The Economist recently reviewed a biography of Herbert Hoover:

Why was it that Hoover, hitherto so talented at overcoming crises, was unable to overcome the Great Depression? Perhaps he had come to believe his own propaganda about ordinary people collectively solving problems without government aid. Or maybe the scale of the problem was too great even for someone of Hoover’s abilities. Mr Whyte does an excellent job of describing the qualities that brought Hoover his early successes–but provides too little guidance as to why, in the end, he failed his severest test.

Hoover is widely regarded as one of the most talented people ever to serve as President of the United States. He was very successful in business, and also in managing complex and difficult relief efforts in Europe (during and after WWI). He was clearly a highly skilled individual.

Elsewhere I’ve argued that people tend to overestimate the influence of the President over the economy (or anything else.) And that’s still my view. But I also think it needs to be said that to the extent that Hoover did have influence, he almost invariably got things wrong:

1. He supported inefficient farm policies.

2. He advocated much higher taxes on the rich (in 1932).

3. He signed the Smoot Hawley tariff in 1930.

4. He opposed tinkering with the gold standard (until it was too late.)

5. He was not a good leader.

There’s a big difference between being a good manager or entrepreneur, and being a good politician. Hoover may have been very good at putting together resources in order to achieve a well-understood goal, but not at all good at identifying the proper goals of government. Lots of very smart people thought that his policy views were quite sensible. But they weren’t.

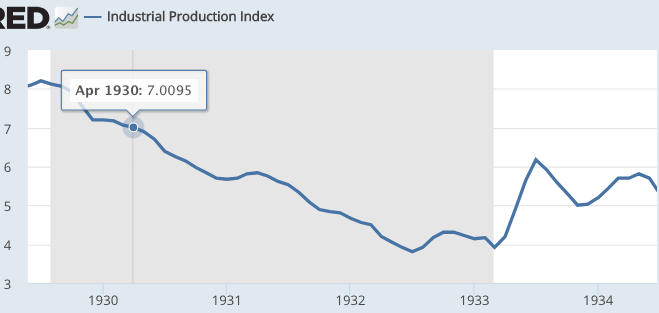

Given the fact that (under the gold standard) Presidents had only limited control over monetary policy, I view Smoot Hawley as Hoover’s biggest mistake. In the US, industrial production fell by 12.3% between July 1929 and December 1929, and then by only 2.3% between December 1929 and April 1930. Stocks rose strongly during the latter period. Thus the Depression was not yet “Great” in the early spring of 1930. Things seemed to be stabilizing a bit. So what went wrong?

During the spring of 1930, stocks fell repeatedly on news that Smoot-Hawley was progressing through Congress. In June 1930, stocks saw their biggest single day plunge of the year on the day following Hoover’s decision to sign Smoot-Hawley. (This despite the fact that Hoover was expected to sign the law—but there had been some uncertainty about this due to his reputation as being a “globalist”.) If Hoover had vetoed the bill then stocks likely would have soared dramatically higher, and an international trade war would have been avoided.

The economy did extremely poorly after the spring of 1930, with industrial production plunging by another 17.3% between May and December 1930.

Most economists don’t agree with my view of Smoot-Hawley, as the tariff itself was not all that consequential. It made the US economy a bit less efficient, but nothing even close to explaining the severity of the Great Depression. What they miss is the way that Smoot-Hawley interacted with monetary policy to produce a decline in “animal spirits” (aka NGDP growth expectations.) So yes, the Depression was primarily about bad monetary policy leading to falling aggregate demand, but Smoot-Hawley played an indirect role. There is no “monetary offset” under a gold standard.

It’s true that the gold standard has a stabilizing feature that we lack today—level targeting—but that mechanism was weakened after WWI, when central banks propped up the global price level to a position nearly 50% above pre-WWI levels. Thus there was plenty of room for prices to fall before the stabilizing properties of the gold standard kicked in.

Of course Hoover didn’t understand any of this, and why should he have? If FDR had been elected President in 1928, he might also have gone down in history as a failed president. His one successful policy (dollar depreciation) would have been politically unacceptable in 1930. And FDR’s other policies made the Depression worse. The one area where he would have clearly done better is trade; FDR probably would not have supported Smoot Hawley.

So was Hoover a victim of bad policies or bad luck? Both.

READER COMMENTS

Mark Cancellieri

Nov 16 2017 at 12:43pm

I have always found it interesting that Herbert Hoover is associated with laissez-faire policies, considering that he was very much the interventionist.

Lauren Landsburg, Econlib Ed.

Nov 16 2017 at 1:05pm

Steve Horwitz has an article on this topic in the Concise Encyclopedia of Economics: Hoover’s Economic Policies.

Mark Bahner

Nov 16 2017 at 5:18pm

It’s so easy to be a quarterback on Monday morning, but Hoover should have pressured Congress to repeal the McFadden Act of 1927, and even pressured Congress to pass legislation that would encourage single-site banks to consolidate or form partnerships, especially with banks in other states.

Big mistake: the McFadden Act of 1927

James

Nov 16 2017 at 8:00pm

“He opposed tinkering with the gold standard”

People say this kind of thing about metallic standards but they neglect to consider the totality of the consequences. Yes, there will be abnormal periods in which fiduciary media, if managed just so, can yield better results than a gold standard. But these episodes are rare. Most of the time, fiduciary media has no special benefit. A gold standard has other benefits similar to the due process protections against unwarranted search and seizure. A gold standard protects citizens from expropriation through inflation and it offers this protection all of the time.

