yes, we should be ever-mindful of focusing illusion; as Kahneman explains, “Nothing in life is as important as you think it is, while you’re thinking about it.” I’m thinking about coronavirus most of the time now, so I tend to overrate it. Yet even taking these biases into account, I readily believe that we’ll have stagflation next year.

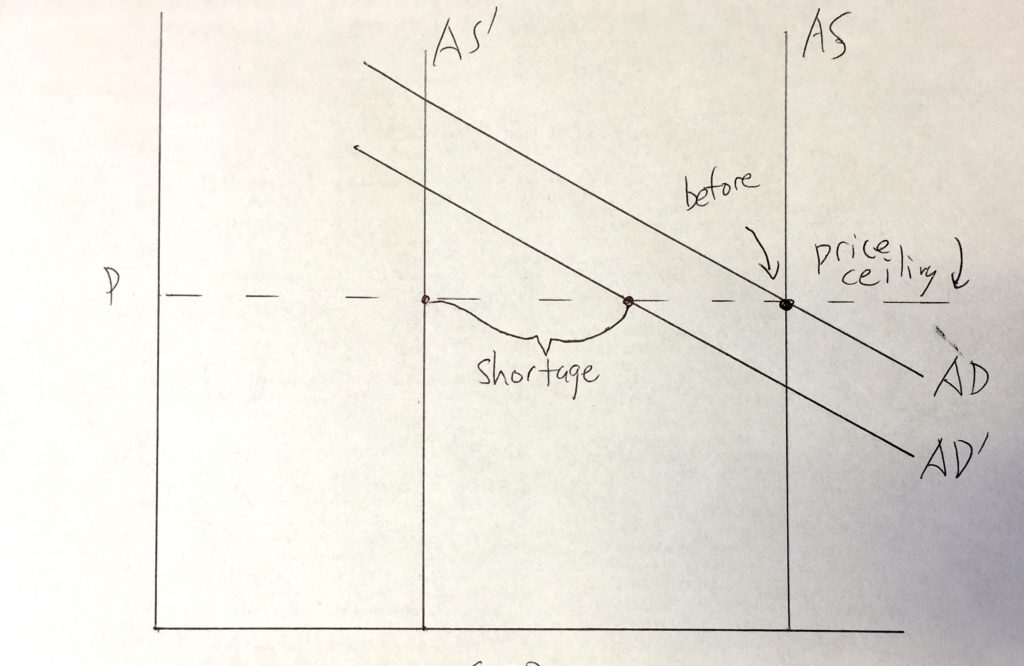

How bad will the inflation be? Again, I share the standard Keynesian view that moderate inflation by itself is no big deal. Yet the public outcry against even high single-digit inflation will be deafening. Historically, governments have a standard response to such outcries: economy-wide price controls. Richard Nixon imposed them in 1971 when inflation was only 4.4% and restaurants were open. If and when the government does impose price controls, the textbook tells us what to expect: Ever-growing shortages, rationing, black markets, and anti-business witch-hunts. We see this when government merely caps the price of a single good, such as apartments. When government caps the price of everything, we face dire economic chaos. Like so:

Optimists will say, “Price controls?! Come on, U.S. policy-makers learned their lesson last time.” I cannot assent. Few policy-makers even remember the 1970s. Many of those who do remember what happened failed to absorb the textbook explanation. Many of those who absorbed the textbook explanation at the time have forgotten it. And once price controls get on the agenda, the few policy-makers who know the damage they’ll cause will probably go with the demagogic flow. I doubt even the CEA will loudly protest: “Price controls would normally be a bad idea, but given our nation’s ongoing emergency…”

Tell me I’m wrong, please.

READER COMMENTS

Ray

Mar 18 2020 at 9:45am

Sounds like a good opportunity for one of your bets, Bryan. 🙂

Garrett

Mar 18 2020 at 9:47am

This is why the Fed should’ve done what Scott Sumner recommended a decade ago and change their language to be on Nominal Gross Domestic Income (NGDI, which equals NGDP) instead of inflation. The public does not understand inflation in the way the Fed discusses it (and sometimes it feels like some Fed governors don’t either), but if the communication was “we need to keep nominal incomes on track through this recession” the public would understand and appreciate that much better than “we need to raise prices on goods and services during this recession.”

Todd Ramsey

Mar 18 2020 at 10:15am

You’re wrong, Bryan.

In the 1970s there was far less understanding that “inflation is always and everywhere a monetary phenomenon”. The Friedman and Schwarz Monetary History of the United States had been published only ten years prior, and was not yet broadly accepted or understood.

Undergrad Econ textbooks presented models of “Demand-pull” and “cost-push” inflation. The President promoted a plan to stop inflation by encouraging everyone to wear a button!

I suspect we’ll pursue lots of unwise policies, but I don’t think widespread price controls will be among them.

I hope.

Philo

Mar 18 2020 at 11:39am

Price controls constitute decisive, direct action by government to address a concern upon which ordinary voters will be focused: rising prices. Therefore, it will seem to ordinary voters that price controls are desirable. It matters little whether economists know they are bad policy; politicians will be under irresistible pressure to adopt them, and will probably do so. Compare: rent controls, anti-price-gouging regulations.

Thaomas

Mar 18 2020 at 2:43pm

Some increase in inflation — enough to keep NGDP rising at about its current rate when real income (supply) is falling — would probably be the best we can do. My guess is that the Fed will again be too timid to keep NGDP on track.

someguy

Mar 18 2020 at 3:16pm

Been thinking about something like this…(note i am but a lay person in the gallery).

