The NYT has a piece discussing the Fed’s gradual reduction in bank capital requirements:

Some of the changes, seemingly incremental and technical on their own, could add up to a weakening of capital requirements installed in the wake of the crisis to prevent the largest banks from suffering the kind of destabilizing losses that imperiled the United States economy. Another imminent change will soften a rule intended to prevent banks from making risky bets with customer deposits.

Translation:

“Another imminent change will soften a rule intended to prevent banks from making risky bets with taxpayer insured funds.”

After the banking crisis, Congress passed the massive Dodd-Frank bill, which somehow “forgot” to address most of the actual causes of the crisis. One concrete step in Dodd-Frank that its supporters often point to was the higher capital requirements. But now that’s also being chipped away.

In a perfect world, there would be no capital requirements at all, but also no FDIC, no t00-big-to-fail, no Fannie Mae and Freddie Mac, no FHA, etc. Given all the moral hazard in the system, there needs to be some way of discouraging excessive risk-taking.

Deregulation doesn’t always reduce the footprint of the government, in this case it makes the government even more involved in the financial system.

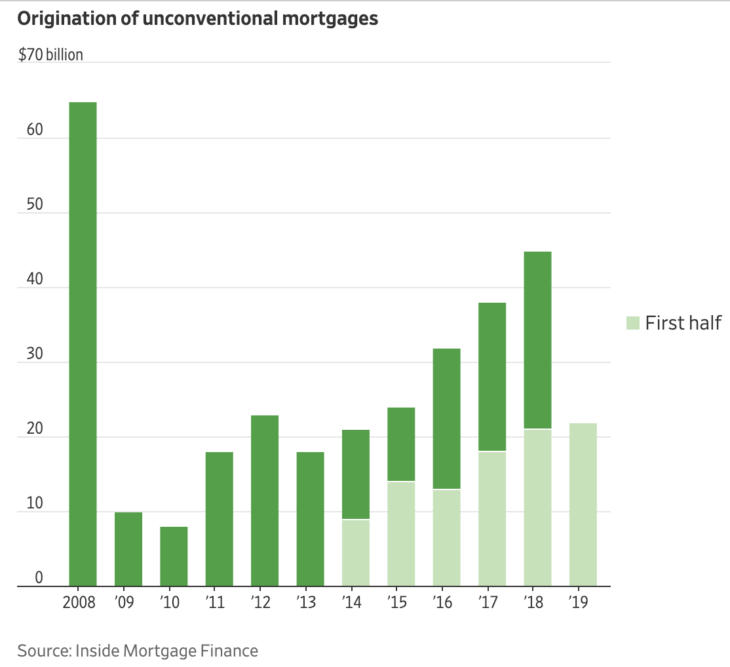

Meanwhile, the WSJ reports that “unconventional mortgages” (no longer called subprime) are on the rise again:

I don’t have strong views on the appropriate regulation of subprime mortgages. What I object to is procyclical banking regulation. We loosen regulations during booms and tighten them during recessions. Thus our banking regulators make the same error as our monetary policymakers—a procyclical policy regime that makes the economy less stable.

There’s a lot of talk about “macroprudential regulation”, but our policymakers do the exact opposite.

READER COMMENTS

Michael Sandifer

Aug 22 2019 at 10:31am

Scott,

I assume you know this, and just brushed over it for simplicity, but the FDIC is ostensibly not funded with tax dollars.

https://www.fdic.gov/about/learn/symbol/index.html

It is funded with a tax on banks and in interest earned on Treasuries.

That said, I think I vaguely remember talk about the FDIC possibly running out of money during the financial crisis. I suppose it’s not impossible for taxpayers to be on the line. And again, it may create some moral hazard, at least for depositors.

Mark Z

Aug 22 2019 at 1:41pm

Doesn’t this just mean risk is socialized among banks, rather than among the general public? So risk averse banks end up subsidizing risk seeking banks.

Scott Sumner

Aug 22 2019 at 5:12pm

Michael, You contradicted yourself, saying it’s not funded with tax dollars, and then saying its funded with a tax on banks (which is correct.) As you probably know, taxes on business services are largely passed on to consumers. Think about the gasoline tax, which is “ostensibly” (to use your term) paid by gas stations, not consumers. Or the employer share of the payroll tax.

Michael Sandifer

Aug 22 2019 at 10:32am

And the TARP bailout was paid back in full, with interest, ahead of schedule, as I recall. Banks didn’t like many aspects of TARP, though such programs certainly may also create some moral hazard.

Scott Sumner

Aug 22 2019 at 5:14pm

The main problem is the smaller banks. Look at the risks that Bank of the Ozarks is currently taking. It may all work out fine for that particular bank—but that’s deposit insurance at work.

Alan Goldhammer

Aug 22 2019 at 11:44am

It would be good to go back and listen again to Russ Roberts’s interview with Anat Admati on Econtalk: http://www.econtalk.org/anat-admati-on-the-financial-crisis-of-2008/ She highlights the problems with have too low capital requirements on banks. I was prompted to read her book on the subject which was somewhat scary. It’s all well to argue for deregulation and let moral hazard run things but I’m not at all sanguine that this will solve anything. Look at how Wells Fargo is continuing to clean up mess after mess.

