I’m continually amazed by the media coverage of China’s deflation problem, which is treated as a big mystery. Actually, almost all modern examples of deflation have the same explanation—relatively tight money. (To be sure, deflation can be caused by a positive supply shock, but that rarely occurs under modern fiat money regimes.)

Central banks can only hit one target at a time. Most developed countries target inflation at around 2%, which forces them to allow highly volatile exchange rates. Those that stablize their exchange rate are unable to target inflation. When their currencies become overvalued, they are forced to engage in “internal devaluation”, i.e., deflation of domestic wages and prices.

Over the past few decades, China’s currency has been either rigidly fixed to the US dollar (1995-2005 and 2008-2010), or kept within a narrow band around the US dollar. At no time has the Chinese government allowed the yuan to move dramatically up or down, as we see with other currencies like the yen, the euro, the pound, and Swiss franc. Because of China’s exchange rate policy, Chinese monetary policy is essentially made in the USA. A strong dollar in the foreign exchange markets leads to deflation in China. Period, end of story. But the press consistently ignores this issue. Here’s Bloomberg:

Why is China experiencing deflation?

Prices rocketed in the US and other big economies when they reopened after the Covid-19 pandemic, as pent-up demand coincided with shortages in the supply of many goods. Predictions that the same would happen in China proved to be wrong. Consumer spending power is weak and a real estate slump has dented confidence, causing people to hold back from buying big-ticket items.

A tightening of regulations in high-paying industries like technology and finance has led to layoffs and salary cuts, further dampening the appetite for spending. A policy push to develop manufacturing and high-tech goods spurred increased production, but demand for these goods has been weak, forcing businesses to mark down their prices.

That’s it. That’s the entire explanation. Much of the rest of the article is devoted to possible solutions, with no mention of exchange rate adjustment or internal devaluation.

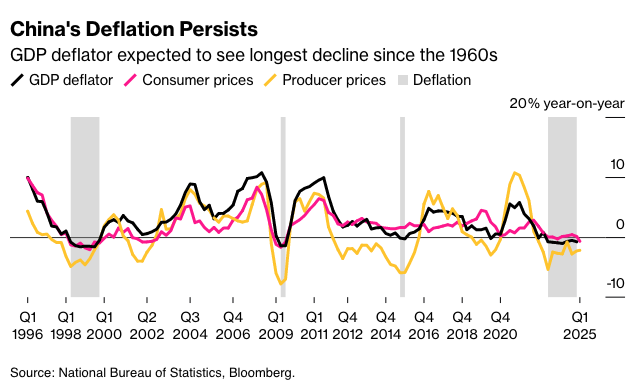

The article even includes a graph, which provides very strong clues as to what is causing these repeated episodes of Chinese deflation:

The grey bands represent periods of deflation using the GDP deflator. Notice an extended period in the late 1990s, a brief period around 2009, a brief period around 2015, and an extended period since 2023.

Now let’s examine the real exchange rate for the US dollar against a basket of other currencies:

Notice a very strong appreciation of the dollar in the late 1990s, a brief surge in 2009, another surge in 2015 and an exceedingly strong dollar over the past few years.

Of course it’s not a perfect fit, as the yuan was not rigidly fixed to the US dollar. The yuan did depreciate somewhat in the late 2010s, which helped to make the 2015 deflationary period fairly brief. And the equilibrium real exchange rate can move around for reasons unrelated to monetary policy. But as a general rule, a strong US dollar means tight money for any country with its currency pegged to the dollar, or even kept relatively stable against the dollar.

So why didn’t most other countries have deflation in the late 1990s? Most other countries allowed their currencies to depreciate against the dollar. Those that didn’t (China, Argentina, Hong Kong) generally experienced deflation. Deflation also hit countries that allow only slight currency depreciation, due to pressure from the US government. The Japanese yen/US dollar exchange rate showed very little change between 1997 and 2002, while most of the rest of the world was sharply depreciating their currencies. The result was Japanese deflation.

It’s not complicated. In the 21st century, deflation is generally caused by a policy of exchange rate stabilization combined with a strong US dollar.

READER COMMENTS

Arqiduka

Mar 15 2025 at 5:48am

I thought the story was supposed to be that a central bank could only target as many indicators as it has tools?

Which is patently wrong, and indeed a central bank can credibly target one and only one nominal indicator.

Thomas L Hutcheson

Mar 15 2025 at 11:09am

True, but the target (and the flexibility around it) can be chosen to optimize, say, a function of inflation and real income.

Scott Sumner

Mar 15 2025 at 1:09pm

I believe the argument is that monetary policy can only target one objective at a time. If you have a second objective you need something else, such as supply-side tax changes.

Thomas L Hutcheson

Mar 15 2025 at 11:05am

I agree with almost everything except the headline. No one in the US is standing in their way to have a more simulative monetary policy.

Dylan

Mar 15 2025 at 3:09pm

Macro makes my head spin, so apologies for a stupid question. But if a strong dollar must lead to deflation in China with a quasi-pegged yuan, why does it not also lead to deflation in the U.S? A strong dollar means each dollar can buy more stuff, and isn’t that pretty much the definition of deflation?

Scott Sumner

Mar 16 2025 at 1:57pm

I’m describing a strong dollar in terms of the real exchange rate. That means it only produces deflation in the price of imports (and foreign travel). Deflation is only a problem when it occurs with domestically produced goods and labor.

Dylan

Mar 16 2025 at 5:53pm

But I’m told that literally everything is made in China. So obviously imports must be 100% of consumption, right?

Seriously though, thanks for the explanation.

spencer

Mar 15 2025 at 5:05pm

re “why does it not also lead to deflation in the U.S?”

Foreign direct investment?

spencer

Mar 15 2025 at 5:46pm

Gross Domestic Product (A191RP1Q027SBEA) | FRED | St. Louis Fed

Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis (DGS10) | FRED | St. Louis Fed

Trade Balance: Goods and Services, Balance of Payments Basis (BOPGSTB) | FRED | St. Louis Fed

Something funny about the monkey.

Comments are closed.