When people ask me whether QE is effective, I know I’m facing an uphill climb. The question is actually pretty meaningless–like asking whether a shovel is effective. For what purpose?

If the question refers to actual real world QE programs, then the answer is obvious. Markets responded to QE announcements as if they were having the effect of boosting NGDP expectations, but not enough to hit the central bank target.

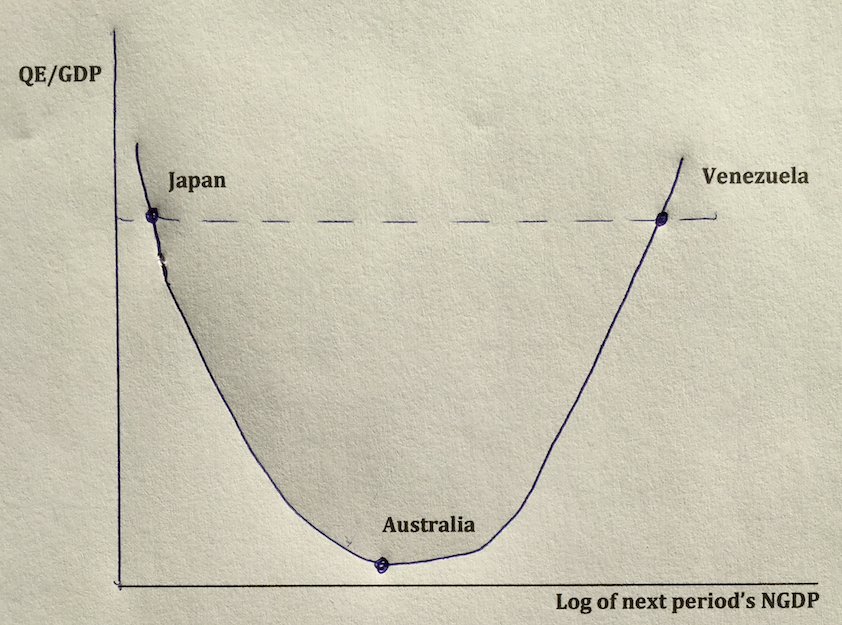

But that’s a profoundly uninteresting question. A far more interesting question to consider is whether QE can be used to achieve any specific nominal target. And the answer is clearly yes. So why is there so much confusion over this issue? The following graph might help to explain the confusion:

Under a fiat money regime, there is often an “indeterminacy problem”. That is, a particular instrument setting might have very different effects, depending on the future expected path of policy. Thus Japan and Venezuela are two countries that do lots of QE, but achieve radically different results. Why is that?

1. Venezuela is the case people have in mind when they think about the quantity theory of money. A policy of printing lots of money leads to very fast growth in NGDP, because it is expected to persist.

2. Japan is the case people have in mind when they think about liquidity traps. At very low rates of expected NGDP growth, nominal interest rates fall to zero and the demand for base money soars. To prevent the economy from falling into a depression, the central bank accommodates this extra demand for base money by injecting more money into the economy via QE programs.

Australia is a “normal country”. Growth in NGDP is high enough to keep interest rates above zero, which leads to very little demand for excess reserves. But not so high that the central bank must inject lots of money to maintain hyperinflationary NGDP growth. Thus Australia does very little QE.

Because of this indeterminacy problem, it really makes no sense to talk about the effect of QE. The same indeterminacy applies to interest rates. Ultra low interest rates might be a very tight money policy leading to the Japanese outcome (if the Fisher effect dominates) or it might be a very easy money policy that leads to the Venezuelan case (if the liquidity effect dominates.)

This indeterminacy problem helps to explain my criticism of a recent MRU video on monetary policy. In the video, Alex Tabarrok points to the extraordinary steps that the Fed took in late 2008, and suggests that in order to prevent a deep recession even greater steps would have been needed. This is like assuming that the function shown above is monotonically upward sloping. Indeed if you asked 100 economists, I’d guess that 99 would tell you that the line slopes up and to the right from the dot representing Japan. But the data suggests pretty overwhelmingly that the opposite is true, the ratio of base money to GDP declines as the NGDP growth rate increases.

Is there a solution to this indeterminacy problem? Fortunately, the answer is yes. Consider three approaches to monetary policy:

1. The quantity of money approach

2. The rental cost of money approach (i.e. interest rates)

3. The price of money approach

Only the third approach is free of the indeterminacy problem. Central banks need to target a price, and then let the market determine how much QE is needed to hit that price. You could think of the price approach to policy as drawing a vertical line on the graph above. It would only cross the QE function once, and hence there is no indeterminacy problem.

For instance, the Fed could target the price of gold, or the price of foreign exchange, or the price of CPI futures contracts. My preference is that they target the price of NGDP futures contracts. With the price approach, QE is always 100% effective. You do enough QE to insure that the market forecast of NGDP is equal to the policy target.

