In general, policies that bring down inflation tend to impose pain on the labor market. That was certainly the case back in the early 1980s, when Paul Volcker’s anti-inflation policy reduced inflation from over 10% to 4%, while pushing unemployment up to a peak of 10.8% in late 1982.

Larry Summers has argued that the current anti-inflation program, while necessary, will also impose substantial pain on the labor markets. This claim seems reasonable, but needs a few qualifiers:

1. The labor market is much tighter than in the early 1980s. One obvious indicator is unemployment, which current stands at 3.5%. Back before the 1981-82 recession, the unemployment rate was about 7.5%. That’s partly because the so-called natural rate of unemployment back then was higher than today, but that’s not the only reason. There really is a much greater worker shortage today than back in early 1981.

2. Nominal wage growth today has far less momentum than back in the early 1980s. Today brought further good news on the wage front:

The employment cost index, a barometer the Federal Reserve watches closely for inflation signs, increased 1% in the October-to-December period, the Labor Department reported Tuesday. That was a bit below the 1.1% Dow Jones estimate and less the 1.2% reading in the third quarter. It also was the lowest quarterly gain in a year.

That figure (4% annualized) is consistent with roughly 3% trend inflation. In contrast, nominal wage growth in the early 1980s was extremely rapid—peaking at roughly 9%. The Fed faced a far greater challenge in the early 1980s than today. They need to do much less wage disinflation, and they start from a stronger labor market.

You might wonder how wage and price inflation back in the early 1980s could have been so much worse, while the today the labor market is far more overheated. Isn’t high inflation caused by excessive real economic growth, as in the Phillips Curve model?

In fact, the Keynesian Phillips curve model is simply wrong. It’s not wrong because there is no relationship between inflation and unemployment. A sharp fall in both wage and price inflation tends to be associated with a temporary rise in unemployment. Rather the Phillips Curve model is wrong because Keynesians get causality reversed. They assume that causation goes from economic overheating to wage and price inflation, whereas the opposite is more nearly true. To be precise, it is unexpected increases in nominal growth in spending that cause both rising inflation and falling unemployment.

Milton Friedman had the correct interpretation of the Phillips Curve. He saw that the high inflation of the early 1980s was not caused by an overheating economy; it was caused by monetary policy. Rapid money growth drove NGDP and wage and price inflation much higher. Because wages and some prices are sticky in the short run, not all of them immediately adjust upward to their new equilibrium. Thus you also get a temporary period of falling unemployment when monetary policy boosts nominal spending. Unexpectedly high (demand side) inflation reduces unemployment for a few years.

Once the public adjusts its expectations to the high trend inflation, the economy returns to the natural rate. This explains why the economy today is more overheated than before the Volcker disinflation. By the early 1980s, the public had adjusted to a long period of high inflation and unemployment had returned close to its natural rate. Each year, both wages and prices rose rapidly—but the economy was not in “disequilibrium”. In contrast, today’s economy has still not adjusted to the very fast NGDP growth of 2022. Thus the labor market is more overheated than in early 1981, despite much less inflation. The labor market is in disequilibrium.

Today’s wage report is good news, as it suggests that Powell doesn’t need to do nearly as much nominal wage disinflation as Volcker had to do. He needs to get that wage index down from 4% annual growth to 3%. Fortunately, today’s workers are not used to getting 9% raises every year, and probably view the big wage increases of last summer as unusual. I still believe that some pain will be imposed on the labor market in bringing inflation down, but perhaps something closer to 4% or 5% unemployment, not the double-digit unemployment of late 1982. It may not be a soft landing, but relative to 1982 it will probably be a softish landing.

