The title of this post is the shortest description I could come up with for the global economy circa 2019. Because these two concepts get confused, a short explanation is in order.

The best way to judge the stance of monetary policy is by looking at the growth rate in “M*V” aka nominal GDP. By that criterion, money has been tighter than average in America, and even more so in Europe and Japan. That helps to explain low nominal interest rates, but it’s not the whole story.

It’s less clear how we should measure credit market tightness. I’d like to suggest looking at the difference between NGDP growth expectations and nominal interest rates.

Unfortunately, we don’t have a precise measure of NGDP growth expectations, but recent trends in many countries show NGDP growing at rates much higher than the current level of risk-free interest rates. Normally you’d expect those two rates to be closer together. Thus credit is currently relatively easy by historical standards. (Of course the low interest rates might be a prediction of recession, but they’ve persisted for quite some time.)

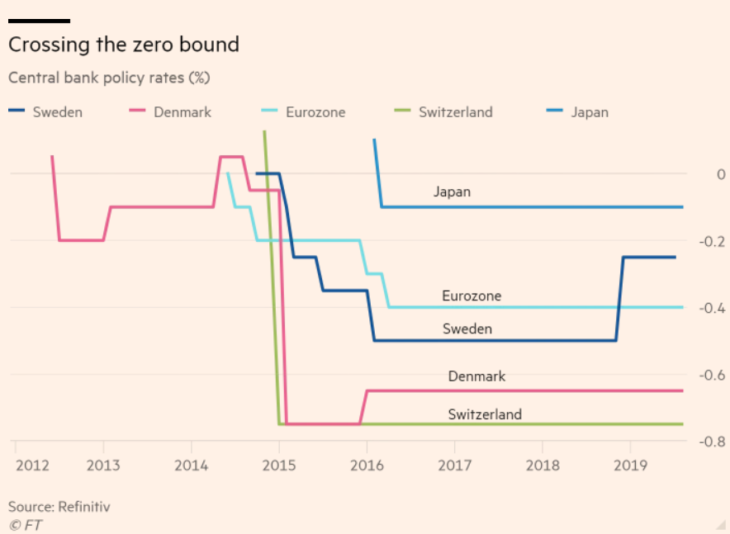

One of the best examples of easy credit is Sweden, where NGDP growth has averaged close to 5% since 2014 (high by European standards), but interest rates have been negative since 2015. The FT has an article discussing Sweden’s situation. They point out that Sweden’s monetary policy has achieved good results. With inflation close to 2% and unemployment is low by historical standards, Sweden has done better than the eurozone. The Swedish krona has been weak. Housing has been especially strong.

Nonetheless, there is a lot of frustration with Sweden’s low interest rate policy, with some calling for the abandonment of the 2% inflation rate target. While inflation targeting is not optimal, many of these critics are confused. They seem to believe that Sweden has ultra low rates because of an easy money policy aimed at 2% inflation, and that a tighter policy would lead to higher interest rates. Actually, the long run effect of tighter money is lower nominal interest rates.

It’s easy to understand the frustration. I certainly would not have expected 5% NGDP growth to lead to such low interest rates. We live in an easy credit world for reasons that I don’t fully understand, although it’s obviously some combination of high saving and low investment. Can’t we just look at the numbers? No, actual realized saving equals investment. There have been shifts in the saving and investment schedules that, taken together, have led to much lower interest rates without much change in the quantity of saving and investment.

Given the strength of the Swedish housing market, I’d guess it’s a combination of low non-residential investment demand and a higher propensity to save, but a lot more research needs to be done in this area.

Don’t draw the wrong policy implications from easy credit. If it is a “problem” (I’m not sure it is), it can’t be solved with monetary policy. Governments could think about removing regulatory barriers to investment in housing, infrastructure and other useful activities. If NGDP is growing at 5%, why can’t entrepreneurs find more useful things to do with money borrowed at near zero percent? What’s changed from earlier decades?

In Denmark, mortgage rates are minus 0.5%. Someone in Copenhagen could take out a $1,000,000 (equivalent) mortgage, put the cash in a safe in their basement, and earn a $5000/year risk free profit. That seems crazy. So don’t get me wrong, I see why people instinctively feel there is something wrong here. It’s just that the “something wrong” in places like Sweden and Denmark doesn’t happen to be monetary policy.

PS. This is not a new issue. In 2012, I did a blog post entitled “Tight money, easy credit”.

PPS. Yes, I understand that fire and theft risk would prevent the Danish arbitrage I describe, but it still highlights the craziness of the situation.