If you are worried about the central bank having to buy too many assets, you simply set a NGDP growth target high enough so that the demand for bank reserves is rather modest.

A Fed announcement that it plans to buy $1 trillion worth of Treasury bonds is not a “policy”, it’s a gesture. It’s meaningless to talk about the effect of this gesture, as it entirely depends on the policy regime in which it is embedded.

A shovel can be effective or ineffective, depending on how it’s used. So please don’t ask me if QE is effective.

READER COMMENTS

AntiSchiff

Dec 27 2017 at 4:23pm

Dr. Sumner,

Is it safe then to use an expectations-adjusted quantity of money theory? In other words, would QTM hold if central bank credibility were 100%?

Lorenzo from Oz

Dec 27 2017 at 8:07pm

It is truly remarkable the number of folk who do not understand that context (policy regime) matters.

Scott Sumner

Dec 28 2017 at 1:26am

Antischiff, Sorry, I don’t understand the question.

Lorenzo, That’s right.

François

Dec 28 2017 at 11:05am

A weak post from Mr. Sumner.

I fully accept his diagnosis that monetary policy in Japan has been too tight for many years. I therefore hoped that the shift in monetary policy brought about by Kuroda would be successful.

We are now 4-5 years later. For sure, there have been some improvements in the Japanese economy: unemployment is low, the economy is doing well. But the BoJ keeps missing its inflation target, and interest rates are still stuck at zero. When looking at 10Y graphs of various aspects of the Japanese economy, the impact of the 2013 monetary policy shift isn’t obvious. Often, it looks like the current positive situation is the simply a continuation of previous trends, making one wonder what is the role of monetary policy, if any.

Mr Sumner compares Japan to Venezuela. I am sorry, but this is just whataboutism. Nobody claims that Venezuela is in a liquidity trap. Therefore, everybody expects growth of the monetary base to be effective at driving NGDP growth. And it is: massive growth of monetary base generates massive NGDP growth in the form of inflation. Similarly, nobody claims that Australia is in a liquidity trap. Moderate growth of the monetary base generates moderate NGDP growth. Thanks, but there is nothing interesting about these facts.

So, once we strip Mr Sumner’s comment from the irrelevant examples of Australia and Venezuela, what is left of his argument that QE works well in Japan? Not much in my opinion. Mr Sumner hasn’t answered the key question: whether QE is always effective, or only when the economy isn’t in a liquidity trap.

AntiSchiff

Dec 28 2017 at 11:58am

Dr. Sumner,

In other words, given a ZLB situation, do you think it’s possible to be able to reasonably estimate the amount of monetary stimulus that would be required to close the output gap if the central bank had 100% credibility across the entire yield curve? Hence, it would then be possible to quantify the lack of credibility a central bank has when engaging in only moderately effective QE programs, for example.

AntiSchiff

Dec 28 2017 at 12:05pm

Francois,

You’ve touched upon the central problem with market monetarism, which is that there isn’t sufficient evidence at the ZLB to support the theory with anything like certainty. On the other hand, there isn’t sufficient evidence to support rival theories either.

The only way to begin to convincingly test MM theory is to adopt MM policies. If an NGDP target is adopted and a ZLB problem is overcome, that is at least consistent with the theory. On the other hand, if ZLB occurs/persists under NGDP targeting, then MMs can still point to possible credibility problems. It seems multiple failures of NGDP targeting or similar regimes could undermine confidence in the theory, one wonders whether it is absolutely disprovable.

Scott Sumner

Dec 28 2017 at 12:47pm

Francois, You said:

“what is left of his argument that QE works well in Japan?”

I think you missed the whole point of the post. My graph clearly shows that QE did not work well in Japan, they failed to hit their target. (Although it did boost inflation slightly above zero). So I did not in fact make an argument that QE worked well in Japan. So we agree.

Again, if you are talking about the question of “does QE work?” then you are entirely missing the point. QE is a tool, the question is what POLICY REGIME have you adopted. QE is merely a gesture.

Antischiff, You said:

“If an NGDP target is adopted and a ZLB problem is overcome, that is at least consistent with the theory.”

That’s not a good test at all. No one is claiming that switching from an inflation target to a NGDP target magically solves the “zero bound problem”, which is not a problem at all.

The MM policy is to do whatever it takes to hit your target, even if that means buying up the entire planet. That applies equally to an inflation or an NGDP target.

You said:

“if the central bank had 100% credibility across the entire yield curve”

What does that mean?

AntiSchiff

Dec 28 2017 at 1:32pm

Dr. Sumner,

In response to

‘”if the central bank had 100% credibility across the entire yield curve”

What does that mean?’