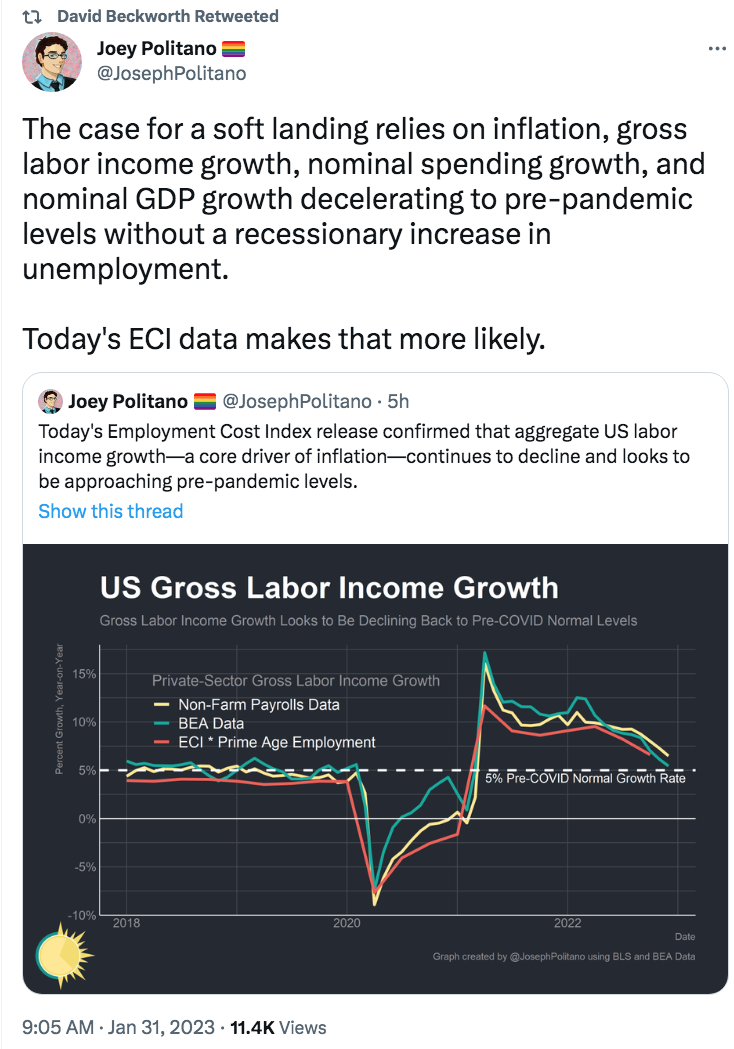

PS. After writing this post, I noticed that Joey Politano has a similar take:

READER COMMENTS

Loquitur Veritatem

Jan 31 2023 at 5:48pm

Taking 2000 as the base case and adjusting for changes in the labor-force-participation rate and the employment/population ratio, the “real” unemployment rate in 2000 was 4%. In the early 1980s it ranged from 11% to 15%. Now, it’s about 11%. The current labor market is nowhere near “tight”. It’s about as “loose” as it was when Volcker cranked up the interest rate.

Scott Sumner

Jan 31 2023 at 7:21pm

No, the real unemployment rate is 3.5%. Companies are simply unable to find workers for available jobs. It was very different in 1981.

I’ve never seen such bad service in my entire life.

vince

Jan 31 2023 at 10:55pm

“I’ve never seen such bad service in my entire life.”

There’s a great topic for a future article, and how it fits in with inflation measurement.

Scott Sumner

Feb 1 2023 at 1:57pm

I could add that at the peak of the 2019 boom, there were 7 million job openings. Today there are 11 million. “Overheated” doesn’t even begin to describe this economy.

Dawid

Feb 1 2023 at 7:01am

“That’s partly because the so-called natural rate of unemployment back then was higher than today, but that’s not the only reason.”Why is that?

Spencer

Feb 2 2023 at 10:53am

Volcker turned 38,000 nonbanks, the CUs, MSBs, and S&Ls into banks. The FDIC raised deposit insurance from 40,000 to 100,000. That destroyed money velocity (as predicted).

JP is the worst Chairman ever. We will have a permanent inverted yield curve accompanied by stagflation.

Spencer

Feb 2 2023 at 11:09am

Banks aren’t intermediaries as George Selgin and JP say. Banks don’t lend deposits. Deposits are the result of lending/investing. As an increasing volume and proportion of bank deposits were saved, secular stagnation grew. Secular stagnation is none other than a deceleration in the velocity of circulation.

The FED’s solution to secular stagnation was an increase in FED credit (as best exemplified by Japan’s economy). The FED is operating the economic engine in reverse.

Comments are closed.