I just finished reading Tyler Cowen’s new book, “The Complacent Class.” Tyler is really good at bringing together lots of seemingly disparate trends and finding a common underlying theme. Many (but not all) of the anecdotes in the book will seem familiar to readers that are well read on current events, but if you are like me then you may not have noticed how they all relate to a single underlying theme. That’s Tyler’s special talent

In the final chapter Tyler looks to the future, and this is the part of the book that I found the least convincing. In this chapter, Tyler presents a sort of cyclical view of history. Before getting into the details, let’s stipulate that history is cyclical in the sense that good times are followed by bad times, where “bad times” are defined as less good times than the previous good times. Thus when bad things happen, such as 9/11, Iraq and the Great Recession, we might be justified in retrospectively labeling the 1990s as “good times.” I have no problem with that sort of claim, but it’s almost tautological.

Of course Tyler has bigger fish to fry, and extends this idea in a number of interesting directions. This is where I have some reservations.

On page 198, Tyler refers to a return of the cyclical perspective to macroeconomics. He seems particularly sympathetic to Minsky’s claim that long periods of stability lead to excessive risk taking, which sows the seeds of the next economic/financial crisis. While Tyler doesn’t make this specific argument, some people worry that a Fed policy that produces short-term stabilization might do so at the cost of bigger crises down the road.

I’m skeptical of the view that stability leads to behavior that makes the economy more unstable in the long run. If that were true, and if bankers were rational, then they would tighten up on loan standards after a long period of stability. I think we all agree that they do not do so. In my view that’s because long periods of stability do not increase the risk of future depressions, whereas my opponents would probably cite some behavioral economics research and then argue that bankers don’t become more cautious after long periods of stability because they are irrational.

The idea that history is cyclical is closely related to some similar ideas in economics and finance, such as the claim that recessions occur at regular frequencies, and the idea that the asset markets are prone to repeated cycles of bubbles and busts.

Because America has never gone more than 10 years without a recession, it seems logical to assume that the longer we go without a recession, the more likely we’ll experience one in the near future. But business cycle research doesn’t seem to back up that intuition; instead the business cycle is more like a random walk. And when we look around the world, we see other countries with economies that are similar to the US, which have gone two or more decades without a recession. (26 years for Australia.) I suppose Australia will eventually have another recession, but I don’t see any reason why it’s more likely to occur next in Australia than in America or the UK.

Because the human eye likes to impose order on random processes, a graph of the S&P500 looks sort of cyclical. But again, studies show that stock price movements are fairly random, albeit perhaps not a complete random walk. In fact, when a market has recently been less volatile, the odds are that it will continue to be less volatile than usual, at least in the near future.

[Today Tyler linked to a study that questions previous “market anomaly” studies. Some say the problem is data mining, but in a sense it’s even deeper, a lack of understanding of what “statistical significance” actually means.]

Instead of stability and complacency leading to the Great Recession, I see the real problem as being government created moral hazard and poorly thought out monetary policy. That’s not to deny that complacency plays some role; I imagine that policymakers are less likely to shift policy when it seems to have been successful. But I believe that moral hazard is much more likely to lead to excessive risk taking than stability. Why do I believe that? Because moral hazard should lead to socially excessive risk taking, whereas stability should not. To overcome that strong theoretical presumption I need hard evidence.

Tyler also considers other types of dangers, such as war. He is skeptical of sunny forecasts of “the end of history” or Steven Pinker’s claim that the planet is becoming steadily less violent. I’m a bit more sympathetic to those optimistic views, but on the other hand the exceptions are so large (for instance WWI and WWII) that it’s probably best we take Tyler’s perspective and spend more time worrying about “black swans”. I certainly won’t live long enough to see whether Pinker’s conjecture is accurate, but I might live long enough to see it refuted in the eyes of most people

Here’s an analogy. I think it’s quite possible that in 50 years, 1985 will still be seen as the beginning of a “Great Moderation” in the business cycle. I don’t see that hypothesis as having been refuted by 2007-09. But on the other hand, back in 2006 we would all have been much better off if we didn’t believe those economists who thought that the Fed had gotten a handle on the business cycle.

