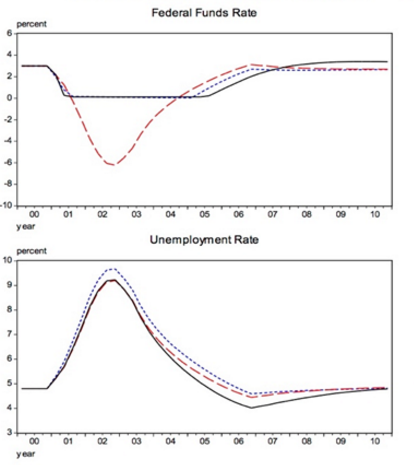

Over at Bloomberg.com, Narayana Kocherlakota has a nice post discussing the Fed’s plan for the next recession. He provides some graphs showing alternative policy paths:

Kocherlakota comments:

She [Yellen] views this black-line outcome as a demonstration that the Fed’s existing tools would be “sufficient” (to use her word) for the Fed’s purposes.

It’s worth thinking carefully about Yellen’s statement. The black line in the bottom left panel shows that the unemployment rate would remain above 5 percent for four years. The black line in the bottom right panel shows that the inflation rate would be below the Fed’s target of 2 percent for more than a decade.

Two years into this hypothetical recession, the Fed would be refusing to provide more accommodation, even though the unemployment rate would be above 9 percent and it would be expecting the inflation rate to be falling further below its target for another three years. (And as I have written, at this point in the recession, the unemployment rate among blacks would likely be above 17 percent.)

How can the Fed view these unemployment and inflation outcomes as acceptable? One answer is that the Fed can’t do any better. But inside the model used to generate Yellen’s slide, the Fed can always push down the unemployment rate and raise the inflation rate by promising to keep its target interest rate lower for longer, buying more long-term assets or both.

The inflation and unemployment outcomes depicted by Yellen represent the Fed’s desires (as modeled by its staff), not its limitations. (Indeed, elsewhere in his paper, Reifschneider depicts how the Fed could do significantly better.)

Kocherlakota is right, and indeed in some ways understates the problem with this plan.

1. Notice that the Fed anticipates that both employment and inflation will decline during the next recession. That means they expect the next recession to be caused by an adverse demand shock. And that means they expect that the cause of the next recession will be . . . the Fed itself.

2. This policy is also inconsistent with the Fed’s dual mandate. Imagine they had a single mandate, inflation targeting. In that case, they would put no weight on employment fluctuations. If you now add employment to the Fed’s mandate, then they need to have a more expansionary policy that otherwise when unemployment is high, and vice versa. But under the Fed’s plan, they actually plan to have a tighter monetary policy than what would be called for under a pure inflation target, during periods when unemployment is extremely high. This is simply perverse.

Instead, the Fed should be aiming for above trend inflation during periods of high unemployment, and vice versa. That’s not just a good idea, it’s the law.

Under nominal GDP targeting, the Fed would push inflation above 2% during recessions, and below 2% during booms. The average would still be 2%, but there would be less volatility in real output. The best way to do this is to always set policy at a level where 12 month (or perhaps 24 month) forward NGDP expectations are exactly on target.

In the graphs above, the Fed assumes that inflation is 2% before the recession, and 2% after the recession. During the recession itself, the inflation rate is considerably below 2%. But that means the average inflation rate will be below 2%, and the Fed has recently assured us that the 2% target is symmetrical; a midpoint, not a ceiling. So why produce hypothetical graphs that make it look like a ceiling?

Under NGDP targeting, inflation might run about 1.5% during a boom, and then rise to 2.5% during a recession. That sort of countercyclical inflation will tend to stabilize the labor market, and also the credit markets.

The BoE’s recent moves to ease policy have produced expectations that British inflation will rise and RGDP growth will decline in 2017. I don’t know if that will occur, but at least in terms of market expectations, the BoE is on the right track—always aim for countercyclical inflation.

The Fed often uses the Phillips Curve to forecast the economy. But the Phillips curve only works when inflation is procyclical. So the Fed uses a forecasting tool that is only useful when Fed policy is destabilizing to the economy. Thus I believe things are far worse than even Kocherlakota suggests. The Fed needs to rethink policy from the ground up.

One place to start is with their assumptions about the stance of monetary policy. Kocherlakota links to a Fed paper that included the graphs above, and also this one:

That graphs show a tight policy during 1979-81, and a very easy money policy since 2009. Back in 2003, Bernanke said the best way to ascertain the stance of monetary policy is to look at NGDP growth and inflation. I agree. By those criteria, policy was wildly expansionary during 1979-81 and very contractionary after 2009.

As long as the Fed doesn’t know where it has set the steering wheel, it’s not likely to be able to reach its preferred destination.

READER COMMENTS

MikeDC

Sep 15 2016 at 12:59pm

Why do both you and Kocherlakota state this outcome as “desired” by the Fed without venturing any guesses as to why?

You both find the outcome patently unconscionable, so it stands to reason that the smart people at the Fed have their reasons. Why?

Brian Donohue

Sep 15 2016 at 1:54pm

Good stuff.

cc: Janet Yellen

ThaomasH

Sep 15 2016 at 3:09pm

This makes sense in your policy model in which NGDP is always exactly what the Fed wants, but is is needlessly confusing to anyone else. To anyone else it makes sense that “stuff happens” that might suddenly cause businesses to want to invest less and or consumers to want to save more and the the failure of the Fed to instantly sense and offset these events would not mean that the Fed “caused” the recession.

