Consumer prices rose 8.5% in March, slightly hotter than expected and the highest since 1981

That’s the headline on a CNBC report on April 12, 2022. Prices rising 8.5% in March? That’s really scary. I don’t blame the reporter, Jeff Cox. His first bullet gets it right:

Headline CPI in March rose by 8.5% from a year ago, the fastest annual gain since December 1981 and one-tenth of a percentage point above the estimate.

That’s somewhat scary too, but not nearly as scary as the misleading headline.

The Wall Street Journal headline writer also misled readers:

U.S. Inflation Accelerated to 8.5% in March, Hitting Four-Decade High

This is misleading in two ways. The first is similar to the way the CNBC headline misled. Inflation didn’t go to 8.5% in March. But also, inflation didn’t clearly accelerate. It rose. So the headline writer is off by one derivative.

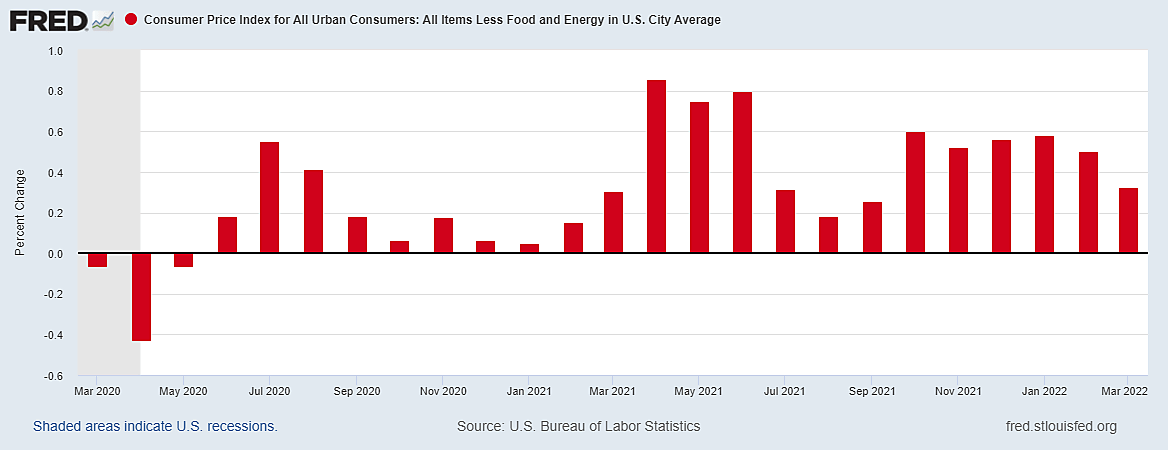

By the way, as Alan Reynolds at the Cato blog recently pointed out, the good news is that “core inflation” is less high. On April 12, he wrote:

After stripping out direct energy and food prices, the core consumer price index rose only 0.3% in March – down from 0.5% in February and 0.6% in January. The graph shows that core inflation was highest in the second quarter of last year, when it rose by 0.8% a month.

I think Alan is showing a lot of integrity here. Libertarians and conservatives are often tempted to bash Joe Biden. There’s a lot that should be bashed. But we should never overstate the case.

Of course, what matters, as Alan recognizes, is the overall inflation rate, not just core inflation. But his point, which he has made in other posts, is that there is some reason to think that energy prices won’t rise further, and might even fall from their high level, which means that the inflation rate is likely to fall. Fall, not “decelerate.”

Don’t get me–or Alan–wrong. Inflation is still too high. But my prediction a year ago that we won’t hit 10 percent in any 12-month period between May 2021 and December 2022 is looking good. I hedged it with probabilities but here’s what I wrote on May 20, 2021:

I would put an 80 percent probability on the prediction that before the end of 2022, there will be at least one twelve-month period in which the CPI has risen by at least 5 percent. I would also estimate less than a 20 percent probability that in the same time period, there will be a twelve-month period in which the inflation rate hits Carter-era 10 percent.

READER COMMENTS

Alex S.

