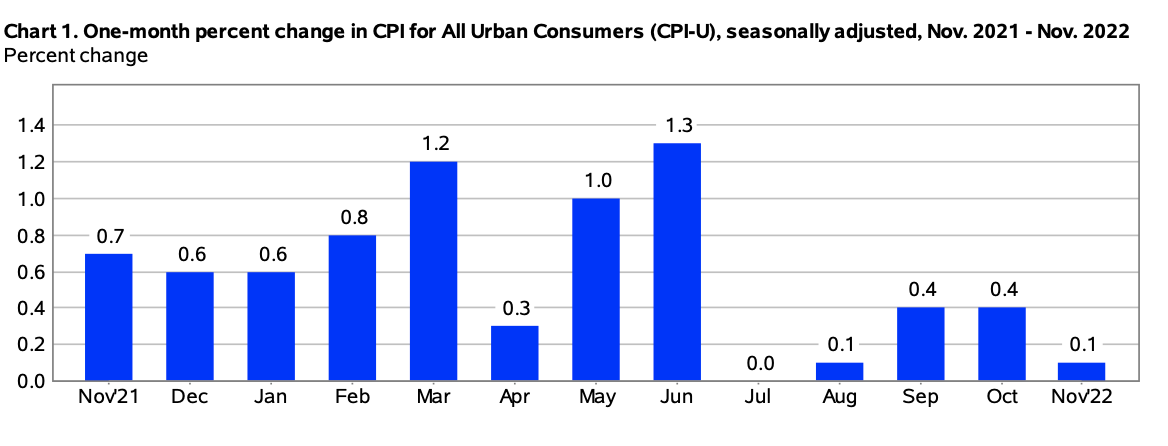

The Bureau of Labor Statistics report on inflation that came out today shows that in November, the CPI (not inflation) rose by 0.1 percent in November. That means that in the 5 months from June to November, the CPI has risen by 0.0 percent (July) + 0.1 percent (August) + 0.4 percent (September) + 0.4 percent (October) + 0.1 percent (November) for a total of 1.0 percent. Although one should ideally compound these numbers, they are so low that compounding would make little difference. That means that the annualized rate of inflation for the last 5 months is approximately 2.4 percent.

Over those same months, the CPI minus food and energy (the core CPI) rose by 0.3 percent (July) + 0.6 percent (August) + 0.6 percent (September) + 0.3 percent (October) + 0.2 percent (November) for a total of 2.0 percent. Failure to compound is a little more serious here because of the large numbers in August and September, but still not a big mistake. That means that the annualized rate of core inflation for the last 5 months is approximately 4.8 percent.

I posted about the inflation rate in November after the October data had been released.

READER COMMENTS

Andrew_FL

Dec 13 2022 at 3:15pm

CPI since June is almost exactly on track for a 2.4% annualized rate & CPI has average .4% higher than PCE over the last 10 years, so the last six months (Jun-Nov) is consistent with the Fed being back on a 2% rate target

But if CPI continues on a 2.4% annualized trajectory going forward that will be a permanent 7.9% level increase compared to if it increased 2.4% from February 2020 indefinitely. CPI was already caught up to 2.4% annualized in April of 2021.

“Flexible [read Asymmetric] Average Inflation Targeting” means random upward shifts of the price level can be expected from now on. Not good.

Scott Sumner

Dec 13 2022 at 5:05pm

My view is that just as the high point of inflation in the summer was partly driven by one-time special factors, so is the slowdown in recent months. Thus there’s still much work to be done to get the trend rate back to 2%.

David Henderson

Dec 14 2022 at 9:52am

True. Moreover, velocity is still well below pre-Covid and pre-lockdown level. If it goes up much, inflation could go higher.

robc

Dec 14 2022 at 12:23pm

Serious question…trend rate starting from when? It obviously matters a lot.

Is the starting point 1933 or 1971? Those would both seem reasonable. Or some later point when the Fed claimed to be targeting inflation? But I didnt believe them, so starting now?

Same applies to a NGDP trend line…where do we start it?

Comments are closed.