When I studied economics, the term ‘high-powered money’ was often used synonymously with the monetary base, which consists of currency plus bank deposits at the Fed. This asset was called “high-powered” for three reasons:

1. It is determined exogenously by the monetary authority.

2. It is non-interest-bearing.

3. It is the medium of account.

As a result of these three factors, high-powered money is a sort of “hot potato”. When the Fed injects new high-powered money into the economy for reasons other than responding to an increased demand for liquidity, the public tries to get rid of excess cash balances by spending them. Prices and NGDP rise until the public is again content to hold the newly enlarged supply of high-powered money.

Today, bank deposits at the Fed earn interest, and thus are no longer high-powered money. Only currency remains high-powered.

$100 bills comprise about 80% of US high-powered money

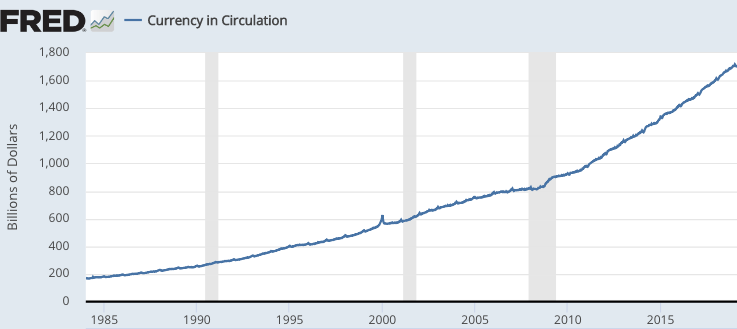

The stock of high-powered money has risen by roughly 265 times over the past 100 years, from about $6.45 billion in early 1919 to just over $1.7 trillion today. NGDP has risen by almost the same proportion, leaving the high-powered money to NGDP ratio at roughly 8.2%, even after 100 years! People seem to want to hold about the same fraction of income in the form of high-powered money as they did 100 years a go. As a result, you might say that the Fed caused NGDP to grow 265-fold by increasing the stock of high-powered money 265-fold.

Actually, it’s a bit more complicated than that. The demand for high-powered money had fallen to 5.6% of GDP right before the Great Recession, and the fortuitous coincidence of almost no change in the ratio over 100 years is actually due to two offsetting factors. Technological progress reduced the demand for high-powered money over time, and very low interest rates plus increased foreign demand for US currency recently boosted the demand for high-powered money.

Currency demand rose after rates fell close to zero

Even so, the Fed determines the long run path of NGDP via adjustments in the stock of high-powered money. (RGDP is up about 16.7 fold over the past 100 years, the rest is inflation.)

I’m hesitant to talk about MMT theory, because its proponents always insist that critics get it wrong. But unless I’m mistaken, MMTers seem to assume that money creation is an important source of funding for federal spending. George Selgin has a post criticizing MMT, and cites this passage from Stephanie Kelton, Andres Bernal, and Greg Carlock, who are MMT proponents:

As a monopoly supplier of U.S. currency with full financial sovereignty, the federal government is not like a household or even a business. When Congress authorizes spending, it sets off a sequence of actions. Federal agencies, such as the Department of Defense or Department of Energy, enter into contracts and begin spending. As the checks go out, the government’s bank ― the Federal Reserve ― clears the payments by crediting the seller’s bank account with digital dollars. In other words, Congress can pass any budget it chooses, and our government already pays for everything by creating new money.

This is very misleading. Nick Rowe has a post where he points out that money creation provides very little revenue for advanced economies, citing a rough estimate of 0.25% of GDP for Canada. If we assume 4% trend growth in NGDP in the US, then an 8% currency ratio will lead to steady-state revenue of roughly 0.32% of GDP, ignoring costs of producing money. That’s trivial compared to total federal spending, which is over 20% of GDP. Studies of the “Laffer Curve” for seignorage tend to produce maximum inflation tax revenue estimates on the order of a few percent of GDP, assuming a revenue maximizing inflation rate of several hundred percent per year.

Obviously those sorts of inflation rates are politically infeasible in the US, and hence as a first approximation it’s best to assume that money creation is not a significant source of funds to pay for government spending. Programs need to be funded with either taxes or debt, and of course debt represents future tax liabilities. The only possible exception is if the interest rate on public debt will stay persistently below the economic growth rate (as has been the case in recent years), in which case a government could earn a one-time revenue windfall by supplying the public with the extra Treasury debt it seems to crave. But it would be foolish to rely on that one-time gain to pay for expensive permanent programs such as “Medicare for all”.