Michael Pettengill

Aug 24 2019 at 5:41pm

The biggest source of funds for mortgages in the 2000s came from banks capitalized at 100%, banks like Primary Reserve Fund, and all the other money funds. All the money comes from investors, thus 100% of all lending is from capital.

They were not insured. They had no access to Fed money. All their money came from investors risking 100% of their money.

The problem was investors first rushed to force share buy backs, then refused to risk their money by putting capital into these funds in late 2008. That contracted the shadow bank money supply by hundreds of billions in a few weeks.

Benjamin Cole

Aug 22 2019 at 8:23pm

Nice post. Some say the US banking system has been fully restored to original specs, circa 2008.

Maybe completely free markets in large financial institutions and systems would work better.

But I ponder AIG, that outfit that provided bond insurance to bond investors. It was set up by and run by the most sophisticated people on Wall Street, and sold Insurance to the most sophisticated and deep-pocketed buyers. It collapsed in 2008 like a house of cards in a zephyr. That is the private sector’s version of financial Insurance.

I would like to proceed through life without fearing that the entire financial system might collapse in any particular economic recession.

Thaomas

Aug 23 2019 at 2:59pm

The problem is not that we allow too big to fail institutions, but that when the TBTF’s get bailed out, the owners who chose too-low capitalization and the managers who executed the choice did not loose everything

Michael Pettengill

Aug 24 2019 at 5:07pm

In other words, money market funds buying securities from non-Fed banks freed from all mortgage regulations by the Bush administration preempting State regulations based on the 2000 omniibus bill passed with lame ducks voting and signing it without reading it in December they head to Christmas vacations, buying credit insurance labeled “credit default swaps” from London to be doubly free of government regulation, and mortgage originations being almost totally from not banks and thus free of regulations.

The crisis was not in the FDIC, the GSE, the regulated Fed bank mortgage originators, but in two non-FDIC, non-Fed banks, who got cash from non-FDIC or Fed or State regulated depository banks, but from businesses and individuals buying high risk shares in debt, and the very first of the “safer” substitutes for bank savings accounts, Primary Reserve Fund, with AIG’s unregulated London options trading unit running out of capital to make good on its contracts.

I’m old enough to have followed the debate over allowing retail money funds. Previously, to open such accounts you had to convince a broker you did not need the money being invested in stocks and bonds for living expenses. Fees on buying stocks and selling stocks limited the number of people holding them, being much more expensive than even buying bank CDs. But Primary Reserve Fund was seeking freedom from both the requirement the funds not be “savings” and from the transaction fees (at least for “deposits”).

A big milestone was allowing multiple “deposits” per month, and one “withdrawal” per month with no sales fee, and only a 3 day delay in getting “cash” plus the account owner signing a statement saying they were not using the fund for demand deposits, and they understood the fund could freeze sales, aka withdrawals, at any time for any length of time.

The fault was the mutual fund industry failing to “declare a bank holiday” freezing investor sales of fund shares until the investors stopped panicking. No money in money funds was needed immediately because no one would risk cash they needed for living or businesses in risky investments, and if they did, the market needed to creatively destroy them, transferring asssets to prudent capitalists.

In any case, nothing that happened from 2001 to 2010 surpised me, other than how bad the consequences were.

The failure, and reasons for failure of Primary Reserve Fund had been detailed circa 1970 in opposition to the regulations that enabled it and all the others.

And deregulation of mortgage lending had already caused a crisis, and a TARP, in the late 80s into early 90s. It is almost Ironic that both President Bushs signed almost identical TARP bills that had to be worked though by Democratic presidents, the resolution dragging down the economy in the early 90s and early 10s.

Why not consider the period of 1935 to 1975 with nothing but individual banks failing from bad lending, followed by deregulation of the FIRE sector increasing from the 70s to 2005 resulting in major bank crisis and government bailouts of savers in for 1985-1995 and 2006-2016, plus bailouts of institutions 1995-2000, (Mexico, LTCM) and 2008-2013 (GMAC, GE Capital, AIG, et al)? FDIC, GSEs were not created in the 70s, but in the 30s, ending for almost half a century banking crisises.

Scott Sumner

Aug 26 2019 at 3:04am

Michael, It’s no surprise that longstanding weaknesses in the banking system show up during disinflationary periods. It’s that way in other countries too.

Steve

Aug 25 2019 at 11:23am

Subprime is a subset of unconventional mortgages. Many unconventional mortgages are issued to prime borrowers who simply don’t fit the prescribed boxes laid out by fannie and freddie. For example, this could include self-employed (dentists, accountants, etc. without W2s) or jumbo mortgages (the cap on agency mortgages is pretty low relative to certain high housing cost areas).

If you dig into the composition of unconventional mortgages, you’ll see we’re not close to repeating 2008.

Scott Sumner

Aug 26 2019 at 3:05am

I agree that things are not as bad as in 2008.

Comments are closed.