I recently argued that uncertainty over Brexit did not lead to the recession that many forecasters expected. Actually ‘argued’ is the wrong term, “pointed out” is more descriptive. But I continue to believe Brexit was a mistake, and that it will hurt the UK economy.

Tyler Cowen has a reply to my recent post on the Brexit shock:

Scott Sumner has a very good post on that question, noting that UK gdp growth has been robust and suggesting this refutes uncertainty-based theories of the business cycle. I see the matter somewhat differently, however. In standard real business cycle theory, a’la Long and Plosser, a business cycle is defined in terms of comovement and persistence. The real business cycle “victim” can either take a direct hit to wealth, or by various processes of smoothing and substitution, spread the hit out across various sectors and over time, thereby generating comovement and persistence and thus what we call a cycle. Taking the direct, concentrated hit isn’t a “cycle” but it still is very painful, in most simple versions of the model it is more painful than doing the smoothing. . . .

I think Scott is a little too distracted by not seeing cyclical action at the usual intermediate frequency.

A while ago I estimated the costs of this “hit” at 5,625 pounds per capita, though since then the British pound has fallen even further, thereby raising those costs.

Just to be clear, Tyler’s estimate of the cost of Brexit to UK consumers in no way conflicts with my post. I think Tyler misinterpreted me as saying that Brexit didn’t harm the UK (which is understandable, as the post was poorly written on that point, before I revised it.) I do think Brexit (when it happens), will reduce British GDP. So Tyler and I agree on that issue.

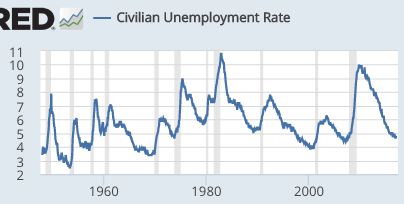

Where we may disagree a bit is the business cycle question. The meaning of the term ‘business cycle’ is fairly clear, and nothing Long and Plosser say will change that meaning. At least since Mitchell, the business cycle has referred to co-movements in many key macro variables that play out over a few years. Most economists think of a business cycle as a significant move in macro data such as unemployment and real output, seasonally adjusted, relative to trend. There’s really no question what business cycles look like, all you need to do is look at RGDP growth rates, or the unemployment rate. For instance, here is the unemployment rate for the US:

That’s what economists mean when they talk about business cycles. I encourage people to focus on the 11 recessions shown on the graph. In every case, the unemployment rate rose by at least 230 basis points. They are very easy to see, as during non-recession periods the unemployment rate never rises by more than 80 basis points. Thus macroeconomists have a very well understood concept in mind when they talk about recessions.

Now it’s true that really bad things can happen that which make a country poorer, which do not show up as recessions. One example might be protectionism. Or Ludditism. Or the 2011 earthquake/tsunami in Japan. Those things might result in a large loss in wealth without being recessions, in a technical sense.

I think Tyler missed the point of what I was trying to do with my UK Brexit post. When we have an event that everyone agrees is a recession (with rising unemployment and falling RGDP), there is often debate about the causes. In my view, tight money (falling NGDP) is usually the cause. Others often claim that real shocks were the problem, and a counterfactual where the central bank kept NGDP growing would not have prevented the recession. Instead (in their view) you would have ended up with an inflationary recession—like 1974. I believe, for instance, that this is Robert Barro’s view of the Great Recession.

If someone doesn’t like my definition of recession, I can simply rename periods of sharply higher unemployment as “bananas“. In that case, my claim is that uncertainty shocks do not cause bananas. (Those not around in the 1970s will think I’m losing my marbles.)

The British natural experiment tells us that uncertainty shocks do not cause periods of sharply rising unemployment and falling RGDP. It tells us nothing about the impact of Brexit itself, which hasn’t even happened, and doesn’t even tell us whether the UK residents are already seeing a drop in wealth due to anticipation of Brexit. Thus it’s still possible that Brexit uncertainty causes harm, just not banana-type harm.

