Germany’s large manufacturing sector has done poorly during 2019. As a result, many are calling for fiscal stimulus:

Germany is the economic engine of Europe — and it’s running on fumes. After a decade of near-constant expansion, the economy is flirting with recession. Germany’s export-dependent companies are deeply exposed to fallout from rumbling trade disputes, and the critical auto industry is struggling with the shift to electric cars. That means pressure is rising on the government to abandon its longstanding aversion to splashing the cash. Will Chancellor Angela Merkel loosen the purse strings to give the economy a shot in the arm — and would it be enough?

Germany should resist the calls for fiscal stimulus. Instead, it should call on the ECB to adopt a more expansionary monetary policy. But even if the ECB continues to undershoot their inflation target, fiscal stimulus is unwise and unnecessary.

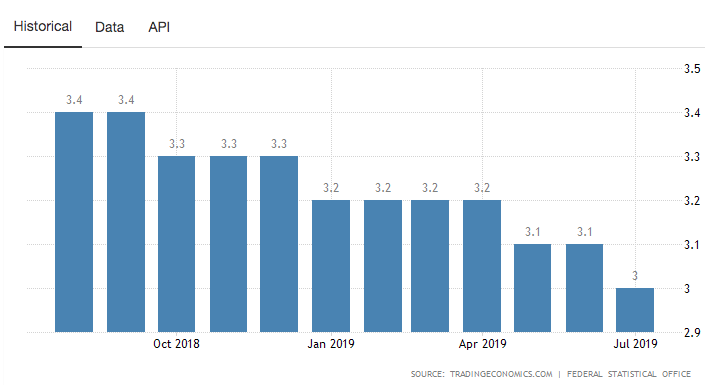

The recent slump in German manufacturing is a real shock, partly fallout from the US/China trade war. Real shocks tend to be much less harmful than nominal shocks, especially for large diversified economies. Thus even though German manufacturing has recently been weak, the German labor market continues to be quite strong. Here’s the unemployment rate in Germany over the past 12 months:

The goal of macroeconomic policy is not to prevent all fluctuations in real output, rather the goal is to prevent fluctuations caused by the interaction of sticky wages and unstable nominal GDP. It is possible that Germany will eventually face a nominal shock, but as of today there is no need for stimulus in Germany.

READER COMMENTS

John Hall

Sep 19 2019 at 1:41pm

There has been a slowdown in the pace of NGDP growth to 2.4% YoY in Q2 after peaking at 4.8% in Q4 2017 recently. The recent low of 2.4% growth in Q2 2019 (also in Q3 2018) represent the slowest pace since early 2013.

For the sake of argument, let’s suppose that there WAS a nominal shock but the ECB doesn’t do enough to offset it. Should the German government engage in fiscal stimulus? What if the same thing happened to a smaller Euro area country, like Czech Republic?

Benjamin Cole

Sep 19 2019 at 7:29pm

Interesting post.

German representatives, of course, have been calling on the ECB to tighten.

The one-size-fits-all monetary policy of the ECB does raise a question. If the ECB policy is too tight for nations such as Greece or Italy, should those nations engage in direct quantitative-easing, aka helicopter drops?

My understanding is that the EC has rules pertaining to the maximum size of fiscal deficits that an Italy or Greece can have. Most likely these rules also pertain to helicopter drops, that is money-financed fiscal programs.

But I guess if a Greece or Italy prints up Euros that would be considered counterfeiting.

Why any nation would give up the sovereign power of printing money is beyond me.

Thaomas

Sep 22 2019 at 8:23am

A one size fits all monetary policy (even if it were a region-wide NGDP trend target) could be problematic for different not incompatible reasons. a) Countries differ in the stickiness of their prices (or whatever causes the optimal rate of inflation to differ from zero) so at any given time some countries will have sub-optimal inflation and unemployment while other have super-optimal inflation. [This partially explains why Ireland left the PIGS sooner than Spain and Greece has not left at all.] b) Countries could have suffered differential supply shocks (such as a one-time investment flow resulting from a one time foreign investor confusion of the removal of cross border exchange risk with the removal of — or arguably enhancement of — country risk. Of course if the one size is subverted to be the size that fits one particular country, that is an additional problem.

Scott Sumner

Sep 19 2019 at 11:53pm

John, Just to be clear, the ECB will do monetary stimulus if the Germans want it to.

But if we consider your hypothetical, the answer may depend on whether you are thinking in terms of what’s best for Germany or what’s best for the eurozone. If there is “monetary offset”, then any stimulus in one country leads to contraction in another.

In smaller open economies, fiscal stimulus probably doesn’t have much effect.

Matthias Görgens

Sep 20 2019 at 2:43am

Playing devil’s advocate, increasing government spending during times of economic slump might make sense for supply side reasons: the government can get some infrastructure projects for cheaper than otherwise.

But that’s not fiscal stimulus.

Scott Sumner

Sep 20 2019 at 2:48pm

If unemployment is 3%? They can certainly borrow money more cheaply, but it’s not obvious that money should be invested in new infrastructure.

P Burgos

Sep 25 2019 at 10:48pm

I thought that Germany’s ports and freight rail were aging and genuinely in need of repair/modernization in order to keep logistics competitive in Germany. And that is part of why China wants to invest in making Trieste a major port again as part of the BRI; Hamburg’s port is becoming outdated and is further away from China’s major shipping lanes.

Thaomas

Sep 22 2019 at 8:03am

If a government followed a net present value rule — which would result in greater investment when market prices of some factor of production are greater than their marginal cost (unemployment) and the borrowing cost/discount rate for the economic life of the project had decreased — government spending would sure “look” like a “fiscal stimulus.”

TMC

Sep 20 2019 at 9:37am

“.. partly fallout from the US/China trade war. ”

Wouldn’t Germany pick up business as a result of the trade war? This should offset the slowness.

Scott Sumner

Sep 20 2019 at 2:49pm

Trade wars are not zero sum games. They slow global investment, which hurts Germany’s capital goods producers.

Thaomas

Sep 22 2019 at 7:57am

How is a fall in exports resulting from a fall in external demand a supply shock. If a fall in export orders is not a demand shock, what is? What about a fall in demand for investment goods because of some new concern about future real growth (say a trade war)?

Thaomas

Sep 22 2019 at 8:30am

I thought the goal of macroeconomic policy at least in the US was to maximize f(real income, price level trend) social welfare function.

Comments are closed.