The Economist recently ran an article comparing the economic crises in Turkey and Argentina:

Failing conventionally

Why Argentine orthodoxy has worked no better than Turkish iconoclasm

Both countries’ currencies have plunged. Only one is taking the prescribed medicine

After discussing Turkey, the article turns to Argentina:

Argentina, by contrast, has stuck much closer to convention. Its finance minister has two economics-related degrees. Its central bank has raised interest rates through the roof (lifting them to 60% on August 30th), and its government has secured prompt and generous assistance from the IMF, which agreed to a $50bn loan in June, the largest in its history. And yet Argentina’s currency has lost over 50% of its value this year (see chart 1).

Why has Argentine orthodoxy yielded such poor results?

The rest of the article is actually quite good, but I worry that this early framing will lead readers astray (as not everyone reads an entire article.)

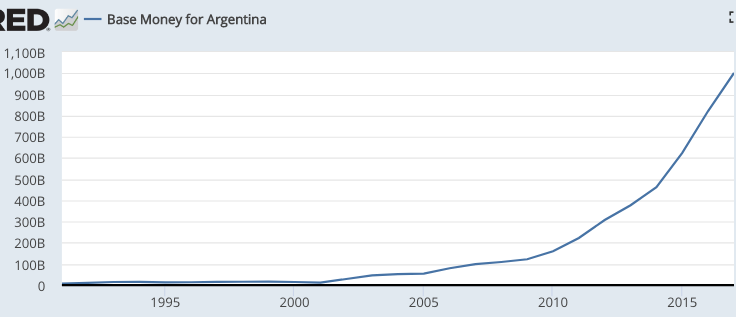

This opening might lead readers to assume that Argentina has tried a “conventional” tight money policy, and that it failed to prevent the peso from rapidly losing value. But has money actually been tight? Here’s the Argentine monetary base:

So if they’ve been printing money like crazy, then why are interest rates so high? The answer is simple—the Fisher effect. Printing money leads to higher inflation expectations, which leads to higher interest rates. As Milton Friedman pointed out back in 1997, low rates are generally a sign that money has been tight, and high rates are a sign that it has been expansionary.

So if they’ve been printing money like crazy, then why are interest rates so high? The answer is simple—the Fisher effect. Printing money leads to higher inflation expectations, which leads to higher interest rates. As Milton Friedman pointed out back in 1997, low rates are generally a sign that money has been tight, and high rates are a sign that it has been expansionary.

The article does eventually get to the underlying problems, including excessive government spending, an inability to borrow due to previous sovereign defaults, and the resort to printing money to fill the gap between taxes and spending. But I almost never see a graph for the monetary base in this type of news article, and that’s unfortunate.

There are lots of problems with 1970s-style monetarism. We now know that the money supply is not a reliable indicator of the stance of monetary policy, due to unstable velocity. But there are worse ideas than monetarism, and unfortunately one of those worse ideas (high interest rates imply tight money) has come to dominate the media.

READER COMMENTS

Mateusz Urban

Sep 14 2018 at 1:12pm

Scott,

As an economics student trained in the mainstream fashion, I have a hard time understanding the Fischer effect described above (and in your JoM article, for that matter). So let me describe the chain of causation as I see it so that you can correct me if I’m wrong.

1. Central bank “loosens” (in the relative sense) monetary policy, e.g. by printing more money, as it is the case in Argentina;

2. This, seen as permanent monetary injunction (in Cagan’s framework), raises inflation expectations;

3. Through the fisher relation this means that nominal interest rates have to rise if real interest rates (determined by real factors) are to remain the same.

Further, I am not really sure where the cb’s discretion over the nominal policy rate fits here; the fisher relation (at least as I see it) implies some automatism in the adjustment. Is the argument here that CB predicts the inflation to come and hence has to increase nominal rates to curb monetary expansion? This is I think the most confusing part – on the one hand we say that cb can print money and on the other that it can set policy rates. I will be grateful for some clarification.

Thanks!

Thomas Sewell

Sep 14 2018 at 7:40pm

Probably someone will explain it better than me, but here’s an attempt:

Consider the mechanism of the Fisher Effect to be primarily market driven, rather than CB driven.

