No, this headline does not reflect any ill will toward the Chinese economy, rather I am celebrating a rare victory in the war on moral hazard.

In the US, the problem of moral hazard seems to be growing worse over time. It began with FDIC insured bank deposits. Then the doctrine of “too-big-to-fail “was added. Then Fannie Mae and Freddie Mac were implicitly backed. Later, their backing was made explicit. Now there’s talk of bailing out student borrowers, and pension fund bailouts may be coming down the road. Federal flood insurance encourages construction in flood prone areas.

I have frequently argued that moral hazard plays a big role in modern financial crises, but it’s hard to get other economists interested in the problem. Most seem to treat it like a minor concern.

Therefore it’s nice to see a major economy taking important steps against moral hazard:

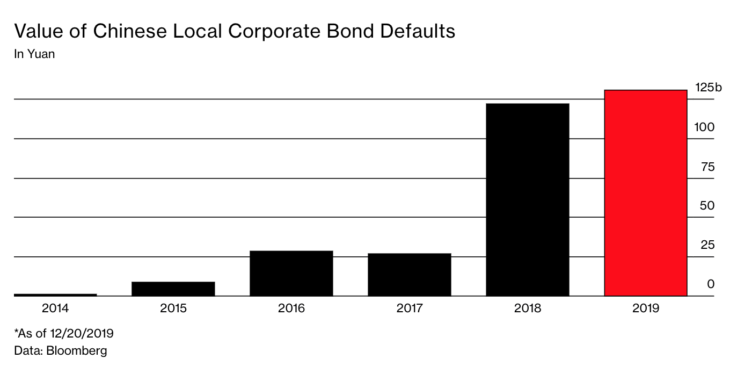

China’s had another record year of corporate bond defaults. That’s not a crisis. It’s a plan.

A decade ago, defaults almost never happened, but that wasn’t because companies in China were always healthy. It was a reflection of the tightly controlled financial system, where companies were often linked to the government and bonds were largely bought by state-owned lenders. Authorities have often stepped in to ensure that financially troubled enterprises didn’t crash into default, out of concern over social unrest in the event of job losses or missed payroll payments.

This system imposed little discipline on borrowers. Now global investors are coming into China’s bond market. Though many companies are still state-backed, policymakers are getting more comfortable with defaults. Without them, bond buyers would have little incentive to make a careful assessment of a company’s creditworthiness.

Government guarantees of debt obligations lead to inefficient investment decisions. In China, this has shown up in the construction of numerous “ghost cities”, such as the Binhai area of Tianjin. I visited this area in August, and snapped a picture of a forest of empty skyscrapers:

If the Chinese government is serious about allowing debt defaults, it will reduce the incentive of investors to misallocate resources. This should make China’s economy more productive.

READER COMMENTS

Alan Goldhammer

Dec 27 2019 at 8:26am

Scott, you write about upcoming pension fund bailouts in the US. The just passed spending bill bailed out the coal miner’s pension fund. That one is suffering because of the ongoing bankruptcies of coal companies and the spinning off of the pension fund liabilities into separate LLCs. There was a recent NY Times article on this bail out that discussed the possibility of future bail outs. Interestingly, the article notes that President Trump is part of a multi-employer plan from his days on his reality television program.

Philo

Dec 27 2019 at 10:32am

Why “interestingly”?

Thaomas

Dec 28 2019 at 6:59am

The Bush-Obama administration made a big mistake in bailing out the owners of over-leveraged financial firms in 2008-9. But given the Fed’s disastrous inaction/passivity, they were in a bind.

Alan Goldhammer

Dec 28 2019 at 9:55am

What was the alternative? Should we have jumped off a financial cliff hoping the parachute would open for a gentle landing?

I have read this kind of statement a lot both back in 2008 and in retrospective articles and posts. Nobody has come up with any reasonable (and realistic) suggestion of what would have transpired had the bail out not taken place. For those of us managing equity investments at the time it was pretty scary.

Scott Sumner

Dec 28 2019 at 12:05pm

Monetary stimulus would have been a more effective policy in 2008.

Michael Pettengill

Dec 31 2019 at 3:03pm

Wasn’t the Fed buying bonds of the uninnsured shadow bank depository institutions (ie, retail money funds) “monetary stimulus”?

I remember the claims made back in the early 70s that money funds would never use worker savings to make bad loans so they would be far safer for worker savings than FDIC banks while paying much higher interest to workers because they no longer bear the fees and regulatory burdens.

Implicit was money funds would be so safe they would never experience bank runs because workers feared they would not get their deposits back.

And wasn’t the Fed buying bonds from the shadow bank lenders like GE Capital and GMAC, which got the money to lend from money funds that got the money from workers and businesses depositing their savings and working capital in shadow bank depository institutions, “monetary stimulus”?

I remember the news of Primary Reserve Fund getting approval to offer restricted “demand deposits” to workers like me, no longer restricted to the certified rich. Thus I was not surprised that it was the first to experience a bank run, fail, and seek a Federal government bailout of wealth redistribution by bankruptcy judge. I wish Louis Rukeyser had lived a bit longer to bookend his discussion on money market fund vs FDIC savings; W$W was where I learned the most about banking and finance.

TMC

Dec 28 2019 at 6:19pm

Agreed Alan, it’s not like TARP lost money. The firms just needed some liquidity. I’m not a fan of bailouts, but this a lot of companies at once and no one know the consequences.

Scott, that’s what bothers me about Bernanke. He was a student of the great depression, but it seems we just repeated the same mistakes.

Robert EV

Dec 29 2019 at 1:46pm

This sounds like an argument in favor of golden parachutes for incompetent managers given that Thaomas was critiquing the bailing out of owners of over-leveraged firms.

Would it not have been more fiscally prudent to give that bail-out money to people who were demonstrating better money management skills? Heck, some of those previously mentioned owners would have probably owned stock in better managed firms as well, and would have benefited even more by having the funds channeled to these better managers.

Michael Pettengill

Dec 31 2019 at 3:26pm

If you were a depositor in a money market fund like Primary Reserve Fund, you wanted to lose your money because you deserved to be punished by enabling over leverage?

The 70s opened up “capitalism” to the “workers” like me, and I followed this debate, and how capitalists risked everything, thus getting big rewards. Ok, so in 2008, workers should have lost big, ie lost their savings in money funds, as well as the thousands of businesses who had their payrolls in money funds. After all, the best way to drive growth is to take money from workers who merely use the money to buy stuff….

Until the Fed starts hiring workers to build capital assets like roads, water and sewer, teach people, build factories, etc, the Fed stimulating the economy involves lending to people who gamble with other people’s money for personal profit, without taking much risk themselves. Just like the “Fed” of the shadow banking system in the investment banks like Lehman, et al. which created trillions from nothing, that vanished in 2008.

Dan

Jan 3 2020 at 1:26pm

Alan,

I agree with your second paragraph, though not your conclusions. We were told repeatedly how something needed to be done or it would be the end of the world. However, that doesn’t mean your conclusion follows. Doing nothing would have negatively impacted many people in the financial sector and probably would have had some spill over effects on the real economy. However, it would make it less likely that a recurrence would occur.

Comments are closed.