The Great Depression had two primary causes: an excessively tight monetary policy caused NGDP to drop in half between 1929 and early 1933, and then a set of New Deal policies such as the National Industrial Recovery Act (NIRA) slowed what would have been an extremely fast recovery after the dollar was devalued in 1933.

I’ve already talked about how reasoning from a price change contributed to the tight money policy of 1929-33. Most pundits and policymakers looked at the rapidly falling level of nominal interest rates and assumed that money was easy. In fact, rates were falling because of a decline in demand for credit, caused by the Depression itself. Money was actually very tight.

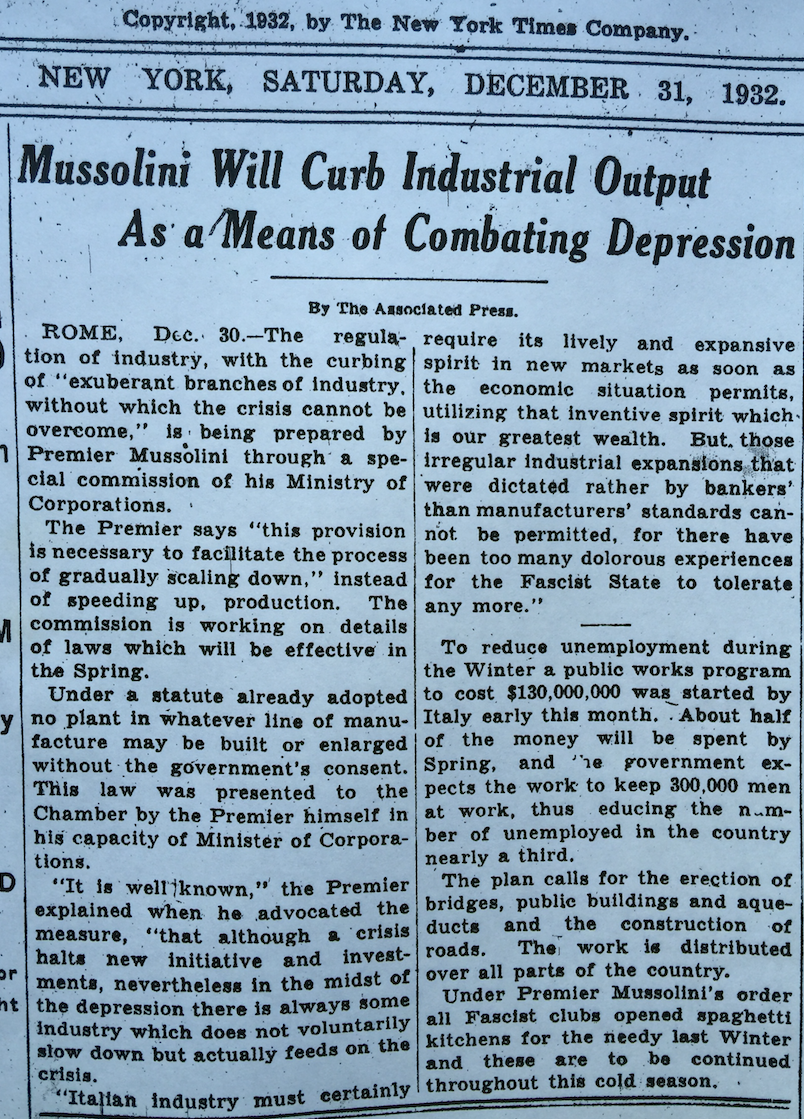

While cleaning up my office, I noticed an old NYT story that points to another type of reasoning from a price change:

You might think this is simply another example of foolish Italian public policy, which doesn’t apply to the US. In fact, this sort of policy provided one inspiration for FDR’s New Deal, and specifically the NIRA. Roosevelt believed that falling prices were the cause of the Great Depression, and set up the NIRA (and AAA) to restrict production and raise output.

I’m sure most of my readers see the problem here. Only deflation caused by falling demand could be said to have caused the Depression. A policy of boosting demand would raise both prices and output, thus contributing to recovery. However, a decrease in supply would raise prices by reducing output, making the Depression even worse.

This is not just a right wing critique of the New Deal; Keynes discussed the same problem in an open letter to FDR, published in the NYT back in December 1933:

That is my first reflection–that N.I.R.A., which is essentially Reform and probably impedes Recovery, has been put across too hastily, in the false guise of being part of the technique of Recovery. . . .

I do not mean to impugn the social justice and social expediency of the redistribution of incomes aimed at by N.I.R.A. and by the various schemes for agricultural restriction. The latter, in particular, I should strongly support in principle. But too much emphasis on the remedial value of a higher price-level as an object in itself may lead to serious misapprehension as to the part which prices can play in the technique of recovery. The stimulation of output by increasing aggregate purchasing power is the right way to get prices up; and not the other way round.

Keynes sees FDR putting the cart before the horse, trying to artificially raise prices, not have them rise as a consequence of recovery promoted by boosting demand.

[Notice that Keynes refers to “aggregate purchasing power” which is essentially NGDP. Elsewhere I’ve argued that much of the General Theory is quite “market monetarist”, with his focus on the relationship between nominal hourly wages and NGDP being quite similar to my “musical chairs model.”]

The tight money policy of 1929 was adopted to slow the stock market boom. I suppose that’s also a sort of reasoning from a price change, failing to distinguish between asset price rises caused by an overheated economy, and those reflecting good fundamentals. But I’d argue that this policy error is better described as reflecting a rejection of the efficient market hypothesis. Either way, when policymakers ignore the basic principles of economics, bad things tend to happen.

