Kevin Erdmann’s blog has made me much more aware of the very strange way we look at housing. Here’s an example from the Financial Times:

More than a million new apartments have sprung up across the US in a post-crisis construction surge. Now bankers who funded the boom are worried: have developers built too much?

As concerns grow about a supply glut, financial watchdogs this month began scrutinising how the largest lenders would cope with a property market crash. . . .

While a simulated property downturn has long been part of banks’ annual “stress tests”, the Fed has made CRE risks a bigger focus this year, reflecting increasing worries that bubbles are forming in parts of US real estate.

Eric Rosengren, head of the Boston Fed, last month singled out “trendy” apartment buildings in big cities, highlighting that prices had “increased sharply”. Other policymakers, including Fed chair Janet Yellen and comptroller of the currency Thomas Curry, have also made cautionary comments.

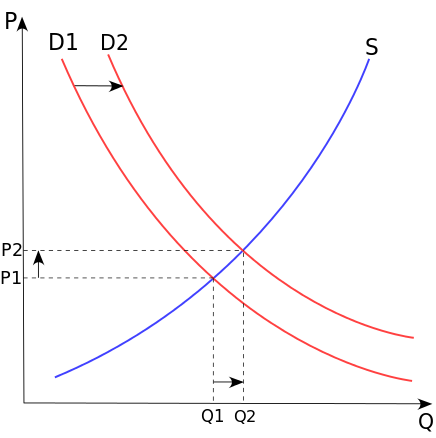

Oddly, when I studied economics we were taught that a simultaneous increase in price and quantity was an indication of a rise in demand:

The FT articles cites higher prices and higher quantity, and concludes that supply has increased. Perhaps the Fed has a more sophisticated model that has superseded the old reliable S&D workhorse.

But has quantity increased? I could not find data on multifamily units, but FRED has a graph on total housing construction:

In fact, over the past decade housing has experienced an unprecedented slump. Could the FT article be rescued if we were to focus on multifamily construction? I doubt it. Since 2008, it has become harder for people to qualify for mortgages, and thus housing demand has switched from single family to apartments. Rents have rising rapidly, especially in bigger cities. This is how markets are supposed to work after a shift in demand (put aside the question of whether regulatory changes that caused the shift are appropriate.)

When I look at the data, I see a reduction in the supply of housing causing an increase in rental prices.

To summarize:

At first glance it looked like the FT article confused supply and demand shifts, not understanding that higher prices accompanied by higher quantity implies an increase in demand, not supply.

At second glance it’s even worse, as the FT got its basic facts wrong. Housing construction has been at unusually low levels during recent the past decade. Indeed even lower than that graph implies, as the total US population is much higher than during the 1960s.

Update: Several commenters provided links to multifamily construction, which is running at about 400,000 a year. This is modestly above recent decades.

READER COMMENTS

Effem

Apr 12 2017 at 11:13am

The answer is that when people complain of a glut what they are often complaining is that an asset-price might fall from an already-lofty level. Too little construction pushes up prices, and you get some supply and prices/rents start to flatten, and then asset-owners come out in droves and complain and capital gets scared.

baconbacon

Apr 12 2017 at 11:26am

I posted some comments on Kevin’s blog a few years ago, but apparently they need reiterating.

1. Gross housing starts are meaningless. How many units were torn down to start those units alters the net gain for an economy. New housing in the Arizona desert will have a different profile from new housing in NYC.

2. Population totals are meaningless, what matters is net household formation. Population growth (which hits housing demand 20-30 years later if it is from increased birth rates and sooner if based on immigration) and average household size changing (from memory it was ~3.5 people per household in the late 60s and dropped to ~2.5 pph in the early 90s where it stabilized) are the driving forces for demand, not total population numbers.

The housing boom in the early 2000s doesn’t stand out on this graph because it is being compared to the 70s when the baby boomers were marrying and having children and divorce rates were increasing which were driving demand. Total new units to new household formation shows a different story.

Scott Sumner

Apr 12 2017 at 11:40am

Effem, Maybe it would help if people said what they mean.

Bacobacon, On your first point, that makes my argument even stronger. During recent years there has been a shift toward construction in places like New York, which implies the net gain is even smaller than the gross data suggests, and the slowdown in new house construction is even sharper.

Your second point is correct, but the recent rise in rents suggests that we are probably building too little housing (due to NImbyism), not too much.

Also recall that there is more housing depreciation in a country of 325 million people than in a country of 200 million, so it’s not clear how all these factors net out.

Garrett M

Apr 12 2017 at 12:02pm

Here’s a link to Erdmann’s blog since one wasn’t in the post

Doug E

Apr 12 2017 at 12:23pm

Besides the factual errors that Scott pointed out, the phrase “glut” is thrown around too much. Whenever a sector of the economy is in a growth phase some Malthusian enthusiast jumps up to tell the world that we all have too much of a good thing. Even when true, it is a crude analysis of deeper economic currents.