To the extent that any upcoming fiscal stimulus overshoots or is mistargeted, and people have extra money, but dont know what to do with it, they will start bidding up the price of some goods. Combine that with supply disruptions, limiting goods availability…boom! Maybe I’ve just stated an obvious lay version of your piece above?

Related, I would expect price controls and rationing within a month or two if there are any deeper issues with essentials like toilet paper or food in the supply chain.

Noel Ngundu

Mar 21 2020 at 3:59am

You’re spot on, someguy…a stimulus program will just increase the money supply at a time when aggregate supply is falling, and that’s likely to be inflationary.

Mark Z

Mar 18 2020 at 3:24pm

Certain states (including my own) whose leaders are openly antipathetic to markets in general will probably impose restrictions on ‘price gouging.’ I think that’s nearly a certainty. It may not happen at the national level, but I am absolutely certain that my mayor, governor, and likely every single member of the city council (I live in one of those ridiculous places that elects actual socialists to pubic office) never has nor ever will understand why price controls cause shortages. The only question is which state will be the first, after whom some others will likely follow.

Anon.

Mar 18 2020 at 4:06pm

5 year TIPS implied inflation rates have dropped from 1.6 to 0.16 over the last couple of weeks, so if you want to bet on inflation there’s definitely a good opportunity for it.

Thaomas

Mar 18 2020 at 4:43pm

@ anon.

I don’t want to bet; I want the Fed to act. With no NGDP futures market in existence yet, it needs to target inflation expectations, i.e., the future price level as indicated by TIPS (unless there is something better that I don’t know of.) If it expects a 5% hit to real output, it needs to target at least 7% inflation and let markets know that is the target.

Scott Sumner

Mar 18 2020 at 5:18pm

I agree that both AS and AD are falling. I don’t know which is most important, but it’s worth noting that the markets seem to be forecasting lower inflation.

Warren Platts

Mar 18 2020 at 5:58pm

If I understand you correctly, Bryan, then maybe a Keyesian $1000/head, and/or a bunch of monetary/fiscal stimulus is not the thing to do this time around.

Because if AS falls a lot, maybe instead heroic measures to prop up AD, it might be better if AD also fell a lot in order to keep the price level relatively flat over time. That would at least eliminate the political pressure for price controls.

Besides, what’s the point of handing out a lot of cash if there’s nothing to buy…

Noel Ngundu

Mar 21 2020 at 4:08am

I absolutely agree with you Warren…pumping more money into the economy when production is declining is insane…it will only push prices up!

bill

Mar 18 2020 at 6:12pm

I doubt this is correct, but in theory, the market prediction of a 0.16% 5-year CPI could be incorporating a prediction of price controls. CPI is like 25% housing/rent, and predicting rent controls right now is not outlandish.

Alex Schell

Mar 18 2020 at 10:55pm

Happy to bet, how about this:

If the 12-month percent change in the core PCE price index exceeds 3.5% for any month between March 2020 through August 2021 inclusive, Alex pays Bryan $x. Otherwise Bryan pays Alex $x.

For x up to $500. Happy to prepay and let you judge the outcome.

BC

Mar 19 2020 at 12:05am

Aren’t price controls, either official or cultural, a large part of why we are in this present mess? Of course, we already see shortages of masks, toilet paper, and other goods mainly because of either actual laws against “price gouging” or just a cultural taboo against surge pricing. (Strange how even during unusually heavy traffic situations we don’t run out of Uber drivers and, coincidentally, Uber implements surge pricing…)

But, our two largest problems right now are a shortage of tests and the potential that hospitals will be overwhelmed by a surge in COVID-19 cases. Might flexible prices for coronavirus tests help us direct limited tests to the highest-value uses, for example people that we really don’t want socially distancing right now if a test could determine that they and those around them are not infected because we really need them to do certain jobs? Might a market for reserving treatment capacity (e.g., ICU slots, ventillators, etc.) internalize costs and benefits of social distancing? And, might such markets (along with removing regulatory barriers) have *predictively* directed suppliers to boost production of tests, masks, ventilators, temporary/scalable hospital capacity, etc.)? Instead, because we are totally cut off from our most effective known means of communicating information and co-ordinating activities on a mass scale — price signals — we consign ourselves to co-ordination by jawboning and daily press briefings. The result has been that we can do no better than just shut down the entire economy for 1-2 months (optimistically, by the way) out of an abundance of caution.

Michael Sandifer

Mar 19 2020 at 9:55am

I think Bryan is correct that the price control scenario seems plausible, if we end up with high inflation. It doesn’t comfort me much that standard textbooks teach that price controls are bad. They also teach that trade barriers are bad.

That said, I think it’s unlikely that we have a sustained period of above 2% inflation at this point. Both the stock and bond markets are strongly signaling that disinflation is the concern going forward, as of now.

Matthias Görgens

Mar 19 2020 at 12:21pm

Don’t you already have lots of price controls due to emergency measures in many of your states? (Definitely California.)

Maciej

Mar 24 2020 at 7:41am

A voice from Poland, Europe:

Bryan, your scenario is already happening for safety masks, suit, goggles and disinfection sprays in Poland. We have price controls, restriction of private trading in these goods and a supply gap.

It could evolve this way for groceries, if the panic buying lasted 1-2 weeks more.

For 2020/21 a key factor is that the gov’t does not stimulate the AD too much. But for the people in power, it’s a political suicide. And that is why I fear this scenario is quite real. 🙁

Comments are closed.