READER COMMENTS

Benjamin Cole

Aug 14 2019 at 7:52pm

I enjoyed this post.

Are total debt to GDP levels rising in Denmark and Sweden?

It seems to me this issue, that is rising debt-to-GDP, needs to be addressed somehow.

Given current monetary and fiscal policies, and the ban on money-financed fiscal programs, and the endogenous creation of money through the commercial banking system, can Western developed nations stimulate economies without rising debt-to-GDP levels?

As widely noted, debt-to-GDP levels ballooning throughout the Western world and also in mainland China. China may have an escape hatch. The People’s Bank of China evidently has the option of printing money and buying back bad loans from their commercial banking system. This deeverages the economy somewhat and also maintains their commercial banking system solvency.

Japan may have also essentially declared a debt Jubilee. One may wonder if the Bank of Japan will ever sell its vast horde of Japanese government bonds, now equal to more than 100% of Japanese GDP. I doubt it.

Benjamin Cole

Aug 14 2019 at 8:03pm

I forgot to include this question: Are rising debt-to-GDP levels a result of easy credit policies? Is it possible to hit a nominal GDP target with tight credit, if a nation is already under-shooting the target?

Lorenzo from Oz

Aug 14 2019 at 8:19pm

The useful pithy expression is a fine thing.

dlr

Aug 15 2019 at 10:22am

If NGDP is growing at 5%, why can’t entrepreneurs find more useful things to do with money borrowed at near zero percent? What’s changed from earlier decades?

One of the quirkiest aspects to recent global rates is that this may not be the right question. There’s no doubt that safe future consumption prices are very high AND that most conventional credit spreads are pretty normal, so somewhat riskier future consumption prices are also very high. But the same can’t necessarily be said about the riskiest future consumption. For example, Swedish stocks are trading at about 13.6X forward earnings, or about a 7.4% real yield in a very oversimplified world. So the implied spread between real equity returns and real junk bond (and safer bond) returns appears to be (at least superficiall)y enormous; and these numbers are not generally unique to Sweden. If this reflects something other than risk premia, it’s very hard to tell (i.e. earnings estimates do not predict margin reversion). Moreover, there is little evidence that global MPK has declined appreciably in the last ~30 years.

So it isn’t necessarily “why can’t entrepreneurs find more useful things to do” so much as why is there such an apparently strange kink somewhere in the middle of the risk curve, leading to a very low cost of safe investment and a not-low cost of riskier investment. There is other evidence backing this idea of a kink in the curve; most investors are well aware that the premium paid for lower-beta equities even without particularly high growth has risen substantially relative to high-beta “riskier” businesses. The normal answer for this sort of thing is just risk-aversion or recession-fears, but the lack of credit-spread compliance really muddies the waters. There might be a fairly consistent story to tell that has a highly stylized version of risk aversion where aversion is outweighed by demographic-based time preferences at relatively low overall levels, but then increases at an accelerated rate as risk perception increases. I don’t know.

Scott Sumner

Aug 15 2019 at 12:42pm

Could this have anything to do with the following. In the old days, if washing machine factories were highly profitable, new firms would enter the industry, making more washing machines. But if Google and Facebook and Amazon are very successful, it’s hard for new firms to enter their industry. High profits, but not high marginal profits on new investments?

Kenneth Duda

Aug 15 2019 at 5:00pm

Scott, I think that’s it exactly. The legal and regulatory climate makes it much harder to create than it should be. That’s true of houses and tech companies.

-Ken

TMC

Aug 15 2019 at 11:18am

Thanks for the post. I find monetary policy to often be counter intuitive. Even after the FED’s rate reduction, what would the next step to ease money?

Alan Goldhammer

Aug 15 2019 at 12:05pm

Taking a quote from the great Buffalo Springfield song, “There’s something happening here, what it is ain’t exactly clear…” From my non-economist vantage point, we are entering the world of the weird and it’s almost like being caught in a Pynchon novel. Just today I saw a story that a large two tower apartment development in our neighborhood has been canceled by the developers who are now trying to sell the property. All the zoning and permit requirements have been in place for two years and our neighborhood was waiting for this to happen with the realization that they had an inadequate traffic flow pattern. In addition, there was a large parcel of land, also in the neighborhood (inside the Washington beltway and close to downtown Bethesda and NIH) that received approval for up to 25 single family homes. That project was supposed to have broken ground this past spring and the developer in this case has also put that property up for sale.

