Nearly everybody seems to think so, including many economists: when a price rises, it fuels inflation. The venerable magazine The Economist doesn’t think twice about it. Speaking of Argentina, it writes (“Javier Milei’s Next Move Could Make His Presidency—or Break It,” June 19, 2024):

Monthly inflation may creep up in June as energy prices rise.

The Wall Street Journal runs a headline saying “Rent Hikes Loom, Posing Threat to Inflation Fight,” June 18, 2024. Examples are everywhere.

But if every price increase fuels inflation (a general rise in the price level), it must be that every price cut threatens deflation (a general drop in the price level, seen in recessions). Other things being equal, then, every price drop on the market is a threat, just like every price increase is. Every price change is a bad omen. Is this strange theory valid? No. The error lies in the failure to distinguish changes in relative prices and a change in the general level of prices, that is in all prices, which is what inflation (or deflation) is.

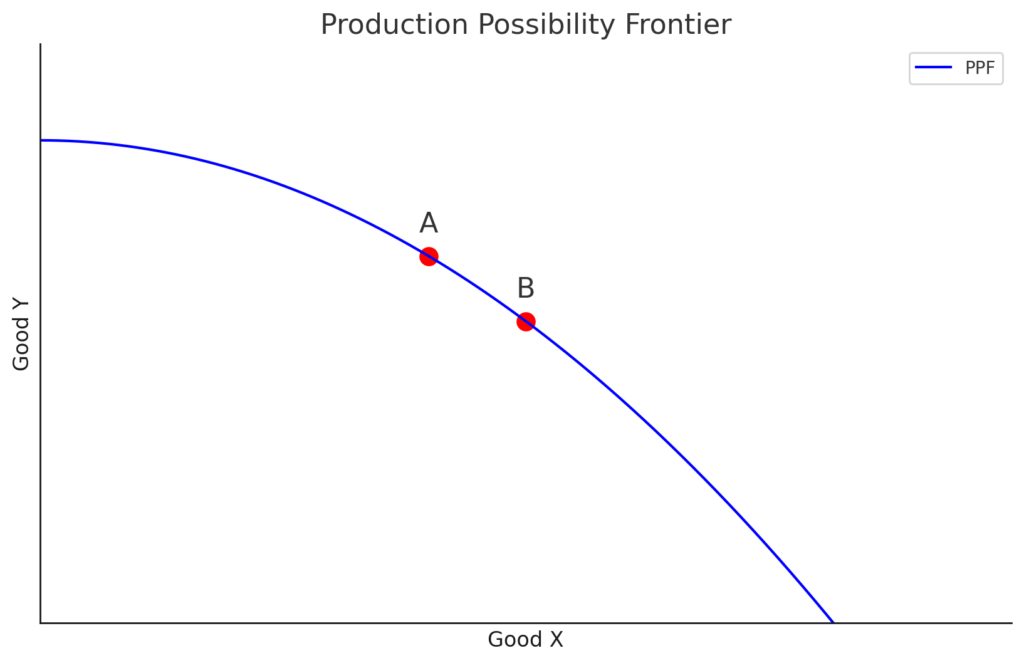

Imagine that there is no inflation nor deflation and that the demand for beef increases, everything else being the same. As a consequence, the price of beef increases relative to (say) pork. This is the same as saying that the economy has moved on its production possibility frontier (PPF) to more beef and less pork, which implies that beef now costs more relative to pork. (The chart below shows a standard PPF for an economy with two goods. If good Y is beef and good X is pork, the economy has moved from point B to point A.) Any price index (say, the Consumer Price Index) will have changed between the original situation B and the new one A on the PPF. Whether the index shows an increase or a decrease will depend on the precise quantities of beef and pork because these quantities are the weights with which the price index is calculated. It would be a fluke if it did not change. Thus, we cannot use a change in a relative price to conclude that inflation or deflation is present.

Inflation—a general increase in the level of prices—is a different phenomenon, caused by the quantity of money in the economy.

Inflation—a general increase in the level of prices—is a different phenomenon, caused by the quantity of money in the economy.

If there is inflation, a price index catches both the changes in relative prices and the change in the general level of prices. We cannot attribute part of the inflation to the change in a specific price, because the latter change is partly due to inflation (how all prices have increased)–and partly due to the change in that price compared (relative) to other prices. Rents or energy prices cannot fuel inflation (or deflation) because they are partly caused by it. Causality works the other way.

I have written a few EconLog posts on this topic, but my recent article “A Rising Product Price Doesn’t Cause Inflation,” in Ryan Bourne, editor, The War on Prices (Cato Institute, pp. 19-27) provides a more detailed explanation. My post “Guns and Butter” contains another illustration of the PPF concept.

