Bryan Caplan has a new post where he suggests that we’d be better off if firms raised prices enough to eliminate shortages. He also suggests that he does not want to raise aggregate demand. I believe his views are sensible, but I don’t entirely agree with his reasoning. Bryan suggests an analogy with price controls in a single market, and that analogy doesn’t hold in a macro context.

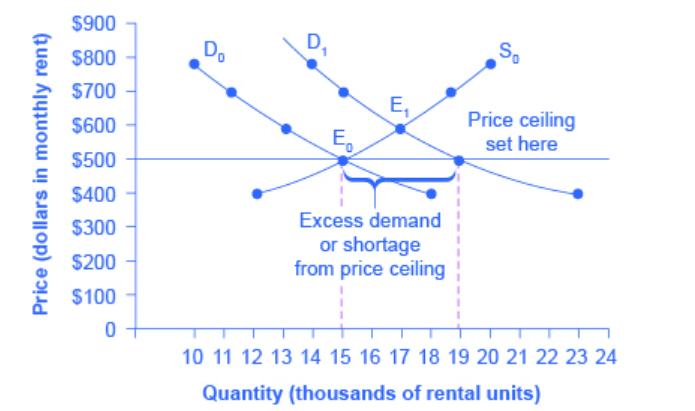

Here’s a graph showing the impact of price controls in a micro context:

When price controls are removed, production and consumption rise from 15,000 to 17,000, while quantity demanded falls from 19,000 to 17,000. It might seem odd that consumption should rise while quantity demanded falls, but there were 4,000 units demanded at the controlled price that were simply not available to be purchased. Phantom demand. Therefore we move from point Eo to E1 when controls are removed, and consumption rises.

Now consider what happens when firms raise prices to eliminate shortages in a macro context:

In this case, the economy moves from point b (where there is excess demand) to point c. Unlike in the microeconomic case, consumption falls after the price increase. At point c there are no longer any shortages, but people are buying fewer goods. This is because we’ve followed Bryan’s suggestion of avoiding a further increase in AD when prices rise. (He’s silent on whether to reduce AD, but he clearly doesn’t want an increase.) In contrast, in the microeconomic case the removal of price controls causes nominal expenditure in the affected market to rise. Macro is not like micro—beware of economists using analogies. Here’s Bryan:

The reason why we need more inflation is simple: ubiquitous shortages. This problem isn’t merely on the news; at this point, something I want to buy is unavailable practically every day. Pre-Covid, that would have happened roughly one a month.

So what? Well, as any standard econ text tells you, shortages exist because at the current market price, the quantity demanded exceeds the quantity supplied. To solve these shortages, we need market prices to rise. This discourages consumption and encourages production until everything you want is conveniently available. Like in the good old days before Covid.

Actually, removing price controls encourages consumption, by making goods more available. (It reduces quantity demanded, but increases quantity purchased.)

I suspect that Bryan believes that if retailers raised prices to eliminate these annoying shortages, he’d end up buying more goods. And that might be true, especially if Bryan is much richer than the average American. But if prices rise while aggregate demand (NGDP) remains unchanged, then output will necessarily fall. The average American will buy fewer goods. That still might be a good thing, as shortages cause a loss of utility in all sorts of subtle ways not picked up in the government’s real GDP data. Nonetheless, the microeconomic analogy that Bryan uses doesn’t really apply to the macro case.

PS. The AS/AD graph I used here is not optimal for making my point. A better graph would have shown no initial change in either AD and SRAS, with LRAS shifting left during Covid. Then firms raise prices to move the economy up and to the left to the new (reduced) LRAS, eliminating shortages. SRAS moves left. The big problem today is unusually low LRAS, not unusually high AD. But the basic point is the same; holding AD constant, eliminating shortages with higher prices means reducing output. That’s very different from the effect of removing a price ceiling in a single market.

READER COMMENTS

OneEyedMan

Jan 25 2022 at 12:01pm

I really enjoyed this post. Extremely clarifying.

Andrew_FL

Jan 25 2022 at 1:06pm

Bryan has forgotten Walras’ Law

nobody.really

Jan 25 2022 at 1:19pm

Maybe ‘cuz he’s the eggman?

Wade

Jan 26 2022 at 1:39pm

How do you figure?

Andrew_FL

Jan 26 2022 at 2:21pm

Bryan seems to believe there can be a general shortage of goods & services, but this is impossible. By Walras’s law, the existence of shortages in some markets implies *balancing* surpluses in others. Bryan can’t see the surpluses, but they exist.

Even if you include money as a good, this doesn’t save his argument, because in order for there to be a general shortage of goods there must be an excess supply of money-which Bryan explicitly denies is the point of his post!

MarkLouis

Jan 25 2022 at 1:24pm

You don’t need broad-based inflation to help solve shortages. You need higher prices in the affected goods; which can easily be offset by lower prices elsewhere. Economists seem rather bad at differentiating between relative prices and the aggregate price level.

