I just read Foote, Gerardi, and Willen’s subprime facts manifesto. Twice. In the process, I learned more about the subprime crisis than I learned in the last five years put together. If you’re going to read one piece on this topic, read this one. Quick version:

1. A simple model where insiders and outsiders grossly overestimated housing price appreciation elegantly explains all the key facts.

2. The competing models – especially stories that allege an “inside job” – contradict basic facts.

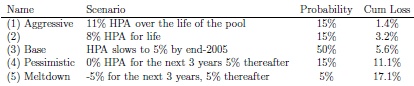

I could easily write twenty posts about this paper. The authors draw on an amazing range of evidence. For now, though, let me just direct your attention to the single most striking table. In 2005, Lehman Brothers made the following conditional forecasts about the performance of subprime-backed bonds:

Using data supplied by issuers and lenders, as well as quantitative tools designed to exploit this information efficiently, investors were able to predict with a fair degree of accuracy how mortgages and related securities would perform under various macroeconomic scenarios. Table 2, taken from a Lehman Brothers analyst report published in August 2005, shows predicted losses for a pool of subprime loans originated in the second half of 2005 under different assumptions for U.S. house prices (Mago and Shu 2005). The top three house price scenarios, which range from “base” to “aggressive,” predict losses of between 1 and 6 percent. Such losses had been typical of previous subprime deals and implied that investments even in lower-rated tranches of subprime deals would be profitable. The report also considers two adverse scenarios for house prices, one labeled “pessimistic” and the other labeled “meltdown.” These two scenarios assume near-term annualized growth in house prices of 0 and -5 percent, respectively. For those scenarios, losses are dramatically worse. The pessimistic scenario generates an 11.1 percent loss while the meltdown scenario generates a 17.1 percent loss…

Lehman analysts were not alone in understanding the strong relationship between house prices and losses on subprime loans. As Gerardi et al. (2008) show, analysts at other banks reached similar conclusions and were similarly accurate in their forecasts conditional on house price appreciation outcomes. (footnotes omitted)

The authors remark:

The analysis underscores investors’ knowledge about the sensitivity of subprime loans to adverse movements in housing prices, and it refutes the idea that investors did not or could not determine how risky these loans were.

[…]

Despite its foreboding name, the “meltdown” scenario was actually optimistic with respect to the observed fall in housing prices that began in 2006. The current forecast for losses on deals in the ABX 2006-1 index, which largely contains loans originated in the second half of 2005, is about 22 percent (Jozoff et al. 2012). This is consistent with the relationship between losses and house prices implied by the table. The bottom line is that analysts working in real time had little trouble figuring out how much subprime investors would lose if house prices fell.

If the conditional forecasts were so prescient, why were unconditional forecasts so ridiculous?

The answer to why investors purchased subprime securities is contained in the third column of the same Lehman analysis cited above, which lists the probabilities that were assigned to each of the various house price scenarios. It indicates that the adverse price scenarios received very little weight. In particular, the meltdown scenario–the only scenario generating losses that threatened repayment of any AAA-rated tranche–was assigned only a 5 percent probability. The more benign pessimistic scenario received only a 15 percent probability. By contrast, the top two price scenarios, each of which assumes at least 8 percent annual growth in house prices over the next several years, receive probabilities that sum to 30 percent. In other words, the authors of the Lehman report were bullish about subprime investments not because they believed that borrowers had some “moral obligation” to repay mortgages, or because they didn’t realize that the lenders had not fully verified borrower incomes. The authors were not concerned about losses because they thought that house prices would continue to rise, and that steady increases in the value of the collateral backing the loans would cover any losses generated by borrowers who would not or could not repay.

The hardest question is simply why such optimism arose in the first place. It contradicted all historical experience:

Relative to historical experience, even the baseline forecast was optimistic, while the two stronger scenarios were almost euphoric. A widely circulated calculation by Shiller (2005) showed that real house price appreciation over the period from 1890 to 2004 was less than 1 percent per year. A cursory look at the FHFA national price index gives slightly higher real house price appreciation–more than 1 percent–from 1975 to 2000, but still offers nothing to justify 5 percent nominal annual price appreciation, let alone 8 or 11 percent.

As far as I remember, I neglected to blog any housing price forecast when prices were rising. But the forecast I shared with friends from 2005 on was always “Prices have plateaued.” Relative to the facts, I was clearly optimistic. But I was more pessimistic than Lehman’s Meltdown Scenario! If I’d only understood the implications of my bearish housing price forecast, I would have made a lot of money from the crisis. Oh well.

Many will look at the Lehman forecasts and confidently declare, “What fools they were.” My reaction, though, is bewilderment. How can experts nail the hard question of “What will happen to our investments given housing prices?” yet botch the easy question of “Will unprecedented increases in nominal housing prices continue indefinitely?” I wish I knew.

READER COMMENTS

MG

May 24 2013 at 11:43am

Great post. “Why Did So Many People Make So Many Ex Post Bad Decisions? The Causes of the Foreclosure Crisis”, a June 2012 paper from Fed Bank of Boston should also be required reading.

