Ben Bernanke is a mild mannered and modest individual. Anyone who has read his memoir will not confuse him with Donald Trump.

During the Great Recession, Bernanke suggested that it would be helpful if fiscal authorities would help to boost aggregate demand. That might seem unsurprising, but for those who have read Bernanke’s academic work, it did raise an eyebrow. Bernanke clearly thought that the Fed’s tight money policy played a major role in the Great Depression, and he was quite dismissive of claims that the Bank of Japan lacked the ammunition to end their deflation. He basically suggested that central banks had almost limitless ammo, as long as there were more assets to buy. Bernanke’s writings on the Great Depression certainly suggested that he was the sort of person who would have the Fed do “whatever it takes” to avoid another depression, even if fiscal authorities did not contribute to the stimulus.

On the other hand, being the head of a central bank is very different from being an academic, so there is no necessary contradiction. He may have privately wished to be more aggressive, but had to work within the constraints of a large and conservative institution. For instance, Fed insiders were skeptical of level targeting, an idea that Bernanke once suggested the Japanese might consider.

The example of 2013 suggests that central bankers may not know their own strength. They warned that sudden austerity might slow the recovery, but instead the recovery sped up over the course of 2013, as easier money offset the big drop in the deficit.

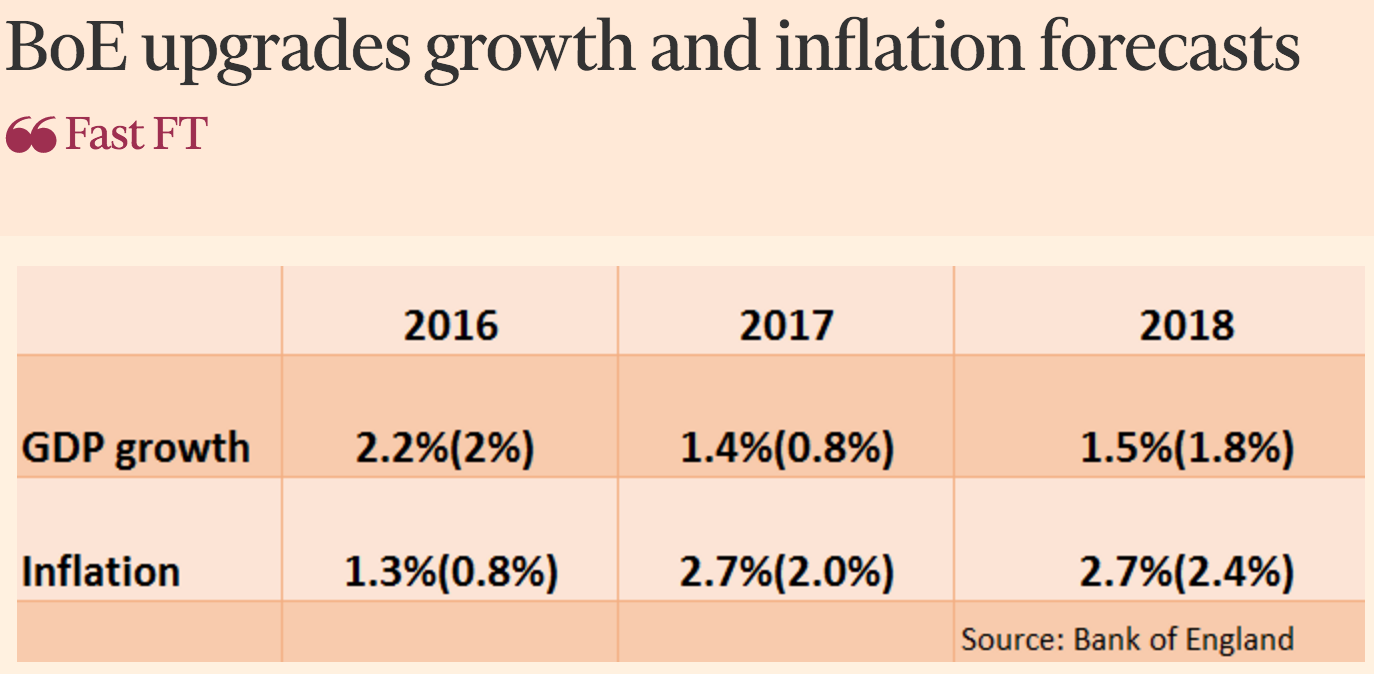

Another example occurred recently in the UK. The Bank of England warned that a Brexit vote could have a very negative impact on the UK economy, even before the actual Brexit occurred (perhaps in 2019). The idea was that uncertainty created by a “yes” vote to leave the EU might sharp reduce economic growth.