******************************

Does a price cut fuel deflation? By DALL-E and your humble blogger

READER COMMENTS

marcus nunes

Jun 23 2024 at 1:35pm

Not just the quantity of moneysupplied but also the quantity of money demanded

Pierre Lemieux

Jun 23 2024 at 2:23pm

Marcus: Yes, if the supply does not automatically adjust.

steve

Jun 23 2024 at 5:56pm

So what happens when our next president adds a 60%-100% tariff on all imports?

Steve

Mark Barbieri

Jun 24 2024 at 9:25am

I’ll try to answer this, despite not being an economist. Here’s what I think would happen:

First, the price of imports rises and the quantity demanded at those higher prices decreases. Because the demand declines, the resulting price of imports is higher than it was before the tax but lower than the original price + the tax.

Domestic goods in competition with foreign goods will see an increase in quantity demanded because the increase in price of imported goods makes them less attractive. That will increase the price of domestically produced goods that are in competition from foreign goods. So far, the price of imports and domestic goods competing with imports are rising, so do we have inflation – a general rise in the price level? Not necessarily.

The money to pay these higher prices has to come from somewhere. Absent a change in the money supply, the people will have less money for other goods, shifting the demand curve. That results in lower prices on domestic goods and services not in competition with imported goods.

Whether the tariff causes inflation depends on how the Fed reacts and how the tax would impact RGDP. If the import tax reduces RGDP because of supply impacts, that would cause demand-driven inflation. If the Fed responds by shrinking the money supply proportionally, there would be no inflation. If the Fed responds by increasing the money supply, inflation would be even worse.

Matthias

Jun 25 2024 at 1:26am

To a first approximating tariffs are a negative supply shock. As you suggest, monetary policy will determine how the nominal impact will be felt.

Pierre Lemieux

Jun 24 2024 at 3:48pm

Thanks, Mark, for daring to be first–and to you Steve for the question. I have not seriously studied all the consequences of replacing the current average tariff of 1.5% with a 50% one, which would also apply to all imported goods (the majority of them) that are not currently tariffed. The cost for consumers would be enormous–including the cost of autarky in the goods for which the new tariff would be prohibitive (reducing domestic demand for imports to zero). The real cost would be losing the benefits of comparative advantage–buying where it is cheaper, selling where it is dearer. Against these costa, we would have to consider the benefits of abolishing the personal income tax (IF it were really abolished!) in terms of incentives to work; this would push up the PPF. My guess is that the deadweight loss from the income tax is smaller than the cost of partial autarky (abandoning the benefits of comparative advantage). This guess would probably translate into a certainty if foreign governments were to retaliate. Moreover, replacing $2 trillion of income tax revenues, which come from progressive taxes, with $2 trillion in regressive tariffs might start a revolution or a civil war (if such things are still possible under Leviathan). Not that I am an advocate of progressivity but, for poorer people, the income impact would be much much worse than the “China shock.”

As for your hypotheses, a couple of points must be remembered. First there is only one price in a market (at equal quality, evaluated by the consumers themselves). In the general case, a tariff of 50% will increase the price of the good imported AND ITS DOMESTIC SUBSTITUTES by 50%. Indeed, this is why domestic producers like tariffs. See the practical example I report in my post “A Simple Illustration of Standard Trade Theory.”

Second, I agree with your penultimate paragraph (which describes a move along the PPF). Inflation can only happen if there is an increase in the money supply that is not in response to an increased demand for money.

I also agree with your last paragraph, if I understand it correctly. The only way, I think, a 50% tariff/tax on all imported goods could cause inflation is if a supply shock followed (especially after retaliation, wide popular discontent, bankruptcies of large exporters [because exports would be reduced as much as imports, according to the Lerner theorem]), that is, if the PPF was pushed down and the Fed did nothing just like in the early 1930s. My guess is that what would be most likely to follow, perhaps after a short inflation, is a banking crisis and a depression.

Again, all these are tentative and poorly quantified scenarios (which Steve and Mark “forced” me to reveal), and I would appreciate comments and criticism.

Craig

Jun 25 2024 at 9:09am

“Against these costa, we would have to consider the benefits of abolishing the personal income tax (IF it were really abolished!)”

If I make a $100 and give $50 to the income tax and buy an imported product for $50, that is one thing. If I make $100, keep $100 and pay $75 for the imported product. I’m $25 ahead, no? Now, for sure that is back of the envelope math, but there’s other considerations with respect to the income tax as well including the fact that filing, but for the fact that it was enabled by an amendment, would violate the concepts of the IV Amendment.