Kevin Erdmann

Apr 12 2017 at 1:36pm

Ain’t it funny how these supply gluts that are going to create a crash always start in NYC, Boston, and San Francisco? Why don’t we ever hear warnings from Fed officials about 30% drops in CRE in Atlanta or Houston? Only thing I can figure is that CRE developers in NYC, etc. just have this unbreakable tendency to create oversupply in those cities. That must be it.

In the off chance that the softness in rental markets is due to soft demand from the first shifts to a cyclical downturn – and I know that’s crazy, but bear with me – what does this tell us about the pro- or counter-cyclical nature of Fed discretionary tendencies in monetary policy?

For those who think the human tendency for herding behavior and asset bubbles requires a counter-cyclical discretionary Fed committee, wouldn’t this call for a committee of dart throwing monkeys? If we can’t get NGDP level targeting, that seems like a decent baby step in the right direction.

Jeff G.

Apr 12 2017 at 2:33pm

Scott, there might be something different going on with multifamily. If you look at total outstanding debt for multifamily (https://fred.stlouisfed.org/series/MDOTPMFR) you will see that it has increased by almost 40% since the 2008 peak. This is in contract to single family debt that is about 10% below its previous peak. I’m not saying this indicates a “glut”, just that multifamily activity appears to be different than single family.

Andrew_FL

Apr 12 2017 at 2:40pm

In the immediate aftermath of the recession you had vacant, unsold or rented inventory but probably not right now, no.

There seems to be a common pattern of government interventions running:

1. Government restricts supply, resulting in

2. Distributional and affordability problems which motivates those effected to call for

3. Redistributive and demand subsidizing policies which

4. Further increase prices which

5. Causes us to repeat the cycle from step 2.

dlr

Apr 12 2017 at 2:55pm

https://fred.stlouisfed.org/series/HOUST5F

Harry

Apr 12 2017 at 3:43pm

Zillow has data on housing prices and rents for many locations and types of residences.

The Census Bureau has data on new construction of multifamily buildings and units in multifamily buildings. Here’s a plot of new construction of multifamily units. Note that this series measures completions of new construction, while the FRED series you linked measures starts of new construction.

[Broken HTML fixed. Parameters have to be enclosed in quotation marks.–Econlib Ed.]

Scott Sumner

Apr 12 2017 at 5:57pm

Thanks Garrett, I added a link.

Andrew, Yes, that’s a common problem.

Thanks dlr, I’ll add an update

Scott Sumner

Apr 12 2017 at 5:58pm

Harry, Thanks, but I’m having trouble opening those links.

Scott Sumner

Apr 13 2017 at 10:02am

Kevin, Good points.

Jeff, Yes, multifamily has increased, but as I indicated what matters is not multifamily production, it’s total housing construction—which is still quite low. The move from single family to multifamily reflects the fact that it’s now harder to get mortgages, therefore many families that used to buy are now shifting to renting.

Overall we have low levels of housing construction and high rent levels. That doesn’t suggest a glut of supply.

Harry Chernoff

Apr 13 2017 at 1:10pm

Scott:

The multifamily oversupply issue that concerns the regulators is primarily Class A apartments in the core of Class A cities. This is the stuff that has every possible amenity and is within walking distance of everything interesting. It rents for $3-4/sqft/month or more. Too much expensive supply chasing too little (read: very upscale millennial) demand. It has little to do with NIMBY or Kevin’s Closed Access Cities and a lot to do with herd behavior among developers. Most cities are happy to have this construction because they want this demographic (though SF is becoming an exception).

Of course, the other part of this is that assuming the demand exists, it’s very profitable almost everywhere to build multifamily that rents for $3-4/sqft/month. Affordability in most cities (outside the Class A urban core) is more like $1-$1.50/sqft/month, which is below replacement cost almost everywhere. There’s no supply glut in this segment of the market. This is where rents are going up.

baconbacon

Apr 13 2017 at 3:34pm

No it doesn’t, not if you are citing Erdmann. His position is that starts have been way to low since not just 2014 or 2008, but during the housing “bubble” as well. It also was a single example not to be extrapolated from, but to highlight how different the situations could be. If you don’t actually have net starts vs the historical record you can’t state that it helps your position with an off hand remark.

Which is why you shouldn’t stake out and defend a position without looking at those numbers (note that I didn’t and I have looked at some of those numbers, using intuition is a bad idea here as the changes have been very large and there are lots of sub trends to worry about).

This is reasoning from a price change. Idiosyncratic Whisk has a ton of nice charts including ones that show the shelter component of CPI being below trend from ~2008-2012, can I conclude then that housing was overbuilt during that period?

Ken P

Apr 13 2017 at 9:06pm

Harry Chernoff, I agree with what you are saying and would add that these properties are often government subsidized via city provided low/no interest loans, gants and/or TIF. There is also an assumption that millennials will always prefer to rent not buy.

Comments are closed.