As a result the BoE eased policy, or at least did enough to prevent the Brexit shock from (effectively) tightening policy, and now the BoE is saying something to the effect, “Never mind, our prediction of gloom and doom was wrong.”

That makes them look bad. But on the other hand they deserve some credit for preventing the bad thing that they predicted would happen. Indeed central banks are supposed to prevent bad things from happening to NGDP. That’s their job. I give central banks no credit for correctly predicting a bad outcome for NGDP, just as I’d give a bus driver no credit for accurately predicting that the bus would fly over the guardrail, three curves ahead. If you think something bad will happen to NGDP, then turn the &%#@$& steering wheel!

At first glance it looks like NGDP growth will actually speed up from 3.5% to just over 4%. But that’s misleading, as the inflation figures refer to the CPI, not the GDP deflator. Normally it doesn’t make much difference, but in this case the pound has plunged sharply, so imported consumer goods will soar in price. The GDP deflator inflation rate will be significantly lower, and I think it’s likely that NGDP growth will actually slow down a little bit. Still, not a bad job by the BoE.

You may recall that BoE Governor Mark Carney had said some nice things about NGDP targeting back before moving to the BoE. That’s not his official remit, but the UK’s inflation target is flexible, and he may have had steady NGDP growth in the back of his mind, as an intermediate target during a difficult and confusing period for the UK economy.

The only downside of central bank modesty is that it leads fiscal authorities to (wrongly) believe that they have a role to play in economic stabilization. Maybe we should put Trump in charge of the Fed. 🙂

READER COMMENTS

Brian Donohue

Nov 4 2016 at 9:51am

People misunderstand the idea that central banks have great power in the same way they misunderstand that a bus driver has great power.

Like sports officials, central bankers and bus drivers are doing their job well when you don’t notice them.

Thaomas

Nov 4 2016 at 11:06am

Fiscal authorities do have a role, albeit a negative one in “stabilization.” When there is a recession and deficits soar because of automatic stabilizers, fiscal authorities should NOT behave like a Swabian hausfrau (ordinary credit constrained household), as US, UK and Eurozone countries did, by reducing spending/raising taxes. Rather they should continue (or begin, if they have not been behaving thus if there were no recession) to invest in activities with positive NPVs when benefits and costs are discounted at the borrowing rate. Since real borrowing rates are likely to fall during a recession and many of the inputs into investments will have marginal costs below their market prices (and even their market prices may fall) during a recession, this will typically imply that expenditures will rise above the automatic stabilizer levels. This will look like “fiscal stimulus” to those who oppose fiscal stimuli, but their misunderstanding should not get in the way of income maximizing investment.

How much additional investment will occur during a recession is an institutional matter depending on how quickly new investment opportunities can be identified and executed.

Scott Sumner

Nov 4 2016 at 11:19am

Brian, Good analogy.

Thaomas, That’s “reasoning from a price change”. The reason why interest rates fall during recessions is that the productivity of new investments falls. So a lower interest rate does not imply a need for a greater quantity of investment, any more than a lower price of gas means people “should” drive more.

Thaomas

Nov 4 2016 at 3:45pm

Brian,

I think you are assuming everything is in equilibrium. Why do the returns to repairing potholes or upgrading the IRS’s ancient computer systems fall during recessions unless enough investments are actually made to drive down the marginal returns?

Adam

Nov 6 2016 at 12:26am

A bus driver can not drive well without quality fuel.The central bankers and fiscal authourities also can not play in economic stablization throught tighting or easing quantity of money without a sole uniform stable value mearsure of money-the quality of economic fuel. They are making things complex by issuing paper money and debt without an sole anchor for money.

Roger McKinney

Nov 6 2016 at 7:45pm

There is a growing number of people who think central bankers are far less impressive. “Have Central Bankers “Lost the Plot?” http://www.alt-m.org/2016/11/01/have-central-bankers-lost-plot/

Craig

Nov 8 2016 at 2:30pm

Central banks are interested in maintaining market confidence in their ability, but I wonder if it is self-defeating.

Comments are closed.