I actually think it likely that the uncertainty does not cause much harm, but that Brexit itself will cause modest harm. The fall in the pound is certainly an indication that Brexit is expected to be a significant problem for the UK economy, as Tyler suggests.

My post wasn’t really about Brexit at all. I was using Brexit uncertainty to show that one explanation of recessions, sorry bananas, has been removed from consideration. That makes it even more likely that periods of sharply rising unemployment and falling RGDP are due to falling NGDP growth, caused by tight money. There are still a few competing real business cycles theories of “recessions” (as the term is conventionally defined), but one less theory than a year ago.

PS. Don’t underrate the importance of the very weak pound (soon to be called “ounce sterling”). Without a sharply lower pound, I would consider Tyler’s argument to be very weak. But with the pound at $1.25, I think the argument is pretty strong, at least 70-30 that Brexit will significantly reduce British GDP growth.

PPS. Tyler also said:

As for the uncertainty theories, I’m not sure the Brexit story is a good case study for them. At first I was uncertain as to whether it really would happen, but not very much any more.

In the six months after the Brexit vote, there seemed to be great uncertainty about how it would play out, hard or soft. It’s still not clear what arrangements the UK will be able to negotiate, particularly for industries such as banking. But in the end neither my view nor Tyler’s view matters. The point is that the consensus of economists thought it created great uncertainty, and the consensus of economists expected a dramatic slowdown in UK growth as a result. And they were wrong. Either economists don’t know what uncertainty looks like, or it has no cyclical effect. Either possibility is really bad for uncertainty theories of the cycle.

Here is Tyler back in July, expressing what I believe was the conventional wisdom:

I think there is a pretty simple story here. Brexit increases uncertainty, both in the mean-preserving sense, and in the “very bad outcomes are now more likely” sense, and that lowers investment. That in turns shifts back the aggregate demand and aggregate supply curves, and a recession may result. Less than a year ago, MIT economist Olivier Blanchard published a major paper on capital inflows being expansionary, and now of course we are seeing the reverse. Toss in some negative wealth effects for further transmission. I was at an event in The City a few days ago where the anecdotal data about postponed or cancelled deals seemed pretty overwhelming, and this is consistent with what one reads in the papers as well, not to mention with basic economic theory. It is true of course that we don’t know how large these effects will be, but the more purely British measures of equity value are still down quite a bit.

The uncertainty Tyler refers to did not suddenly go away after he wrote the post. Rather the UK started doing better than expected, and that created the impression that the uncertainty was being resolved. But in a policy sense the Theresa May government was very vague about its plans for quite a number of months.

The term ‘uncertainty’ must have some sort of independent meaning beyond “the economy is spiraling downwards” in order to have an important causal role. (Just as ‘bubble’ must mean more than “prices went up and then down”.)

READER COMMENTS

Thaomas

Feb 4 2017 at 10:46am

I still do not see how the failure of a banana to appear even though an exogenous shock to the “uncertainty” variable in a model can show that the value of the uncertainty parameter is zero. The model might be misspecified in any number of different ways to give that result. Very specifically, those expecting a banana after Brexit might have been using a model in which BOE would to try to prevent a fall in the exchange rate, whereas it did not. In other words the BOE’s reaction parameter was mis-specified, not the uncertainty parameter.

This looks like the non-banana after fiscal tightening in the US. There it was pretty clear that those predicting banana thought that the Fed would not offset the fiscal effect, but I believe you said the did. So again it was the misspecification of the Fed’s reaction function that was the problem with their model, not the fiscal multiplier.

Market Fiscalist

Feb 4 2017 at 10:52am

Its not clear to me why the pounds has fallen so much.

The main effect of Brexit will presumably be that some goods they sell to the EU will start to be hit by tariffs.

Some quick back-of the envelope calculations:

– International trade is about 30% of the size of UK GDP.

– Just under half of this trade is with the EU.