In any case, whatever one’s views on the “dynamic inefficiency” argument for more federal debt, it’s misleading to claim that money creation provides a significant source of funds for government spending. Perhaps the confusion comes from the huge QE programs of the past decade, which looked to many people like a case of “monetizing the debt”. While bank reserves used to be high-powered money, today they are not (except for vault cash, of course.) In fact, QE largely exchanged one form of federal debt (T-bonds) for another (bank reserves.) QE does not pay for a significant fraction of government spending; for the most part it simply changes the maturity of the public debt.

PS. The Nick Rowe post I linked to is the best explanation of MMT that I have encountered. I also recommend the George Selgin post linked to above, as well as Paul Krugman’s critique:

[T]here are limits to the amount of real resources that you can extract through seigniorage. When people expect inflation, they become reluctant to hold cash, which drive prices up and means that the government has to print more money to extract a given amount of real resources, which means higher inflation, etc.. Do the math, and it becomes clear that any attempt to extract too much from seigniorage — more than a few percent of GDP, probably — leads to an infinite upward spiral in inflation. In effect, the currency is destroyed. This would not happen, even with the same deficit, if the government can still sell bonds.

The point is that under normal, non-liquidity-trap conditions, the direct effects of the deficit on aggregate demand are by no means the whole story; it matters whether the government can issue bonds or has to rely on the printing press. And while it may literally be true that a government with its own currency can’t go bankrupt, it can destroy that currency if it loses fiscal credibility.

Now, I am not predicting hyperinflation for the US . . . But the MMT people are just wrong in believing that the only question you need to ask about the budget deficit is whether it supplies the right amount of aggregate demand; financeability matters too, even with fiat money.

PPS. My early NGDP data comes from Balke and Gordon’s data set (actually GNP). My high-powered money data is from FRED, and from Friedman and Schwartz.

HT: Pat Horan

READER COMMENTS

Charlie

Feb 18 2019 at 7:45pm

This is not a critique. I’m here to learn! I have some questions regarding the intro:

“When the Fed injects new high-powered money into the economy for reasons other than responding to an increased demand for liquidity, the public tries to get rid of excess cash balances by spending them. Prices and NGDP rise until the public is again content to hold the newly enlarged supply of high-powered money.”

Who is the public in this context?

How do we know that the public behaves in this manner?

Jerry Brown

Feb 19 2019 at 12:02am

First thing is- MMT says that ANY time the currency issuing government spends it is creating money. And every time it taxes, it destroys money. And that the difference between taxing and spending should depend on the condition of the economy- as in too much taxing with too little spending (total spending, not just government spending) you have unemployment. Too much spending in the economy you get inflation. This is not an issue about ‘seigniorage’ as most people understand that term, although MMT would say like Nick Rowe did- take the free lunch when you can. That ‘free lunch’ will often be there to have, but sometimes it won’t, and sometimes the government might have to destroy more money than it creates through spending to avoid inflation. MMT says this generally depends on the desire to save in the currency of the private sector.

The quote you provide from Stephanie Kelton, Andres Bernal, and Greg Carlock is factually true- I’m not sure why true things are very misleading. And why would the best ‘explanation’ of MMT come from Nick Rowe rather than an MMT economist? If an explanation of NGDPLT was desired, I would recommend reading Scott Sumner for starts.

Scott Sumner

Feb 19 2019 at 1:27am

Jerry, You said:

“This is not an issue about ‘seigniorage’ as most people understand that term,”

I think that’s the problem. If MMTers cannot speak in a language that brilliant economists like Paul Krugman and Nick Rowe understand, then it’s pretty unlikely that they’ll ever be able to influence Fed policy. Say what you will about market monetarism, we don’t create our own private language.

So let me get this right. You “pay for” spending by creating money, and you create money by spending. Sounds nice!

Jerry Brown

Feb 19 2019 at 3:13am

“So let me get this right. You “pay for” spending by creating money, and you create money by spending. Sounds nice!”

No Scott- I pay for spending by using US Dollars. And my spending doesn’t create more US Dollars. I am not the US Congress. MMT would say the US government creates money when it spends.

Perhaps my understanding of what the ordinary understanding of what seigniorage means is off- I always thought it mostly was a historical reference to when kings might set a higher value to a coin than the market value of the physical substance of what the coin was made of. In any event, I have read a lot from MMT economists and they don’t often use the term ‘seigniorage’, but they do speak a language that even brilliant economists probably can understand- at least if they understand English and read about it.