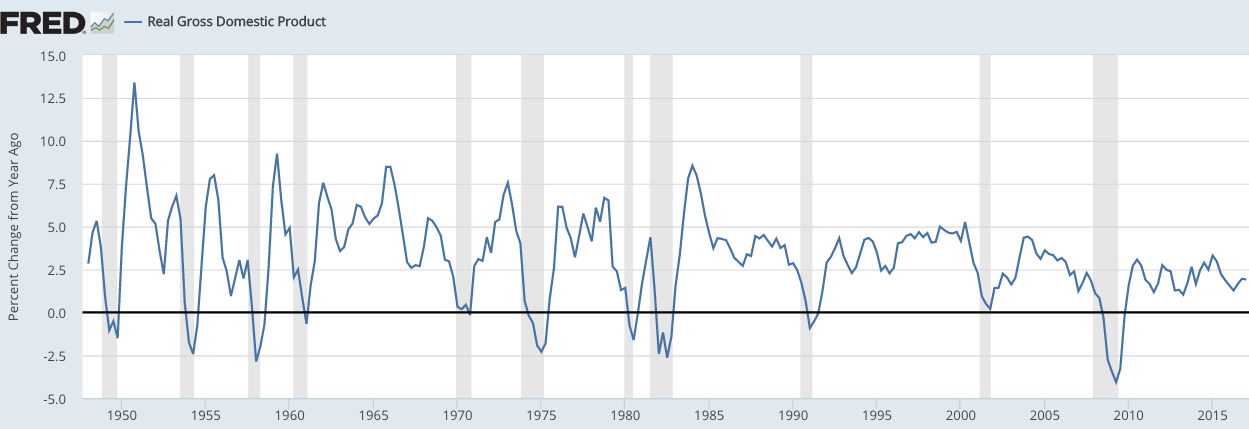

Here’s a graph of RGDP growth rates (year-over-year). Notice that since the Great Recession, RGDP growth has been even less volatile than during the 1960s expansion.

The final chapter also discusses Eric Cline’s book “1177 B.C.: The Year Civilization Collapsed“. The title sounded intriguing, so I read this book last year. Unfortunately, while it was an interesting read, the book did not really present any evidence that life in 1167 BCE was much different from life in 1187 BCE. (If you like this sort of historical speculation, I’d recommend one of Charles Pellegrino’s books instead. It may not be more accurate, but it’s more entertaining)

I’m generally skeptical of most forecasting, including the specific forecasts at the end of The Complacent Class. However Tyler probably didn’t intend that we put too much weight on any single forecast, rather that we become less complacent about whether progress was inevitable. If so, then the book will have provided a useful public service.

READER COMMENTS

Todd Kreider

May 9 2017 at 3:21am

What are the specific forecasts? Tyler Cowen said in 2009 that his “Great Stagnation” would last until the 2040s. Recently, he said there would be a “Great Reset” soon but that we will also get out of that soon as well.

Cowen doesn’t get U.S. productivity correct when being interviewed about his book. He claims that we are in a new period of low productivity when it is clear that there is nothing unusual about low periods in U.S. history. The global economy went through the worst recession since the 1930s and Total Factor Productivity fell sharply before climbing back. There was also no growth in TFP from around 1965 to 1982. When Cowen fondly reminisces about strong productivity in the 1960s, he is using labor productivity instead.

Cowen has also said there was a burst of “productivity” only in the mid 1990s but that is not true for either total factor productivity or labor productivity.

I understand why journalists can’t quickly look this up but even economist Russ Roberts didn’t question Cowen’s productivity claims yesterday.

liberty

May 9 2017 at 6:47am

“I’m skeptical of the view that stability leads to behavior that makes the economy more unstable in the long run. If that were true, and if bankers were rational, then they would tighten up on loan standards after a long period of stability. I think we all agree that they do not do so.”

This is a bit simplistic – especially considering the complexities of banking and loans these days, and in particular the fact that it is not a single person making a loan and holding on to it for decades. If it were, this might be true — self-interest would lead them to tighten up standards when they predict a crash coming. But the modern banking world is much more concerned with short-term profit, based upon the policies and interest rates of the moment — and then the loans are repackaged and sold on. So, even if a banker predicts a crash, they can still make the loan, taking advantage of whatever policy exists during the stability that might benefit them, and then repackage the loan with a bunch of others and sell it on before the crash. The person they sell it to will be interested in the price of the package of loans, and might expect that if a crash comes they might be bailed out or can rely upon their insurance… I expect that the various complications involved make your assumptions less reliable.

Michael

May 9 2017 at 6:50am

I think the claim about loan standards is stronger. It’s not that they fail to tighten standards because of an exogenous increase in riskiness, but rather that a long period of stability encourages relaxation of loan standards, which itself causes instability. There’s good evidence that this happens. And I don’t think it’s much to do with bailouts. Bailouts help creditors, primarily. Other banks are creditors, but it mainly helps depositors. Bank executives lose jobs and reputations, and shareholders generally lose their shirt. So getting rid of bailouts creates another constituency with an interest in stable banks, but the agency problem is even greater than that with shareholders – who are unable to prevent excessive risk-taking in response to stability.

bill

May 9 2017 at 8:49am

Since you mentioned Australia, I thought you’d might this an interesting tangent.

Page 292 of Age of Turbulence (Alan Greenspan – 2007). “… housing boom developed and ended in Australia a year or two ahead of the United States.”

I highlight this because I like and respect Greenspan very much, yet even someone with access to so much data can misinterpret a couple of errant squiggles. We see cycles everywhere.

Scott Sumner

May 9 2017 at 9:32am

Todd, I assumed that he was referring to labor productivity, but you’ll have to ask him.

Liberty, I don’t agree that banks are mostly concerned with short term profit. In any case, even the short term forecast should be more bearish after a long period of stability, if the Minsky hypothesis is correct.

Michael, I agree that they might weaken loan standards over time, but that may be rational, if long periods of stability make future stability more likely. Thus banks in the 1960s quite rightly forecast that financial crises would be less common over the next few decades than during the previous century.

