Last July, Arnold Kling made the following observations:

Tyler Cowen on Brexit, Steven Pinker, and Joseph McCarthy

Posted on July 22, 2016 by Arnold Kling

And also other topics. The link goes to a Twitter post with a video.

Judge for yourself, but to me it sounds like he is telling a PSST story. He says that, for better or worse, the UK spent the last twenty years working with a set of rules on trade in services with other European countries, and now that those rules have been cast into doubt by the Brexit vote, the British economy is in trouble. It is a very different take from that of those who think in GDP-factory terms.

Here are my thoughts on these issues:

1. Real and nominal shocks have very different effects on an economy. Real shocks tend to cause re-allocation from one sector to another, without significantly impacting the unemployment rate.

2. Real shocks may impact the long run level of real GDP, without a big impact on the business cycle. Nominal shocks strongly impact the business cycle, without significantly affecting the long run level of real GDP.

3. Brexit is a real shock that will not create a UK recession, but may well impact the long run level of real GDP.

4. The “GDP factory” model is not useful when thinking about real shocks (such as 2006-07), but is useful when thinking about nominal shocks (such as 2008-09)—which tend to influence the overall economy, not just a few sectors.

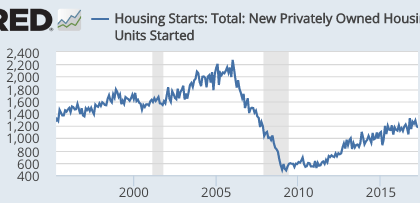

During 2006-07 there was a lot of re-allocation out of housing, without a US recession. During 2008-09 there was a significant drop in America’s nominal GDP, which had the effect of reducing real output in the “GDP factory”.

READER COMMENTS

John Hall

Jun 5 2017 at 12:30pm

So when are you gonna write a macroeconomics textbook?

Andrew_FL

Jun 5 2017 at 4:10pm

Peaks & declines in housing starts also preceded the Great Depression (peaking in 1925, but not in steep decline until 1929) the 1960 recession (peaking in 1959) the 1970 recession (peaking in 1969) the 1980 recession (peaking in 1978) the 1990 recession (peaking about 1984-86) and 2001 (peaking ca 1999)

I’m seeing a pattern hear. Hm.

The last housing trough not associated with a recession was 1966. Before that, the slump associated with WWII, for obvious reasons.

Scott Sumner

Jun 5 2017 at 10:03pm

John, I’m working on it.

Andrew, I’d guess it has something to do with housing being sensitive to interest rates, or at least more so than business investment.

If rates rise late in an expansion, housing may decline.

Colin W

Jun 6 2017 at 3:07am

Scott, I’m surprised you didn’t reiterate the point that even if the real shock is “aggregate” in some sense, its effect will be dampened by monetary policy under the appropriate regime (e.g. NGDPLT). Isn’t one of the big advantages of NGPLT over inflation targeting that it weakens rather than amplifies the real effects of aggregate supply shocks (which are more often real in nature)? This seems to be something you, George Selgin, and others have emphasized a lot.

Scott Sumner

Jun 6 2017 at 8:47am

Colin, Yes, I agree.

Alexander Hamilton

Jun 6 2017 at 9:45am

Professor Sumner, did you see this? Any thoughts?

https://www.theguardian.com/news/2017/jun/03/the-big-issue-labour-manifesto-what-economy-needs

I don’t mean the list of economists as such. It’s just a who’s that of non-economists and lecturers from UK schools with the only recognisable names being the usual heterodox quacks (Ha-Joon Chang, Keen, Galbraith etc)

Is there anything in that manifesto anyone but a total ideologue could think was good? For me when I see a list like that I think: If that’s the people they could get to sign it then 99% of the profession must think it’s garbage. Hell, even Stiglitz and Picketty aren’t on there.

Of course, Simon Wren-Lewis has signed it. There doesn’t seem to be much he doesn’t think can be solved by deficit financed “public investment” even with employment at record highs.

Scott Sumner

Jun 6 2017 at 8:37pm

Alexander, Thanks. And Dean Baker signed too?

Maurizio

Jun 7 2017 at 4:34am

“I’m working on [a macroeconomics book].”

Great news!!! 🙂

George Selgin

Jun 9 2017 at 4:21pm

” Isn’t one of the big advantages of NGPLT over inflation targeting that it weakens rather than amplifies the real effects of aggregate supply shocks (which are more often real in nature)? This seems to be something you, George Selgin, and others have emphasized a lot.”

For my part I’d merely say that NGDPLT “doesn’t amplify” the effects of real shocks, and leave it at that. The suggestion that any monetary policy can “weaken” the effects of real shocks/innovations, in the sense of somehow negating their inevitable consequences, is I think best avoided, for it leads to the interventionist fallacy of imagining that the right sort of activist monetary policy only has to kiss every (real) boo-boo to make it all better.

Comments are closed.