We have these incredibly low interest rates that might go even lower and yet, two very appealing building projects are not going forward. I don’t fully understand NGDP growth and will leave it up to Scott to explain things but I can tell you as an investor the inverted yield curve and the current international trade situation leaves me quite worried. I think we will get some very bad news from the farm sector this fall and bankruptcies will be increasing (I hope not as bad as the mid-1980s). There is also a lot of shadow bank loans out in the commercial sector that might fail as well.

There are not a lot of good choices for investing these days.

Scott Sumner

Aug 15 2019 at 12:43pm

Good example.

nobody.really

Aug 15 2019 at 3:48pm

Perhaps the developers are concerned by the glut of homes coming onto the market from employees fleeing the Dept. of Agriculture, the Pentagon, Health & Human Services, Justice, Interior, Transportation, Labor, State, Energy, Education, Housing & Urban Development, etc?

Alan Goldhammer

Aug 15 2019 at 6:13pm

Those job losses are minuscule. The National Institutes of Health and the Walter Reed Medical Center are the two biggest employers and are within about one mile of the location (I also live in this neighborhood). They have a combined workforce of maybe 25K at the two locations. There is ample public transportation as well. Home here usually sell within 2 weeks of going on the market.

nobody.really

Aug 19 2019 at 10:54pm

I’ll take your word for it.

I note, however, that a glut of new apartments is allegedly driving down rents in Seattle.

John D

Aug 15 2019 at 1:38pm

Safe to say we’ve been in a liquidity trap since 2008?

Scott Sumner

Aug 15 2019 at 5:11pm

No.

mike

Aug 15 2019 at 3:43pm

Scott, I have a few thoughts on a general framework on interest rate dynamics right now:

Interest rate to borrow = base (real interest rate) + credit spread + other factors (duration / liquidity etc)

The base / real interest rate is historically low (excess savings, lack of productive investment opportunities, money printing, etc.)

The other factors (duration/ liquidity, currency risk etc) haven’t changed too much

But the risk premium has gone up, but not linearly, its gone up much more substanitally for smaller companies / newer companies.

Back in 2000 the 10 year was at 6.2%. Lets Say big company / good credit risk was +2% and good credit risk but small company was 6%. Big company credit = 8%, Small company 12%. Now with the 10 year at 1.5%, Big company rate is 3.5%, but small company is still 7.5%. The big company has had their rate cut substantially, (55%), and the small company less so (37% of so). So the big company not only had their rate cut more relatively, this also allows them to have much greater downstream advantages:

They can acquire customers easier (can spend more advertising or on sweetheart teaser deals. Higher CAC can be financed to make the LTV make sense)

They can attract best talent, because they can pay higher wages since their ROI from future profits from new projects is higher – due to lower discount rate of their cost of capital

They can make purchase capital goods / real estate more easily due to cheaper cost of capital

They can acquire competitors and both get immediate wealth/valuation bump, while also reducing competitive landscape. (A particularly good example of this was after financial crisis in the midwest I know of some small investment bankers who sold 10+ companies that were small banks .. think under 50 million equity value, trading at .5 book, to larger regional banks (think 1-20 billion) who were trading at 1.5 book. So suddently that bank just pocketed the “100 million” wealth effect, and also could be less generous in interest rates, and charge more fees on accounts etc

I know my comment is rambling, but what I think you see is the lowering of the real rate / risk free rate, is that this has disproportionate effects (advantages) for entrenched and large businesses over everyone else. Idea is not fully fleshed out and articulated here, but i hope it provides some interesting thoughts that don’t seem to be discussed to broadly by others

Scott Sumner

Aug 15 2019 at 5:14pm

Mike, Perhaps a finance person could chime in, but it’s not obvious to me that the percentage rate change matters, and not the absolute change in interest rates. In both cases there’s 400 basis point penalty for being small. But this isn’t really my area of expertise.

dlr

Aug 16 2019 at 9:03am

Could this have anything to do with the following. In the old days, if washing machine factories were highly profitable, new firms would enter the industry, making more washing machines. But if Google and Facebook and Amazon are very successful, it’s hard for new firms to enter their industry. High profits, but not high marginal profits on new investments?

I think there is something here to this, but it’s not simple. The winner-take-all and low marginal capital phenomena matter, but they may also muddy our conventional measurements. These days entry in tech often consists of many tadpoles incurring substantial operating losses to secure the pole position on a platform that may be new or maybe be sort of new and sort of competitive with part of an existing platform business. And once the one or two winners do secure the hub but are still in growth mode, they still incur more expenses and lower operating margins than historical winners. And in many cases, incumbents pay gaudy valuations for contenders or early leaders, though these acquisition aren’t considered capital expenditures in most measurements. The losses (or profits below where they would otherwise be) incurred in securing platform or network dominance (or protecting your own position via acquisitions) can be considered capital investment in many senses relevant to this conversation about risk and value.

