During 2008-09, both the US and the Eurozone had deep recessions, with the Eurozone experiencing an especially sharp fall in NGDP growth. In both areas, the central bank should have cut rates into negative territory, but neither bank did so (at the time).

Even so, there were clear differences in the response of the two central banks. The Fed reduced rates more aggressively (relative to the natural rate), and also did QE much earlier than the ECB. Some ECB officials were critical of the Fed’s aggressive response, and preferred a more conservative approach. This comparison represents an interesting case study. What would you have expected in each region?

In the late 1990s, Milton Friedman told us what he would have expected. Friedman argued that the ultra low interest rates in Japan were a sign that money had actually been quite restrictive in the past:

Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy.

. . .

After the U.S. experience during the Great Depression, and after inflation and rising interest rates in the 1970s and disinflation and falling interest rates in the 1980s, I thought the fallacy of identifying tight money with high interest rates and easy money with low interest rates was dead. Apparently, old fallacies never die.

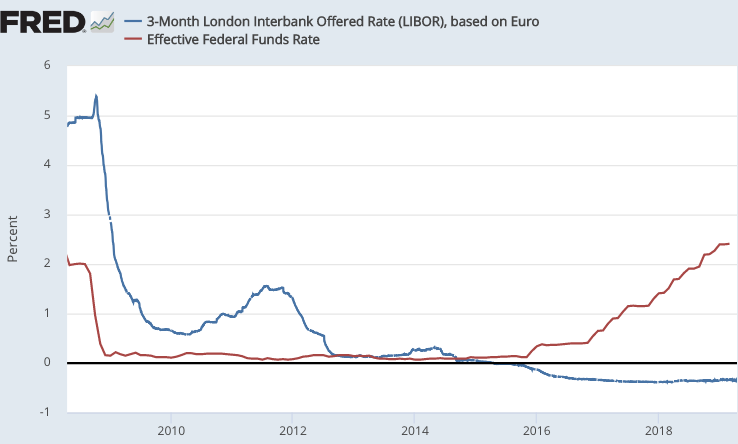

The Europeans thought Friedman was wrong. Let’s see how each view holds up, a decade after the 2008-09 recession. If Friedman was right, then the tighter monetary policy in the Eurozone (which was initially associated with higher interest rates) would eventually lead to lower interest rates than in America. And that’s exactly what happened:

(Ben Bernanke must smile every time he sees this graph, thinking about the criticism he got back in 2009.)

(Ben Bernanke must smile every time he sees this graph, thinking about the criticism he got back in 2009.)

Hardly a day goes by where I do not encounter at least one article that misunderstands this basic point. Thus a recent Bloomberg article on Fed policy and inequality is based on the premise that low interest rates represent an expansionary monetary policy:

If the recession-fighting techniques of the last decade are responsible for widening inequality, central banks will need a new set of tools soon or risk not only widening the wealth gap but also eroding confidence in their ability to set monetary policy. And there is emerging evidence that could be the case.

A new paper from economists Ernest Liu, Atif Mian and Amir Sufi suggests the reason the recession didn’t put a dent in inequality may very well be the Fed’s fault. Low interest rates, particularly when they get to close to zero, tend to increase inequality, even as they revive the economy, the economists argue.

In the short term that can be true. But inequality is a long-term problem, and the long run correlation between the stance of monetary policy and interest rates is exactly the opposite of the short run correlation.

If you are worried that low interest rates worsen inequality (I don’t believe they do so), then you should favor an easy money policy during recessions, as in the long run this will lead to higher interest rates. A tight money policy will leave rates close to zero for decades on end, as we’ve seen in Japan and are beginning to see in Europe.

I also question the claim that low interest rates lead to higher inequality, as that is an example of reasoning from a price change. Low rates might be caused by a deep depression, as in the 1930s. In that case, inequality fell sharply. Alternatively, low rates might reflect a long-term decline in the natural rate of interest, as we’ve seen since 1980. In that case, it may lead to higher asset prices and more inequality. In neither case did the change in rates reflect the short run impact of monetary policy.