So (using very simplistic assumptions) about 15% of UK sales may soon start to be taxed by the EU. Even assuming quite high and universal tariffs on UK goods sold the EU I do not see this has having more than a marginal long-term effect on the overall economy. I do not see why it would represent big loses in current wealth for owners of UK assets.

And that’s before one looks at the upside:

– Maybe a good trade deal with the EU can be worked out

– Better trade deals with non-EU countries will reduce other tariffs.

– Supply-side effects of Brexit (such as being rid of a burdensome bureaucracy). These are hard to call but could easily outweigh the low marginal affects of some export sales now being taxed.

Scott Sumner

Feb 4 2017 at 2:29pm

Thaomas, If a shock can be offset by monetary policy, then it is not a real shock, it’s simply one of many factors that can cause monetary shocks.

Market, Those are good arguments, but the markets obviously believe this is a big deal. Time will tell.

Todd Kreider

Feb 4 2017 at 2:45pm

Scott wrote:

1) I don’t get this. The quarter Japan had the 3/11 earthquake, real GDP growth was -0.7 followed by -0.4 and then 0 percent growth and then a recovery with 2.9 and 2.9 percent growth.

How is three consecutive quarters of lower GDP or flat not a recession? Unemployment neither increased nor decreased but hours decreased. Not relevant for determining a recession but the Nikkei was flat for four months, dipped a bit and quickly increased. I’d say there was clearly a recession but a mild one. So does every other economist I’ve read seem to say.

2) Do you agree with Tyler Cowen when he uses a change in the pound/Euro rate to estimate some loss in wealth? Don’t you argue against using this both simplistic and inaccurate static accounting?

The pound/euro was at around 1.18 all 2013 then we are to believe that the UK got “wealthier” when it rose to around 1.40? Then again poorer when it decline to around 1.27 from Jan 1, 2016 to June 22nd, 2016 prior to the referendum? According this argument, Britain was already losing quite a bit of wealth prior to Brexit passing in June 23rd. How do we know Brexit passing was why it kept on its path to the current 1.15? Or maybe it was just half the reason, etc.

At the same time, the London stock markets rose, there were two quarters of decent growth and unemployment went slightly lower. All while the pound has hardly changed since June 22nd.

To repeat, the stock market went up after Brexit and has stayed up. So those markets are apparently favorable to Brexit or don’t seem to think it will be a burden to growth.

Andrew_FL

Feb 4 2017 at 3:49pm

I see uncertainty theories as miscast, if they attempt to explain business cycles. Uncertainty having an impact on long run growth rates makes significantly more sense.

Thomas Hutchesoon

Feb 4 2017 at 10:35pm

Scott,

Whether you call uncertainty a real or nominal shock, I suggested a way in which an increase in uncertainty in a model with all parameters correctly estimated WOULD lead to a banana, but which does not because another parameter (the central bank reaction function to an increase demand for foreign exchange) is misestimated. Therefore the UK experience does not to me necessarily indicate that uncertainty cannot cause a banana.

mico

Feb 5 2017 at 6:16am

If you think Britain will lose a lot of GDP by withdrawing from the EU, could you please estimate the GDP increase that would be experienced by the following countries if they were to join the EU:

1. Iceland

2. Canada

3. Australia

4. Japan

Do you believe they should do so if they could?

ChrisA

Feb 5 2017 at 8:28am

I think it is pretty clear why the pound fell so much after Brexit – it was the BOEs clear commitment to keep interest rates low to deal with the “shock” and in fact they did lower interest rates shortly afterwards. Of course before Brexit the BOE were on track to raise interest rates so this was a double shock to interest rate expectations. As the Fed remains on track to keep interest rates rising so the pound should fall against the dollar. Currency exchange rates seem to depend a lot on interest rate disparities (something to do with the carry trade, borrowing in one currency and invest on another).