And while I think NGDPLT is a good idea, the very name NGDPLT kind of points to some kind of specialized language don’t you think?

Matthias Goergens

Feb 19 2019 at 10:20am

Nominal GDP level targeting is a specialised term by the standards of the general public. But it is a phrase entirely understandable within orthodox economics.

Scott Sumner

Feb 19 2019 at 1:25pm

Jerry, I should have been clearer. In my sarcastic remark I meant “US government” when I said “you.” But my problem is still there. In what sense does the US government create money when it spends? Why is the government different from a state government, for instance? Does it also create money when it spends? How about a corporation? And even if it does create money in some odd sense of the term, in what sense can that money creation be said to pay for the spending?

The term “seignorage” simply refers to the revenue earned from money creation. It’s a standard term in economics. If MMTers mean something else by the revenue from money creation, they need to explain what that something else is.

As I read your comment, you seemed to be saying that Krugman and Rowe had completely misunderstood what MMTers meant by the revenue from money creation.

Jerry Brown

Feb 19 2019 at 4:03pm

Scott, I am going to try to answer these questions based on MY understanding of what MMT says. So I will be more or less ‘reporting’ about the ideas to the extent that I can. (It would be far better, but more time consuming, to read what the MMT economists themselves have written.) These answers pertain to a currency issuing government (such as the US federal government) that issues a fiat currency that is not pegged to any other currency or commodity.

“Why is the [federal US] government different from a state government, for instance?” Because state governments do not issue the US Dollar and are users of the currency somewhat similar to ordinary households and corporations. State governments do not create money when they spend- they must obtain US Dollars first in order to finance their spending.

“How about a corporation?” Most corporations do not create money. But MMT holds that commercial banks do create a form of money through their lending operations in the form of bank deposits. We use this form of money almost interchangeably with the US Dollars issued by the federal government. Except to pay federal taxes- you can pay with a bank check but your bank has to transfer US government created Dollars (usually in the form of reserves at the Fed) to the government to actually satisfy the tax obligation.

“In what sense does the US government create money when it spends?” and “in what sense can that money creation be said to pay for the spending?” Well this is truly the ‘money’ question and it is both simple and complex. The simple answer is, in the US, Congress is authorized in the Constitution to establish a currency and impose taxes in that currency and spend in that currency. Which they have obviously done. So in MMT ideas, the order of this goes 1.create a currency 2. impose a tax payable in that currency (create a demand for that currency amongst your citizens because they need it or they go to jail) 3. spend some of that currency into existence in exchange for services or goods from your citizens (so that they will be able to actually pay the tax and not go to jail).

So now the federal government has created money by spending its currency. And it doesn’t need its currency back from the citizens in order to spend. It can just destroy the paper notes that come back to it as payment of taxes. It might pretend to need them and make laws that constrain its spending, but the government really can and does just create more everytime it spends. What the government needs is for the people to want the currency and to be willing to exchange things for it. Government is not Mr. Nice Guy in MMT. It imposes taxes and penalties to create a demand for its currency so that we will be willing to give up our time, or labor, or property to the government so that it can provision itself as (hopefully) we think appropriate.

So (maybe) MMT would consider that the entirety of federal government spending could be understood as ‘seigniorage’. Except for the minimal real costs of printing the cash, or the even smaller real costs of creating money through computer keystrokes into accounts. But that is just my own supposition. Like I said, I don’t recall MMT economists actually using the term ‘seigniorage’ very often if at all.

Scott Sumner

Feb 19 2019 at 6:13pm

Jerry, You said:

“State governments do not create money when they spend- they must obtain US Dollars first in order to finance their spending.”

But the federal government also does not create money when it spends, at least most of the time. The small amount of spending financed by seignorage is trivial.

As far as bank money, when you pay for something with a check you are not paying for it by “creating money”, you are buying it on credit and the loan is repaid when the check clears. At that point you deliver base money to the seller.

You said:

“So now the federal government has created money by spending its currency.”

That’s what I said in the post, but the amount of spending paid for by newly created money is trivial.

As for your final comment that perhaps all spending could be financed out of seignorage; that’s impossible for the reasons provided by Krugman, Rowe and me. Most spending must be paid for by taxes or debt. And debt means future tax liabilities. Paying for the bulk of it by money creation is sheer fantasy.