“Moreover, replacing $2 trillion of income tax revenues, which come from progressive taxes, with $2 trillion in regressive tariffs might start a revolution or a civil war”

As long as Americans can drive to it in their F150 after getting thru the McD’s drive thru line.

Pierre Lemieux

Jun 25 2024 at 11:27am

Craig:

You write:

In fact, with an income tax rate of 0%, you would probably work more and earn more than $100, which strengthens your argument, if everybody else is identical to you. The problem (I raised it with the progressivity and regressivity issue) is that the “poor” who currently earns $50, pays $10 in income tax, and spends $40 in goods, would now just be able to buy for $27 of goods (on which he would pay $13 in tariff tax; his standard of living would have dropped by 1/3. And the poor are much more numerous than “you.”

So the guy in his F150 would earn less in his job at McDo (a more or less autarkic America would quite probably be poorer) and would now be driving a Ford Fiesta which would have cost him $24,000 instead of $16,000 as before. (Remember the Law of One Price.)

Craig

Jun 25 2024 at 1:24pm

“his standard of living would have dropped by 1/3. And the poor are much more numerous than “you.””

Just as an aside to this, I applied the tariff at retail, the tariff would obviously be applied at the border.

“(a more or less autarkic America would quite probably be poorer) ”

One of my takeaways from you, Pierre, is that there are innumerable nuances and tradeoffs that I am obviously not in a position to calculate. So for sure, you absolutely might be correct here. Indeed I would even say if this were done all at once it would probably cause a shock to the system. But I would ask with respect to an ‘autarkic’ America whether you mean autarkic like Albania under Communism, or ‘autarkic’ like 19th century America?

Pierre Lemieux

Jun 29 2024 at 4:06pm

Craig: About “autarkic” 19th-century America, Doug Irwin has a good answer. Protection against imports of goods was high in America–although not high enough to stop imports, as the latter were financing the federal government. But immigration was wide open. A poor German, instead of staying in Germany and benefiting from a job in a firm exporting to America, just moved to America. Protectionism and immigration are substitutes.

Thomas L Hutcheson

Jun 25 2024 at 11:18am

Repeat after me (and Milton Friedman), “Inflation is everywhere and at all times a monetary [policy] phenomenon.”

It is not caused by shifts in demand. It is not cause by negative supply shocks or positive demand shocks. [Or positive supply shocks or negative demand shocks, for that matter.] It is not caused by budget deficits. It is 100%, totally, entirely, without exception the Fed’s policies. Central bankers like to try to avoid taking responsibility and politician let the get away with it, but recognized or not, the responsibility lies with them.

Now it is true that shifts in demand and shocks and budget deficits can lead a central bank like the Fed that is pursuing a flexible average inflation target (FAIT) to decide, in response to a shock, to raise inflation temporarily above it targeted rate in order to facilitate the adjustment of relative prices to a new income maximizing configuration (~ prevent some markets from not clearing, ~ resources becoming unemployed). Well executed that is a wise decision. But it is still a Fed _policy_, not the shock, that caused the inflation.

Pierre Lemieux

Jun 26 2024 at 11:56am

Thomas: Well said. I broadly agree (which goes on to prove that we don’t disagree on everything!).

Craig

Jun 24 2024 at 2:42pm

Its one thing to get the inflation genie back in the bottle. The problem is Argentina has done that before and then reverted to form. The Argentine people need to get the government out of the money business completely.

Pierre Lemieux

Jun 24 2024 at 3:52pm

Craig: And it is easy for the government to say, “it’s the fault of rents, “it’s because of oil prices,” “it’s your fault!“

Craig

Jun 24 2024 at 5:48pm

Governments do many things, take responsibility for inflation is rarely one of them.

Matthias

Jun 25 2024 at 1:27am

Well, many Argentinians already use American dollars. So that way they at least got the Argentinian government out of their money business.

We might grumble about the US government, but it’s still an improvement.

Robert EV

Jun 28 2024 at 3:32pm

It’s microecon, but this makes me think about when I go shopping and something I usually get is out due to either a sales (demand shock) or being at the wrong end of a resupply (supply shock). I’m forced to either go without, or to purchase either a more expensive replacement or a less desired replacement.

Due to the way just-in-time retail stocking works, the sales price demand shock does not result in a later glut that drives down prices from the non-sales price. Some people just get lucky and get an extra full pantry, while others get hit with higher prices or a less desired substitute, but the long-term price trajectory remains the same.

Comments are closed.