BTW, reasoning from a price change also caused the Great Recession. In addition to the well-known interest rate fallacy, the Fed and ECB were fooled by rising inflation in 2008, wrongly viewing that as evidence that monetary policy was too easy. The Fed passively tightened while the ECB actually raised rates in July 2008. In fact, the higher inflation was caused by a reduction in AS, not a rise in AD.

PS. It’s interesting how often the US adopts fads that started in Italy. When Italy elected Silvio Berlusconi in the late 1990s, I shook my head in disbelief. At the time, I couldn’t imagine American voters doing anything remotely similar.

PPS. Some people argue that the New Deal had “fascist” roots, pointing to inspiration provided by Mussolini. There’s a bit of truth in that claim, but it’s also a bit unfair—given that in the modern world the term ‘fascism’ is associated with highly repressive and racist policies adopted in places like Germany. The meaning of words evolves over time, and that accusation had more merit in 1933 than today.

PPPS, Keynes’ entire 1933 letter is quite interesting and worth reading. For instance, it makes clear that Keynes’ belief in liquidity traps was not a “myth”.

READER COMMENTS

Thomas Sewell

May 31 2017 at 10:37am

Similar logic seems to apply to some of the recent minimum wage arguments being put forth, i.e. we need to legally set labor prices higher and we’ll make up the normal negative effects of a price floor by the resulting increased spending of those wages into the economy.

Andrew_FL

May 31 2017 at 11:22am

You are imputing a rationale to the Italian policy the article does not indicate. In point of fact Rexford Tugwell was the mastermind behind the NIRA and his reasoning (and from my reading of the article, the Italians’ as well) was not about the need for inflation but a theory of general overproduction/underconsumption.

It’s important to understand the actual fallacies at work at the time, rather than viewing them through the lens of modern debates.

David R. Henderson

May 31 2017 at 11:53am

Scott,

Excellent post.

Two differences:

1. You write, “Only deflation caused by falling demand could be said to have caused the Depression.”

No. Only falling demand could be said to have caused the Depression. To the extent it caused prices to fall, that reduced the harm from falling demand. Or is your argument the one Alex Tabarrok recently made about the real burden of debt increasing due to lower prices?

2. You write, “Some people argue that the New Deal had “fascist” roots, pointing to inspiration provided by Mussolini. There’s a bit of truth in that claim, but it’s also a bit unfair—given that in the modern world the term ‘fascism’ is associated with highly repressive and racist policies adopted in places like Germany.”

Actually, most of the time I hear the words “fascism” or “fascist” used to refer to the 1930s, it’s used to refer to Mussolini, not Hitler. The usual terms for Hitler’s views and followers is “Naziism” and “Nazis.”

Mark Bahner

May 31 2017 at 12:47pm

Why would Keynes support “agricultural restriction”?

Why support the Agricultural Adjustment Act?

Brad Hunt

May 31 2017 at 9:33pm

In Reply to David Henderson’s post. Hitler’s Germany easily meets the three prong definition of fascism. In fact Nazi Germany is perhaps the most extreme example of fascism.

rtd

May 31 2017 at 10:46pm

I searched this webpage for “gold” and received no results. What gives? Or is the G.S. a part of excessively tight monetary policy in your view of the causes?

Scott Sumner

Jun 1 2017 at 9:19am

Thomas, Good point.

Andrew, As far as FDR was concerned, the rationale for the NIRA and the AAA was higher prices—he believed that reflection would promote recovery.

David, Those are both reasonable points.

1. Someone might claim that deflation caused the depression by boosting real wages.

2. On the second point, even Mussolini was much more authoritarian than FDR.

But again, I think both of your criticisms are fair.

rtd, I wrote an entire book on the role of the gold standard during the Great Depression. As far as monetary policy was concerned, the biggest problem was gold hoarding by the major central banks, which was deflationary.

Thaomas

Jun 1 2017 at 9:26am

I wonder how to quantify the relative contributions of poor monetary policy and FDR’s microeconomic mistakes like NIRA, AAA, and the 1937 attempt to reduce the deficit with tax increases, what today is called “austerity.” I’d call financing SS with a wage tax rather than a consumption tax a pretty big micro mistake, too. Specifically, if the Fed had been buying whatever it took to keep NGDP growing, how bad would NIRA, AAA and 1937 austerity have been? My own guess is that with good macro polices, the micro mistakes would have been pretty small potatoes.

A similar question could be posed about wage-price controls during WWII. How much damage did they do, even leaving aside the legacy of employer-purchased health insurance?

David R. Henderson

Jun 1 2017 at 10:08am

@Brad Hunt,

In Reply to David Henderson’s post. Hitler’s Germany easily meets the three prong definition of fascism. In fact Nazi Germany is perhaps the most extreme example of fascism.

I agree, but that doesn’t contradict my point. Hitler’s people are usually referred to as Nazis and Mussolini’s are usually referred to as fascists.

Mark Bahner

Jun 1 2017 at 12:24pm

But apparently Keynes approved of the AAA attempt to artificially raise prices on farm goods, by charging agricultural processors (making food and clothing) money, and then turning around to pay farmers not to produce. Why would an economist think that’s a good idea? Why would anyone think that was a good idea?

And this is even crazier!

richard feibel

Jun 3 2017 at 2:25pm

[Comment removed. Please consult our comment policies and check your email for explanation.–Econlib Ed.]

Comments are closed.