Maybe fiduciary media really is superior to gold on average, as opposed to just during rare events, but I have yet to see anyone present evidence to this effect.

Andrew_FL

Nov 16 2017 at 10:51pm

@James-you keep using “fiduciary media” when you clearly mean “fiat money.” The Gold Standard that existed at the time of the Great Depression-more accurately the Gold Exchange Standard-and indeed even the pre-WWI Gold Standard-coexisted with fiduciary media.

Mark

Nov 16 2017 at 11:16pm

James,

You can still be expropriated (or the equivalent) under a gold standard. Anyone mining more gold reduces the value of your gold, or if the public decides it wants less gold and demand falls. You may make an ethical distinction between this and central bank-caused inflation, but the practical effect is the same.

The gold standard may perform as well as any currency system in a setting with essentially 0 economic growth, which was most of history. But that doesn’t mean much for the last 150-200 years.

James

Nov 17 2017 at 1:08am

Andrew_FL,

Yes, I mean fiat money.

Mark,

Historically, governments that have used inflation to expropriate the weath of citizens have not done so through mining for precious metals. We know the reason why. Under a fiat standard, the cost to expropriate the public is the cost of operating a printing press or, in modern times, a computer. Under a gold standard, the cost to expropriate the public is the cost of mining.

In any case, nothing in you comment provides evidence as to whether a gold standard would be better than fiat on average. Is that because you have no belief on the subject?

Mark

Nov 17 2017 at 1:59am

I think fiat money can easily perform better than the gold standard for the simple reason that the optimal money supply isn’t equal to whatever the current stock of gold is, and the demand for currency changes. It stands to reason, so should the money supply. I could understand why one might argue for 0% inflation, but even that’s better achieved through price level targeting with a fiat currency than with gold, or any commodity-based currency.

Matthew Waters

Nov 17 2017 at 2:21am

James,

History is absolutely full of such “expropriation” under any sort of gold standard.

1. With specie, where gold coins were minted, the government would shave gold down if tax revenue was not enough.

2. The gold standard, where paper currency is convertible but only partly backed by gold, can simply be left or suspended by the government.

European countries left the gold standard en masse for World War I. The currencies were all technically convertible at the same rate, but they suspended conversion and backing. The currencies were inflated to pay for the war, despite the gold standard.

If you truly think the government will expropriate, there is no mere mechanical thing like the gold standard that will fix it. A government truly set to expropriate assets will do so.

In the end, what matters is Rule of Law, property rights, due process, freedom of speech, etc. Not that these things are written on paper, but they become embedded in the government and judicial culture.

Scott Sumner

Nov 17 2017 at 7:54am

Thanks Lauren.

I agree with all three Marks.

James, I recall Hoover used a term like “tinkering”, but I probably should have used a different term. You can argue that the Depression happened because central banks in the US and France were tinkering with the gold standard, i.e. not following the rules of the game.

James

Nov 17 2017 at 8:17am

Mark,

I’m with you that fiat money *can* work better than a gold standard. But this has not happened. In the US, we have economic data and we can identify the relevant breakpoints in policy. As government gave itself increasing authority to manage the money supply there was no decrease in any of the problems that fiat money is supposed to solve but there was a lot more inflation.

Matthew,

No policy can constrain government in an absolute sense but that does not mean that such constraints offer no protection. This goes for a gold standard as it does for the stuff in the Bill of Rights. Neither will stop a government determined to violate rights but that doesn’t mean they’re of no value.

Ken

Nov 17 2017 at 8:46am

Some of the comments address the fact that inflation under a fiat money standard expropriated purchasing power from consumers.

But doesn’t deflation expropriate purchasing power from debtors, by raising the real value of their debt contract. During the years of the classic gold standard, as I recall, there was about a 1.5% year over year deflation.

It seems to me that a change in currency value, whether through inflation or deflation causes harm. It’s just a matter of which group suffers the most

Matthew Waters

Nov 17 2017 at 9:42am

James,

It’s important to think about what “expropriating” means exactly. You haven’t really defined it.

It’s obvious what a search and seizure without a warrant is, but it’s not obvious how monetary policy would “expropriate.”

By the definition of expropriate, all taxes are fundamentally expropriation. Any spending that is debt-financed will also result in expropriation eventually. These mechanisms do not involve monetary policy at all.

Congress has nearly unlimited power to spend on anything, to provide for the general welfare. Congress also has broad powers of taxation. Finally, Congress has complete control over debt issued.

The argument may go that Fiat money seigniorage has less oversight than spending and taxes. But monetary policy oversight is independent of the mechanism used.

The gold standard under the Fed, for example, only required 40% backing of notes with gold at $20.67. The rest was at the Fed’s discretion for open market purchases or loans to banks. Loans to banks were actually a far bigger tool under the gold standard than now.

Congress changed the Fed to target general inflation instead of one price (gold). The Fed is limited with its purchases and audited (yes, it is in fact heavily audited). In other words, Janet Yellen cannot just grab a bunch of $100 bills.

Sorry for the long answer. Oversight and accountability is important for any government function. A gold standard, even pure specie, can be overridden by Congress if it really wanted.

Comments are closed.