So if the “natural” rate of interest given a particular set of circumstances is a 5% return on investment at 0% inflation, then if printing money raises inflation expectations to 3%, lenders/investors will see that change and demand 8% for their money instead in order to maintain the same 5% cost of future money. As a result of those normal market changes, we end up still with a 5% real interest rate, but an 8% (real + inflation) nominal interest rate.

Ignoring velocity, the CB printing the money is the “loose” side, which then implies higher inflation and higher nominal rates as above. If you were observing only nominal interest rates, then seeing them go higher without a corresponding reason why real interest rates went higher would obviously imply higher inflation expected and thus that someone has been increasing the monetary base. Conversely, if you see nominal interest rates dropping without a real explanation, you’d see that as an indicator of a tighter monetary policy.

The CB (generally) controls the money supply. As a result, if the CB wants to raise nominal interest rates, they can inject money into the economy and if they want to lower them, they can remove money. The CB can’t just “declare” an interest rate and make it magically so. They have to have some sort of policy mechanism to enforce/encourage it. So if instead they decide to “set” a particular nominal interest rate, to accomplish that they can use various mechanisms to commit to adding/removing money as long as their interest rate target isn’t hit yet.

So if the CB’s nominal interest rate target is lower than the current (Real INT + Inflation), they must be by the nature of things tightening the monetary base and if it’s higher than current, they must be loosening it. So in shorthand result, CB raising rates = CB tightening, while CB lowering rates = CB loosening.

Mateusz Urban

Sep 15 2018 at 11:05pm

Thomas,

Thanks for this. I think most of the confusion for me stemmed from the distinct definition of ‘money injection’ I was thinking of (that is, the indirect one through the transmission mechanism as economists call it). Then, in order to decrease interest rates the central bank would increase the quantity of base money through open market operations, increasing the supply of reserves demanded by a banking system. This, in turn, would decrease the interbank rate and, through competetive process, bring other nominal interest rates down. This is the basic texbook exposition of the monetary policy in action.

On the other hand, the use of ‘money injection’ here seems to have been more literal (printing money), which is bound to increase inflation expectations quicker than the afroementioned mechanism and consequently ‘make’ the central bank increase the rates sooner (though it still may take considerable amount of time, as Scott explained below).

Scott Sumner

Sep 14 2018 at 10:07pm

Mateusz, It is a bit confusing, as the central bank can impact both the money supply and interest rates. The path of the money supply (and demand) determines the inflation rate over time. That inflation rate then influences market equilibrium interest rates. The central bank has some ability to move interest rates a bit above or below market equilibrium rates, in the short run. But if it deviates too far, then the economy spirals into depression or hyperinflation. So as a practical matter the central bank is, over time, pretty much forced to follow along with market forces. In Turkey, the president wanted the CB to hold down interest rates, but eventually even he had to concede that was impossible as long as inflation was soaring.

So at the deepest level, money growth determines interest rates via the Fisher effect, at least in the long run.

Mateusz Urban

Sep 15 2018 at 10:53pm

Scott,

Thanks for that – the process seems much more clear now, especially while seen through the short-run/long-run lens.

Benjamin Cole

Sep 15 2018 at 6:47am

Derek Scissors, over at AEI, notes a radical decline in the expansion of the money supply in mainland China recently.

Monetary policy, even in the West, is nearly indecipherable. Perhaps there is bad news out there for China.

ChrisA

Sep 17 2018 at 1:18am

China’s monetary policy is not hard to understand, they want to keep a rough parity with the US dollar for reasons of import inflation and export sustainability. So they adjust their monetary policy to do this. So do most western countries, even though they don’t realize it explicitly. If the Euro starts to fall too much against the dollar the ECB would, because of concerns over the impact of import driven inflation, would tighten. The only countries that run independent monetary policies are the US (with commodities priced in dollars and a relative small import sector import inflation is not a big issue), or counties like Argentina where the central bank prioritizes other things other than inflation. But even in countries like Argentina any change in demand in the rest of the world will have a big impact on their economy.

This is why the Fed’s actions are so important, they think they are setting monetary policy for the US, but they are also controlling monetary policies across the entire world, including China.

Comments are closed.