This is not just a theory. Apparent winners like ServiceNow and Workday sport $40-$50b EVs trading at adjusted earnings multiples of 80-120X and still generate GAAP losses (mostly thanks to stock comp). Strong contenders like Zoom and Z-scaler trade at 20-40X forward sales without profits. Oracle and IBM have spent tens of billions to protects against winner-take-all startup encroachment. SalesForce has arguably moved into protect-mode even before hitting park-profit monopoly mode. The point is not that these valuations are silly or wrong. It is that this phenomenon of “hidden capital” should be an important counterweight (along with the high multiples assigned to existing earnings streams) to P/E compression expected from growing obsolescence risk and lower conventionally available capex growth. And, in fact, looking case-by-case, it’s clear that the market assigns huge valuations, conventionally measured, to these sorts of platform/network races. In the venture and unicorn markets, it’s even more obvious.

Throw in the large incumbents like MSFT and GOOG and AMZN trading at higher-thank-market multiples, and it’s not at all clear you should expect overall equity multiples to appear lower than you’d otherwise expected relative to, say, junk bonds. It’s not an easy question.

José

Aug 16 2019 at 10:33am

Prof. Sumner, you said “Governments could think about removing regulatory barriers to investment in housing, infrastructure and other useful activities.”

A few years ago I commented in one of your posts that regulation could be the cause of low growth, low rates. You were not decisive, but you didn’t agree with me then. It seems you have changed your mind somewhat.

I don’t mean to be a “I told you so” guy, don’t take me wrong. But I do think we should enphasize that the regulatory environment we have now is NOT NEUTRAL on growth potential. I don’t really see policymakers conceding this issue (except for Trump?), unfortunately.

Thaomas

Aug 16 2019 at 7:25pm

“The best way to judge the stance of monetary policy is by looking at the growth rate in “M*V” aka nominal GDP”

It seems to me the best way is to point to the values of the instruments and compare them to the values they would have under an optimal policy.

Mike Sandifer

Aug 17 2019 at 8:59am

Scott, here’s what I don’t understand about your perspective. To the degree low rates are driven by a global savings glut, why don’t you expect that to expand RGDP potential, ceteris in counparibus,even tries like Sweden now, or the US last year?

As you know, I’ve continued to view most of this as an aggregate demand shortfall.

Seppo

Aug 17 2019 at 1:28pm

Using Sweden’s housing market as an example of anything is very dangerous unless one knows its kinks.

Firstly, there are very strong zoning restrictions in place, so supply is reduced.

Additionally ALL rental flata are rent controlled, even privately owned ones and you can only get a rental contract through publicly managed queue. Practically no rental flats are being built (considering the insane demand vs supply) and queues to first hand rental contract can be 10+ years in most wanted neighbourhoods.

Yes, if you own a flat in sweden, you can’t rent it legally to whoever you want, at whatever price they agree to pay.

Rental flats are in such demand, that if you get one, you never let go of it. Even if you buy your own house, you keep the rental flat and sublet it (regulated little premium can be collected).

Sweden’s housing market is totally broken and it is a great mystery to me how the country can even function with it. I just know that there are people making close to 6 figures a month unable to get first hand rental contracts.

This system forces everyone to buy, even if they’d rather not due to being (highly paid) engineer immigrants and being unsure if they plan to stay indefinitely.

I wouldn’t think much of the strength of housing market under such conditions.

Seppo

Aug 17 2019 at 1:30pm

Six figures a month in SEK, so close to $10k/month.

Jason Boileau

Aug 17 2019 at 4:38pm

It’s not true that mortgage rates are -0.5 % in Denmark. Mortgage backed securities are available with a coupon rate of -0.5%, but the yield is closer to 0 at the moment, and the actual mortgage has a positive rate when including other fees, probably around +0.5%.

Chris

Aug 22 2019 at 9:02am

Is this largely due to demographics? Boomers are close to their peak wealth share and are retiring from the work force. The risk preferences for their savings is lowering as they age. Their pensions and life insurers are required to purchase government debt regardless of the price. And with higher life expectancy than during previous generational booms, their savings won’t be transferred to 30-something children, but to children often approaching retirement themselves. A much larger portion of wealth is and will be held by an older, risk-averse population.

Comments are closed.