And finally, regarding your suggestion that I read MMT papers—I’ve done so. The problem is that the writing style is so confusing that it’s hard to make heads or tails of what they are saying.

Jerry Brown

Feb 19 2019 at 9:55pm

Like I said- I am reporting what my understanding of MMT is based on my reading of it and discussions I have listened to or attended. I have read a lot about it and I think MMT makes some very good arguments. And I think it is worthwhile to try to understand what they are saying. And that the best way to do that would be to read what the MMT economists have to say themselves rather than my interpretations of it- there is no doubt that I will screw up somewhere in my interpretation. And it is not all that difficult to understand what they say if you are willing to try to. That doesn’t mean you need to agree with it. But I do mostly.

But anyhow.

“But the federal government also does not create money when it spends, at least most of the time.” I refer you to the first sentence of my first comment-” MMT says that ANY time the currency issuing government spends it is creating money. ”

“The small amount of spending financed by seignorage is trivial.” If you accept my assertion that MMT actually says that ANY time the currency issuing government spends it is creating money then it seems to me that MMT says either that there is no seigniorage or that it is all seigniorage when that government spends. MMT rarely, if ever, uses the term seigniorage to my knowledge..

“As far as bank money, when you pay for something with a check you are not paying for it by “creating money””. Yes you are. You are creating something that either fulfils or promises to fulfil all the definitions of money that we use. It is just usually not as secure as the government’s money and therefore not as widely accepted. It is also usually much more temporary in that it is ‘destroyed’ when presented to the bank it is written through.

“Most spending must be paid for by taxes or debt. And debt means future tax liabilities. Paying for the bulk of it by money creation is sheer fantasy.” That is the current state of the law in the US so I’m sure MMT recognizes the institutional realities in place. But as a matter of theory, MMT holds that the difference between tax receipts and government spending is going to have different effects depending on the state of the economy at that time in question- as in how much unemployment is there. And MMT holds more or less (more really) that government deficit spending that is “financed” by bonds, the way it is currently done, is not significantly different in its macroeconomic effects (not less inflationary) than that same government spending would be if the government just spent without creating the bonds and selling them.

Scott Sumner

Feb 20 2019 at 12:08pm

Jerry, You said:

“MMT says that ANY time the currency issuing government spends it is creating money.”

Saying something that is clearly false doesn’t make it true. At a minimum, you’d need to explain why they believe this to be true. You say that it’s easy to understand their ideas if you take the time to read therm. I’ve done that. I also wonder why you are incapable of clearly explaining their ideas, if you believe they are so clear. You haven’t told me why governments create money when they spend it.

You said:

“”As far as bank money, when you pay for something with a check you are not paying for it by “creating money””. Yes you are. You are creating something that either fulfils or promises to fulfil all the definitions of money that we use.”

This is clearly wrong, at least according to the definition of money used by economists. You are free to make up definitions all day long, but don’t expect anyone to pay attention. I can assert that stocks are actually bonds, or that houses are actually peaches, but I wouldn’t expect anyone to believe me.

Next time you see a Rolls Royce you want to buy, try “creating the money” to finance it by writing a big check.

When you write a check you are transferring money from your bank account to the seller. You are not creating new money–you are spending existing money.

You said:

“And MMT holds more or less (more really) that government deficit spending that is “financed” by bonds, the way it is currently done, is not significantly different in its macroeconomic effects (not less inflationary) than that same government spending would be if the government just spent without creating the bonds and selling them.”

This is completely false; money financed spending is vastly more inflationary than debt financed spending. It explains why Argentina had hyperinflation in the 1980s and we did not. Both places had big deficits.

Jerry Brown

Feb 22 2019 at 12:35am

You know Scott, I really thought you might be interested in learning what the MMT economists say regardless of whether you agree with them or not. If only so you could be accurate when you write about what they say. “MMT says that ANY time the currency issuing government spends it is creating money” is a reasonable one sentence summary of what they say happens when the federal government spends. At least one MMT economist, Bill Mitchell, says deficit spending with bond issuance, given the institutional arrangements in place, is not less inflationary than deficit spending without bonds.

What is a check that you use to pay for something? I think it is reasonable to consider that it is a promise (contract) to have your agent (bank) pay what you owe when it is presented to them. In that sense a check is a short term debt obligation that you made. It is an I.O.U. until that time the bank pays up. So until that time it is a form of money that you created when you handed it to someone in exchange for goods or services. You go to a grocery store and pay with a check you walk out with your groceries. Walk out without paying you might get arrested. The check is a type of money. I’m guessing that a lot of Rolls Royces have been purchased with checks over the years. Probably a lot more than with cash. Never bought one myself.