Scott Sumner

Jan 25 2022 at 2:58pm

Bryan obviously understands that point.

Danny

Jan 25 2022 at 2:31pm

The big problem today is unusually low LRAS, not unusually high AD.

There seems to be a lot of disagreement on this point among pundits. I assume your reasoning is that NGDP is close to trend which means that AD is at about the correct level, which means that LRAS must be low?

Scott Sumner

Jan 25 2022 at 2:59pm

I do believe NGDP is somewhat too high, but the much bigger problem is low LRAS (as many workers have left the labor force.)

AMT

Jan 25 2022 at 6:41pm

There is a big difference between encouraging, and increasing. When there are large shortages, you can discourage consumption via higher prices and still increase quantity purchased. I think I’ll have to quote you, “Bryan obviously understands that point.”

Isn’t Bryan’s whole point that staying out of equilibrium for longer is bad? You say that consumption decreases as we move from point b to c. But that MUST happen eventually, since you cannot stay producing beyond the LRAS. That extra production and consumption is not a free lunch; it is suboptimal. His point is that the sooner we get back to equilibrium and equate supply and demand, the better, because this WILL happen eventually, but the longer it takes to get there, the more inefficiency we are experiencing in the meantime.

So along the same lines, of course we will reduce aggregate output, but we MUST do so to get to the optimal level of output.

Scott Sumner

Jan 26 2022 at 12:49am

This may all be obvious to you (and perhaps to Bryan). But look at his comment section—lots of them are confused.

Rajat

Jan 25 2022 at 7:12pm

I don’t think I agree with you, Scott. Why would Bryan be observing shortages today if the economy were actually producing at point b? Isn’t the gap between b and a ‘phantom demand’ like in your micro diagram? Your AD/AS diagram works when we have a positive shock to nominal demand that ‘fools’ firms into producing more than they would in LR equilibrium. There are thus ordinarily no shortages at point b for that reason. However, b is not sustainable and as prices rise, output contracts back to the LR equilibrium.

Scott Sumner

Jan 26 2022 at 12:41am

“Isn’t the gap between b and a ‘phantom demand’ like in your micro diagram?”

Yes, but in the micro example that issue gets resolved by spending more in nominal terms and buying more units of good X. In the macro example the issue is resolved by spending the same amount of nominal dollars and buying fewer goods.

“There are thus ordinarily no shortages at point b for that reason.”

That’s true in a monopolistic competition model. But that’s not the issue Bryan is discussing. A model with actual shortages also has a point b.

BC

Jan 25 2022 at 9:51pm

Bryan’s post got me thinking about inflation and shortages. In labor markets, nominal wages are sticky downwards. So, to avoid unemployment (labor surplus) when real wages are too high, we need inflation to raise all other prices so that real wages can fall. A price control (or other upward nominal price stickiness) is the mirror image of downward stickiness. Shortages arise when the *real* price of a good can’t rise. So, to allow the real price to rise when the nominal price is upward sticky, we actually need *deflation* in all other prices. When the “thermometer is broken” as Bryan says and the nominal price of a good can’t rise quickly enough, then we actually need deflation (or less inflation), rather than more inflation, to increase the *real* price of the good in question to avoid a shortage.

Then, could the recent high inflation at least partly explain the many shortages that we’re experiencing? Even without formal price controls, some prices are upward sticky because firms don’t like the bad PR that comes from raising nominal prices, for example. Especially since we have become accustomed to 2%- inflation for many years, it seems plausible that many pricing practices may have arisen that make “keeping up” with 7% inflation difficult. Of course, we also have many formal anti-gouging laws and informal political pressures against raising prices, especially during a pandemic.

Inflation can compound problems when real factors like workers leaving the labor force call for real price increases. Suppose a firm has difficulty finding workers and must raise real prices by 5% to continue operating profitably. If inflation is 2%, then the firm needs to raise nominal prices by 7%. If inflation is 7%, however, then the firm would need to raise nominal prices by 12%. A 12% nominal price increase might be more noticeable to customers than a 7% increase and might engender more ill will, attract more regulators’ attention, etc.

Scott Sumner

Jan 26 2022 at 12:52am

To figure out the appropriate inflation rate you must first determine AD, and then the position of the LRAS. Relative price change models are not enough.

MikeDC

Jan 27 2022 at 8:09am

I believe Scott’s response is misleading. He says Caplan:

but what Caplan actually says is:

Aggregate demand can increase without aggregate demand policy. Working of the AD/AS graph, Bryan is saying that a shift of SRAS to SRAS’ will be accompanied by an outward shift in both AD (to AD’) and LRAS.

This doesn’t seem to be controversial since Scott is also saying LRAS is abnormally low. Increasing price level will lure those workers back to work.

Comments are closed.