If rates are reduced as part of an easy money policy (the so-called “liquidity effect”) then it tends to helps those at the top (stock investors) and also those at the bottom (the unemployed) and hurts some of those in the middle with secure jobs (teachers, nurses, etc.) Overall, most people are probably helped by an easy money policy adopted during a recession, regardless of the impact on inequality. But those are merely short run effects.

In any case, inequality is a long-term issue that is unaffected by monetary policy, which is neutral in the long run. Confusing the secular decline in the natural rate of interest since 1980 with “easy money” will lead to bad monetary policy in the future, hurting those at the bottom of society. Even worse, a relatively tight money policy won’t even deliver the higher interest rates that its proponents assume it will produce. Just look at Europe.

HT: Stephen Kirchner

READER COMMENTS

Gordon

Apr 26 2019 at 5:58pm

Scott, speaking of interest rate policy, what are your thoughts on the PCE core data from today’s GDP release? Year over year PCE core was 1.7% and the annualized PCE core for Q1 was 1.3%.

Benjamin Cole

Apr 26 2019 at 8:08pm

Ditto, even in sophisticated financial media, the Bank of Japan policy is described as “ultra-loose.”

I do not think central banks should be concerned with the idea of financial inequality. Not their bailiwick.

That said, the idea that the Federal Reserve considers a 4.65% rate of unemployment to be “natural” is to witness institutionalized perversion in action. The Fed “Beige Books,” with their constant caterwauling about “worker shortages” are also an example of class warfare in action. PU!

Inflation appears dead in Europe and Japan. Perhaps those central banks should concentrate on generating as much employment as possible.

Nothing could be better for the United States than a couple generations of very tight labor markets and rising real wages.

Ahmed Fares

Apr 26 2019 at 10:20pm

From the linked article, first this:

There is no limit to the extent to which the Bank of Japan can increase the money supply if it wishes to do so.

I’m assuming the above was base money and not broad money. Then this:

After a year or so, the economy will expand more rapidly; output will grow, and after another delay, inflation will increase moderately.

What did I miss? It’s like something magical happened. How exactly does expanding base money lead to an expanding economy? Assume for the sake of argument that consumers don’t want want to borrow and spend and businesses therefore have no need to add capacity.

Trevor Adcock

Apr 27 2019 at 4:38am

Assume the economy doesn’t expand and it can’t.

For the sake of argument assume people have more money and the prices of the goods they usually buy don’t increase. Would they buy more goods?

Mark

Apr 27 2019 at 7:54am

It seems like lower interest rates should decrease inequality in the long run because the wealthy are more likely to be net creditors. Even if stock and bond prices are boosted for today’s wealthy who own stocks and bonds, their future returns will be lower for tomorrow’s wealthy when they buy stocks and bonds.

Thaomas

Apr 27 2019 at 11:13am

Unfortunately, those who understood that the Fed was not being aggressive enough in 2008-13 did not make a clear argument about what more should have been done*: no positive interest on reserves, much more aggressive (and not time and amount self- limited) purchases of longer term USD denominated assets and or foreign exchange denominated assets, explaining that this would continued until they had achieved symmetric inflation of 2% and unemployment below 4%. [Granted that recent experience has shown that 4% unemployment is too high, but it was a reasonable target in 2008.]

* I wonder if this does not go back to Freedman’s saying that low interest rates ARE not a sign of loose monetary policy, rather than saying clearly that sometimes (specifying the circumstances) “low” interest rates can still need to be lowered more or other policy instruments used to achieve improved macroeconomic performance.

Scott Sumner

Apr 27 2019 at 1:26pm

Gordon, Yes, that shows that inflation continues to run a bit below the Fed’s target. I wouldn’t say that’s a huge problem (it should be below 2% when unemployment is below the natural rate), but it’s a problem.

Ahmed, Friedman did not pay enough attention to the distinction between temporary and permanent monetary injections.

Mark, Hard to say, it depends on why interest rates fell.

Thaomas, You said:

“Unfortunately, those who understood that the Fed was not being aggressive enough in 2008-13 did not make a clear argument about what more should have been done*:”

Market monetarists certainly discussed what should have been done.

Comments are closed.