That was perhaps a clumsy way of trying to say the central bank has 100% credibility infinitely far into the future. So, in other words, markets are confident the central bank won’t scare itself with small increases in inflation and tighten policy.

AntiSchiff

Dec 28 2017 at 1:37pm

Dr. Sumner,

You replied:

‘”If an NGDP target is adopted and a ZLB problem is overcome, that is at least consistent with the theory.”

That’s not a good test at all. No one is claiming that switching from an inflation target to a NGDP target magically solves the “zero bound problem”, which is not a problem at all.

The MM policy is to do whatever it takes to hit your target, even if that means buying up the entire planet. That applies equally to an inflation or an NGDP target.’

Yes, I didn’t indicate it was a good test. I indicated such an outcome would be consistent with MM theory. NGDP targeting could fail and MM may survive. I recognize MM does not depend on NGDP targeting.

However, how to formally model a situation in which a central bank has to buy up ridiculous amounts of assets to escape the ZLB? That’s really the question in my mind. Is it just QTM with expectation effects?

François

Dec 28 2017 at 1:55pm

You formulated the question perfectly well:

“But that’s a profoundly uninteresting question. A far more interesting question to consider is whether QE can be used to achieve any specific nominal target.”

The BoJ has set a clear nominal target: achieving 2% inflation. Despite massive QE over 4-5 years, it has failed to achieve that target. I tend to conclude that QE is not always effective in achieving any specific nominal target.

As far as I am concerned, claiming that targeting a price level or a NGDP level would make QE much more effective is just a statement of faith. There isn’t any evidence to prove (or disprove) that.

AntiSchiff

Dec 28 2017 at 1:57pm

Dr. Sumner,

Let me be a little more explicit here and ask whether there can be a formal model for market monetarism that makes the theory falsifiable. What prevents market monetarists from always just claiming a central bank lacks credibility when monetary stimulus is relatively ineffective?

I certainly think market monetarists have the best arguments in favor of their perspective, and their perspective makes the most a priori sense. However, we all know that ideas that seem to make all the sense in the world sometimes fail.

Louis Woodhill

Dec 28 2017 at 4:52pm

Scott:

QE hasn’t worked in the U.S. because Treasuries and federally-guaranteed MBSs are considered by the the markets to be equivalent to cash (and, for the purpose of repo transactions, superior to bank reserves). With IOR neutralizing the money multiplier effect, all QE accomplishes is to effect a 1:1 exchange of one form of dollar liquidity (bank reserves) for another (Treasuries).

If you want to increase NGDP or inflation, you have to do something that increases total world dollar liquidity. The creation of liquidity inherently involves risk. Someone has to issue liquid liabilities against illiquid (or, at least less liquid) assets. The Fed could do this by (say) doing unsecured lending to the Eurodollar market, or they could phase out IOR and let the banks take the risk of creating dollar liquidity.

It will not matter what “target” the Fed aims for if all they do operationally is 1:1 trades of bank reserves for Treasuries, while keeping the IOR rate above the short end of the Treasury yield curve.

Scott Sumner

Dec 28 2017 at 7:11pm

Antischiff, You said:

“However, how to formally model a situation in which a central bank has to buy up ridiculous amounts of assets to escape the ZLB?”

The whole point of this post is to suggest how to model it. The amount of assets that must be bought are negatively related to the NGDP growth target. The higher the NGDP growth target, the fewer the assets (in a liquidity trap). That’s why the US bought fewer assets than Japan.

Francois, You said:

“Despite massive QE over 4-5 years”

Did you look at the graph? Did you see that the graph is U-shaped? If so, why did you say “despite massive QE” The whole point of this post is that when interest rates are near zero then QE gets larger as NGDP growth gets lower.

With all due respect I think you are completely missing the point of this post. The post is not saying, “do lots of QE and you’ll hit your target”. I’m saying that’s WRONG. Again, look at the graph, both Japan and Zimbabwe did lots of QE.

Louis, I have frequently suggested getting rid of IOR, but that’s a separate issue. How much risk is needed depends on the size of the public’s demand for base money when NGDP growth is on target. You should avoid reasoning backwards. Start with the target, then figure out the demand for base money at that target, and that tells you how much QE you need to do. Obviously without IOR it’s a lot less than today.

AntiSchiff

Dec 28 2017 at 7:58pm

Dr. Sumner,

You replied:

“The whole point of this post is to suggest how to model it. The amount of assets that must be bought are negatively related to the NGDP growth target. The higher the NGDP growth target, the fewer the assets (in a liquidity trap). That’s why the US bought fewer assets than Japan.”

Yes, you’re suggesting a qualitative model, but what about a precise quantitative one? Is it just the quantity of money theory, adjusted for expectations?

Comments are closed.