Rajat

Feb 19 2019 at 5:35am

I understand MMT consistently with the way Jerry explains it. That is, it’s fundamentally about (i) ensuring full employment with fiscal policy as the key instrument rather than monetary policy and (ii) securing a desired allocation of resources or consumption, rather than seignorage-based free lunches. In this way, it makes sense as a reaction to people who say things like “we can’t afford X”. Well, perhaps the US can’t give each of its citizens a 400 foot yacht, but it can provide healthcare and housing to all. Doing so would rapidly come up against resource constraints, so fiscal policy (taxation) would be used to keep inflation in check and help effect the desired reallocation of resources from workers to patients and the homeless. It’s a particularly seductive message when inflation in the US and elsewhere remains seemingly entrenched at low levels, creating the impression that a lot more stuff could be had for free.

Scott Sumner

Feb 19 2019 at 1:26pm

Rajat, That mixes up several ideas:

The idea that we can pay for things by “creating money”

The idea that we can pay for things by borrowing more.

The idea that we currently need more demand stimulus in the US.

Lots of conventional economists believe the third claim, which doesn’t really distinguish MMT from any other theory. As far as the question of how to pay for the fiscal stimulus, you can use borrowing or money creation. If it’s borrowing, that’s simply standard Keynesian theory. So what exactly is the point? Keynesians like Krugman object to the claim that all this can be paid for by creating money; that’s how he read their essays and that’s how I read them too. If MMTers don’t actually mean “creating new money” when they say “creating new money” then what exactly are they saying?

James

Feb 19 2019 at 8:26am

The hot potato analogy does not make much sense.

If people and organizations really don’t want to hold high powered money, they can avoid receiving it to begin with. No one has to take the other side of the trade when the Fed engages in open market operations. And yet we see large profit seeking organizations existing as primary dealers.

Matthias Goergens

Feb 19 2019 at 10:25am

Yes, because there’s wealth to be made.

Don’t mix up a dollar as cash (or reserves) with a dollar as a unit of account. Everybody wants to increase their net worth as measured in the latter. But they don’t necessarily want to hold it all as the former.

So those profit seeking enterprises do indeed seek a profit when they play the counterparty to the central bank. But then they can go and invest the proceeds elsewhere instead of just sitting on cash.

Somehow this all seems clearer when you don’t think of central banks being the norm, but in terms of how it would work with competing private issuers of money. (And then as a second step think about how government monopoly money distorts the whole thing somewhat.)

Scott Sumner

Feb 19 2019 at 1:29pm

James, If someone offers me $2 million in cash for my house, I’d sell it in a heartbeat. But that’s not because I want to hold $2 million is cash as an asset, I’d try to immediately get rid of it by buying something else, like stocks or bonds.

This is especially true when bank reserves pay zero interest and other safe assets like T-bills pay positive interest rates.

James

Feb 23 2019 at 11:32pm

Scott,

Your example of the Fed buying your house is either irrelevant to actual central banks or damning.

If the Fed is just buying coupon paying assets at prices equal to the NPV of forward cash flows, then there is no reason why primary dealers would willingly sell financial assets to the Fed for cash only to turn around and use that cash to buy other financial assets. At least in a world with transactions costs.

If the Fed is buying financial assets for more than the NPV of forward cash flows, then open market activities are actually a form of fiscal policy; basically a transfer payment to primary dealers.

Benjamin Cole

Feb 19 2019 at 10:27am

Interestingly, George Selgin responded to one of my comments on MMT by saying that he, Selgin, had proposed money finance fiscal programs for Japan.

Thus Selgin joins Ben Bernanke in occasionally advocating money financed fiscal programs as a form of aggregate demand stimulus.

I think the MMT crowd is a little off base, although that should be said within the context that no one in macroeconomics is ever wrong.

The sensible use of money financed fiscal programs would surely be a better way to proceed then running up more and more national debt.

A fascinating intellectual exercise would be to ponder an economy where new money is created through money financed fiscal programs but the commercial bank system cannot endogenously create new money.

The Original CC

Feb 19 2019 at 12:32pm

Yeah, the seigniorage criticism of MMT is way off. I don’t know if MMT is correct or not, but they are certainly not claiming that spending should be done through seigniorage.

Comments are closed.