So it isn’t as direct as Brexit caused a loss of confidence in the UK economy, which lowered the exchange rate, it was the BOEs response instead. Of course arguably the cause of the lower interest rate policy was Brexit, but I bet if the BOE had increased interest rates (say because of inflationary fears) then the pound would not have fallen and may have risen. Probably the UK would have gone into recession if that had happened so “proving” the remainers case.

As to Tyler’s argument that Brexit reduced UK wealth, I would bet that most people in the UK are net long in overseas assets (like shares) whether directly or via their pension plans. And almost no individual in the UK borrows except in the UK pound so from a point of view of anyone with overseas assets their wealth has gone up expressed in their main spending currency. People with minimal or negative assets (debt) will be neutral. In terms of the UK government, again the vast majority of its debt is in pounds, so the depreciation will have no effect on its net wealth in terms of its primary liabilities.

Jim Glass

Feb 5 2017 at 12:15pm

Where we may disagree a bit is the business cycle question. The meaning of the term ‘business cycle’ is fairly clear, and nothing Long and Plosser say will change that meaning …. Most economists think of a business cycle as a significant move in macro data such as unemployment and real output, seasonally adjusted, relative to trend…

Indeed, the NBER notably dates business cycles from peak to trough to peak…

http://www.nber.org/cycles.html

… which plainly illustrates the pretty much universal meaning of the term “business cycle”. It’s not nice to start changing definitions when the other side scores a point in a debate.

Jim Glass

Feb 5 2017 at 12:25pm

Thomas Hutchesoon wrote:

Whether you call uncertainty a real or nominal shock, I suggested a way in which an increase in uncertainty in a model with all parameters correctly estimated WOULD lead to a banana, but which does not because another parameter (the central bank reaction function…

My takeaway from the professor is: (1) The economy may suffer real shocks (such as the price of oil tripling during the 1974-81 oil crises) and monetary shocks; (2) monetary policy can offset only monetary shocks, not real shocks; thus (3) if a shock is successfully offset by monetary policy it cannot have been a real shock, QED.

Are you arguing than monetary policy can offset real shocks?

Scott Sumner

Feb 5 2017 at 2:58pm

Todd, I disagree. I think the key data series to focus on is unemployment. RGDP figures for Japan are very misleading, as they are distorted by the fact that the trend rate of RGDP growth in Japan is roughly zero. So of course there’ll be lots of negative quarters. There was only one mildly negative quarter after the earthquake, plus a few weeks of Q1.

If you look at the unemployment rate, it’s clear that the last Japanese recession was in 2008-09. Google my posts on “phony Japanese recessions”

Some of the increase in stock prices since Brexit reflects the weaker pound. UK stock indices include lots of companies with foreign earnings.

I agree that it’s misleading to simply read anything into a price change. But when we know why the price changed, then I think it is valid to draw inferences.

Thomas, I think you missed my point. If it’s real, monetary policy cannot offset it. If it’s nominal, then it’s just a cause of monetary shocks.

Mico, I never said the UK would lose a lot of GDP, and I never said it was symmetrical. Plus the UK is a bigger target for immigrants than many of those countries. I would not recommend they join the EU. I’m not sure I would have recommended the UK join, if they were not already a member.

ChrisA, That’s a common mistake. Central banks don’t just decide to cut rates. In most cases, including this one, they cut them because the Wicksellian equilibrium rate was falling. Otherwise NGDP growth would be speeding up. So no, it wasn’t the ECB, it was Brexit.

Maurizio

Feb 6 2017 at 5:14am

“I do think Brexit (when it happens), will reduce British GDP. ”

but shouldn’t the effects of brexit already be partially priced in by the markets?

maxgoedl

Feb 6 2017 at 8:02am

Isn’t there a very simple RBC explanation for the Brexit non-recession?

Suppose people foresee lower productivity in the long run, but the change won’t kick in until 2 years from now or so. People will temporarily supply more labor and produce more now and save the extra output to invest for the future in order to smooth out consumption. The real depreciation of the pound is due to the temporarily high supply of UK goods relative to foreign goods. What’s wrong with that?

Comments are closed.