Bill, Good find.

Effem

May 9 2017 at 10:32am

Our banking system couldn’t even handle a fairly minor monetary policy error (to use your explanation). To me that is Exhibit A that low volatility leads to fragility.

Low volatility causes private actors to add leverage and to become increasingly comfortable acting in accordance with the prevailing trends. That was/is our banking system: all doing the same things…with leverage.

Greg G

May 9 2017 at 10:33am

History is cyclical, but not in a way that allows you to make reliable predictions about future events.

I think Minsky did get it right. Stable growth rewards risky finance. Those who have made the most money in the last few years quickly become seen as those who understand the modern economy best. Leverage builds up until there is too much fragility and things crash. Then the conventional wisdom changes for a while. Economies were cyclical long before governments started adding moral hazard by trying to manage them to stabilize things.

Consider a homeowner saving for a 20% down payment in the early years of the housing boom. Every year he likely got further from his goal as housing prices rose faster than his ability to save. Meanwhile his highly leveraged neighbor was building equity. Most of what he saw in popular media told him real estate was one of the safest possible investments. How many years of that do you think it takes before most people change their mind about what is safe and what is risky, what is smart and what is dumb?

And it is not at all irrational for bankers to make loans that are risky for their banks when not making those loans is even riskier for their careers.

Todd Kreider

May 9 2017 at 12:23pm

Scott, I pointed out his description of labor productivity wasn’t correct, and he replied in comments to me that he meant TFP and that was consistent – but that is wrong as well based on what he said.

Cowen discusses TFP on p 89 but without detail or a graph from 1919 to 2015.

TFP from 1919 to 1947 is mentioned as “well over 2 percent” although a specific number would have been nice as well as actual data that he had in front of him. Then, “Later from 1948 to 1973, this measure of innovation still tended to average about 2 percent. But in 1973, TFP declined dramatically, often coming in below 1 percent a year, and for the most part, TFP growth stays low until 1995, with an average of about 0.5 percent.”

That is not what the FRED graph shows below. Instead, TFP is (net) flat from around 1967 to 1982, then steadily climbs steadily higher each year apart from the 1991/1992 recession and the 2001/2002 recession.

“The mid 1990s to early 2000s were a new golden age for TPF, which again at times ran at 2 percent or more.”

This TPF graph shows the solid gains from 1983 , and really further back except for the severe 1982/1983 recession, all the way to 2011, although there is a slowdown from 2005, a drop from the recession, and then climb up to 2011 where it stops.

(Third graph down)

http://sam-koblenski.blogspot.com/2014/07/what-limits-technological-progress.html

Scott Sumner

May 9 2017 at 4:11pm

Effem and Greg, Why didn’t banks do subprime lending in the era before FDIC?

I don’t think the problem was too much stability, it was too much moral hazard, created by FDIC and TBTF.

Todd, That’s interesting. Whenever I talk about productivity I am referring to labor productivity, not TFP. As far as I know, the slowdown after 1973, and then again after 2004, was in labor productivity growth.

Greg G

May 9 2017 at 7:26pm

Scott,

I agree that the FDIC made subprime lending more likely but so what? That is evidence for Minsky’s thesis not evidence against it.

The FDIC increased stability (and also moral hazard) and that facilitated more risky lending. This is entirely compatible with Minsky. There were plenty of booms and busts before the FDIC.

Todd Kreider

May 9 2017 at 8:03pm

Almost everyone means labor productivity when they say productivity so Cowen should be saying this in his interviews.

Labor productivity still grew strongly in 2005 at 2.1%. 2006 to 2010 had average growth of 1.94% so the productivity growth slowdown really started in 2011 not 2005. 2011 to 2016 growth was just 0.5%

The BLS shows:

(1947-1956) 2.8%

(1957-1966) 3.3%

(1967-1976) 2.3%

(1977-1986) 1.4%

(1987-1996) 1.5%,

(1997-2006) 2.8%

(2007-2016) 1.2%.

https://data.bls.gov/pdq/SurveyOutputServlet

Lauren Landsburg

May 10 2017 at 6:27am

There is also an EconTalk podcast episode with Tyler Cowen on this book this week.

Andrew_FL

May 10 2017 at 4:17pm

Empirically, manufacturing employment is more volatile than service employment, especially Durable Goods Manufacturing. This represented a much larger fraction of total employment in the 1960s than it did during the “Great Moderation.” If you take the employment data from the Establishment Survey and weight the cyclical component of each sector as describe here you can get a chart of employment growth rates weighted by the current % of total employment each sector represents. Compare this chart to your chart of RGDP growth rates. It looks like much of the differential in volatility is explained by structural changes.

Bahrum Lamehdasht

May 15 2017 at 6:26pm

I find it staggering that anyone today would even question whether stability is destabilising. Have we not seen enough financial crises arise from periods of stability? Has Minsky’s work been forgotten?

Call me a befuddled old post-Keynesian but I think the belief that stability is destabilising is cyclical. After the next global financial crisis everyone will again agree that stability is destabilising, but only until we’ve gone back to a period of stability!

Comments are closed.