Apr 14 2022 at 2:22pm

I’d read somewhere that the drop in used car prices was the key cause of the core CPI coming in below what was expected. While I take your point that the overall slowdown in month-to-month core inflation is a welcome development, it seems poised to be offset by rising shelter costs in the coming months. Hope I’m wrong though!

zeke5123

Apr 14 2022 at 2:44pm

I am correct to understand the 0.3% increase to be the increase from the prior month price level?

If so, a 0.3% increase in Month 1 is smaller than the same 0.3% increase in Month 2?

David Henderson

Apr 14 2022 at 3:05pm

You wrote:

For core inflation, yes.

You wrote:

No. It’s the same, unless there’s some rounding going on. I’m not sure why you asked.

Henri Hein

Apr 15 2022 at 12:45pm

If we were talking about, say, money or liquid, the first 0.3% would be smaller than the second 0.3%, since the second would be 0.3% of [starting amount]*1.003. Since we are talking about inflation, it’s not obvious (at least to us laymen) if it works like money or liquid.

David Henderson

Apr 16 2022 at 7:55pm

Ah. Now I see. Yes, compounding applies. The numbers are so small, and rounded, that it makes very little difference.

Consider the following numerical example. A number starts at 100. In one month it rises by 0.3 percent, which means it rises to 100.3. Next month it rises by 0.3 percent, which means it rises to 100.6009.

If you didn’t compound, you would conclude that it rose to 100.60. You can see how little difference compounding makes.

Moreover, what if the 0.3 percent in the second month was really 0.28 but was rounded up? Then compounding gets you to 100.58, which is less than 100.60.

Henri Hein

Apr 18 2022 at 12:55pm

I realized it was going to be small potatoes, but good point about comparing to even a small rounding.

Thanks for the explanation.

Thomas Strenge

Apr 14 2022 at 2:57pm

Expectations matter. Given the disruption in the food supply brought about by the Ukrainian conflict and avian flu, then I would expect food prices to increase substantially as well. That may actually reduce price pressures elsewhere as consumers reallocate their dollars, but that is the type of inflation care more about than heavy machinery prices.

Evan

Apr 18 2022 at 11:50am

Captain Obvious comment incoming, but it’s worth saying that: The real big picture economic consequences of inflation trends are different than the political consequences, which derive from perceptions and sentiment.

For political purposes, non-core inflation is exactly the inflation that matters the most. Regular people buy gas and groceries – often literally the same food items – every week. Without any conscious effort, then, non-experts can easily track price patterns over time in food and fuel. Also, non-core inflation disproportionally affects purchases in necessities that cannot really be delayed (in the way that discretionary purchases can be delayed). Finally, because non-core inflation consists disproportionally of necessities, it disproportionally hurts the working class and the poor, which not only angers those particular voters but also looks bad to all voters.

Capt. J Parker

Apr 21 2022 at 5:31pm

I’m totally sympathetic to there being absolutely terrible press reporting on inflation. The worst of it seems to come from a parallel universe were Irving Fisher had never been born and inflation materialized form the mysterious workings of union contracts, supply bottlenecks, oil price and boardroom filled with greedy cigar-smoking SOBs, all the while the Fed sits innocently by waiting to take credit for masterfully saving us from mess they created in the first place.

But for the particular headline above, I’m not seeing a problem. True, “inflation” is often, if imprecisely, used as a synonym for “annualized rate of inflation.” This is just about always true when you see “inflation” quantified by a percentage. So, in the context of the headline, “inflation” means a rate of change, and this rate of change increased from what it had been a month earlier, consequently “inflation” did indeed accelerate to 8.5% since “inflation” in this context is already a first derivative.

Alan Reynolds

May 4 2022 at 1:56pm

If the core PCE deflator rises at the same 0.29% monthly pace as it did in February and March, the backward-looking year-to-year percentage change will drop to 4% by June and 3.5%. War-impacted global energy and food prices get all the attention. But the Fed-engineered crash of U.S. bond and stock prices cannot reduce global commodity prices except by helping to shrink world output and income (partly by pushing the Euro and yen down). Core PCE Inflation Has Been Slowing Down | Cato at Liberty Blog

Comments are closed.