ThaomasH

Sep 15 2016 at 3:27pm

I second MikeDC’s request for some analysis of the political economy of the policy failure you identify.

I’ve heard at least 3 reasons for Fed errors, political constraints (skittishness) about:

1) the amount of asset purchases (whether causing some intrinsic harm or fears of “financial instability”)

2) the amount of inflation above their (implicit) 2% ceiling

3) the rapidity with which ST interest rates would have to move (if inflation rates got above a 2% ceiling)

that would be required to hit their target.

Yes, we know you do not think that the amount of asset purchases/inflation/interest rate movements would be all that large if the Fed were properly targeting NGDP, but take as given that they do not think that way and try to figure out what their perceived constraints are.

Philo

Sep 15 2016 at 7:15pm

@ ThaomasH:

The Fed’s expectation for next year’s NGDP must be what the Fed wants. Otherwise they would adopt different policies that would yield the desired expectation.

Gordon

Sep 15 2016 at 7:18pm

Scott, I was wondering if you saw the latest item from Kocherlakota which came out today. I agree with both you and him that the Fed would be making a serious mistake if it followed the game plan outlined above.

But Kocherlakota is calling for a discretionary rather than a rule based policy:

https://www.brookings.edu/bpea-articles/rules-versus-discretion-a-reconsideration/

I know you’ve expressed your thoughts on this in the past. If I remember correctly you advocate flexibility to change policy regimes but that having a rule based policy to help set expectations is important. Is that correct?

Joe Leider

Sep 15 2016 at 10:18pm

Those graphs make a couple of other huge assumptions:

1) that the Fed Funds rate will be 3% by the next recession.

2) inflation will be back at the Fed’s 2% ceiling.

How likely are either of those possibilities with the Fed tightening before even reaching those targets?

Bob Murphy

Sep 15 2016 at 11:22pm

Scott,

I would like to request that when you get a chance, you devote an EconLog post to avoiding potential confusion among its readers. Here’s my concern:

==> From a 30,000-ft view, I think a lot of free market economists in 2005 would have endorsed the following: “The Keynesian economists thought the proper policy in a recession was to print money and generate (price) inflation, in order to bring down unemployment. But Friedman and others pointed out that this was quite shortsighted. Once unions and other workers adjusted to the new policy, the so-called Phillips Curve would simply shift. Then we’d have the worst of both worlds, of high unemployment and inflation. That’s why the central bank shouldn’t try to solve a recession by the printing press, but should instead focus on monetary policy rules that provide a stable framework that, in the long run, maximizes real GDP growth and minimizes volatility.”

==> So I know you know all of this stuff, and can get much more nuanced, but I’m concerned the average EconLog reader will take away the lesson from your typical posts here that: “For the last 8 years we have had tight money and that’s why the economy has been bad. The way to fix this recession is to inflate. The way to fix the next recession is to inflate. If unemployment is too high, you need more inflation to fix it.”

Again, I realize that’s not literally what you are saying, but at times it sounds like that’s the take-away message. So if you could at some talk about this, I think that would be helpful.

bill

Sep 16 2016 at 8:41am

The Fed probably will be the cause of the next recession. They never listen to market prices. They’ve been saying (with their dot plots) that they want to cause a recession. You can’t raise IOR to 3% when 10 year T’s are projected to be sub 2% and not cause a recession. I’m throwing in the towel on them making even the right tactical moves (cut IOR) let alone making a grand strategic change (NGDPLT).

Bill Woolsey

Sep 16 2016 at 9:03am

I think that the language of manipulating inflation along the business cycle is misleading.

If nominal GDP stays on target, and there is a supply side recession, then inflation will be higher. If there is a supply side boom, then inflation will be lower. The market system will tend to generate this result unless the Fed takes action to “correct” inflation.

If there is a demand side recession, then nominal GDP did not stay on target. The Fed will seek to get nominal GDP back on target, which should hasten the recovery. If there is a demand side boom, then nominal GDP did not stay on target. The Fed will seek to get it back on target, hastening the end of the boom.

baconbacon

Sep 16 2016 at 12:26pm

From what frame of reference? The trimmed mean PCE rate was > 3% during the 80s, and > 2% for most of the 90s. From 1983 (which cuts out all of the high inflation 70s and early 80s) to 2008 it was > 2% for all but roughly 4 years (the story is similar for CPI).

Over what time frame should the Fed be targeting 2% inflation? What justification is there for demanding the rate be above 2% now when it was above 2% for the previous years?

Scott Sumner

Sep 16 2016 at 5:45pm

Thaomas, Philo said what I was going to say, you need to look to see if expectations stay on track. My view is that expected future NGDP usually falls during recession.

Gordon, Thanks, I’ll take a look.

Joe, Good point.

Bob, I have done a number of posts arguing that the Fed should not try to “solve problems”. But I suppose there is always room for more.

bill, I’m agnostic on what they’ll do next time.

Bill, Good point.

baconbacon, The Fed was not targeting inflation at 2% during the 1980s, and even in the 1990s that target was only gradually adopted.

B Cole

Sep 16 2016 at 8:32pm

Great post.

The independent fiat-money Fed no longer answers to the White House. It may fear some gold-nut Congressmen. Its milieu is banking.

baconbacon

Sep 17 2016 at 10:25am

@ Scott- it is irrelevant when the announcement came, by your own standard the Fed’s actions are more important than their words. Unless the announcement came with a major shift in actual policy (that is a dramatic change in the near term like as happened under Volcker) then the announcement should be seen as clarification, not as a policy shift.

Comments are closed.