The insider-outsider theories (myths that are part of a broader narrative) are covered under “Facts” 10 and 11.

http://www.bostonfed.org/economic/ppdp/2012/ppdp1202.htm

Eric Falkenstein

May 24 2013 at 11:49am

I don’t think you would have made money if prices would have plateaued, as opposed to what they actually did, which was falling 22%.

There’s an interesting, lengthy report from a 2005 Fed meeting that presents the ‘non-bearish’ housing case in real time, and it’s pretty good. Remember, even housing bear Bob Shiller could only muster a plateau forecast for ‘some areas’ back in 2005, which isn’t really that bearish, and certainly wouldn’t have motivated a short position.

Brian

May 24 2013 at 12:32pm

MG,

The Boston Fed paper you reference is the one Bryan Caplan is blogging about. It’s by Foote (Boston Fed), Gerardi (Atlanta Fed), and Willen (Boston Fed).

Brian

May 24 2013 at 12:44pm

How do you think you would have done that?

Michael Lewis’s The Big Short is about the gyrations, politics, and difficulties that faced traders in housing markets. Many people did see the collapse coming want to go short housing, but there’s no obvious way to do it. Otherwise, it’s unlikely the bubble would have been as long and destructive as it was.

Even those like Paulson who did make money going short did not do so in a predictable of sustainable way. Buying naked credit default swaps is obviously foolhardy. You’re betting that banks that have written disastrous bankrupting loans will still be able to pay you back if they fail and your insurance kicks in. Only the bailout — that half-baked nationalization of the whole banking industry — managed ironically to deliver huge profits to the few who were working to end the bubble by selling it short.

So one of the things sustaining the bubble is the structural difficulty in going against it at scale. Maybe you would have personally made a lot of money by renting and only buying your family home after the crash, but we’re talking about tens of thousands. It needs to be tens of billions to create a market force for bubble popping.

ed

May 24 2013 at 1:38pm

Yes, shorting the housing market was hard.

When Mark Kleiman wanted to short the housing market in 2005, the best way he could think of to do it was to actually move out of his house and rent!

http://www.samefacts.com/2005/05/macroeconomic-policy/speculative-selling-in-the-la-housing-market/

Michael

May 24 2013 at 2:18pm

That’s an easy question to answer! Because they were making lots of money! An honest assessment of future HPA probabilities would have looked like this:

Optimistic: 0% HPA for the next 3 years, 5% thereafter.

Base: -5% HPA for the next 3 years, 4% thereafter.

Pessimistic: -10% HPA for the next 3 years, flat for 3 years, 4% thereafter.

Had they been this realistic, the loss probability would have been too high and their very lucrative business would have ended. As they say, it’s very difficult to get a man to understand something when his livelihood depends on him not understanding it.

BTW, if you still want an opportunity to make money from a bursting bubble, the Canadian housing bust is just starting.

DougT

May 24 2013 at 2:38pm

Two words: recency bias.

MG

May 24 2013 at 2:38pm

Brian,

Thanks. Did not even notice. No wonder the findings/examples Bryan Caplan cited sounded..so familiar. The paper addresses a few other myths, and it is indeed required reading, and in my case, re-reading.

Steve Sailer

May 24 2013 at 3:11pm

Here’s what Bryan wrote on the topic of Los Angeles real estate prices in January 2007, the month before the foundering of New Century Financial, the first subprime domino to topple:

I just got back from another vacation in Los Angeles. As they say, it’s a “city of contrasts,” but the most interesting contrast is rarely mentioned. On the one hand, even pretty ordinary Angelenos – especially the elderly – reside in homes worth about a million dollars. On the other hand, the people of L.A. – and its self-absorbed local media – never stop complaining about how bad they’ve got it. Any resident I talked to for more than five minutes starting ranting about crime, gangs, natural disasters, health care, and, above all, “illegals.” And these same issues dominate every newscast and the front page of every newspaper. Los Angeles media make the New York Times look like the Julian Simon Sentinel.

Unfortunately, vacation is so exhausting that I didn’t have the energy to set L.A. straight. But now that I’m home, here’s what I’d like to have said:

Angelenos: Turn off the news. Cancel your newspaper subscriptions. If you want to really understand your city, all you need to do is take a look at housing prices. If your house is worth a million dollars, then life in your neighborhood is excellent, and will continue to be excellent for a long time. The problems you keep complaining about are minor drawbacks for people who live in cheaper areas. If your home is worth a million dollars, these problems barely affect you at all.

What makes me so sure? People don’t pay a million dollars to live in a hellhole. They don’t pay a million dollars to live somewhere that is going to be a hellhole in ten years. If popular opinion and local media imply otherwise, they’re wrong. In fact, they’re so wrong that they don’t deserve your time. …

http://www.econlib.org/archives/2007/01/million_dollar.html

Tom West

May 24 2013 at 3:23pm

The hardest question is simply why such optimism arose in the first place.

Well, I wasn’t paying as close attention to the housing crisis, but I do know that every single analyst or newspaper columnist that I read closely that was predicting the tech bubble collapse was let go (or stopped publishing where I saw them) before the collapse actually came.

Simply put, missing out on big gains that are occurring around you is far more deleterious to your career than being among the masses when the boom is lowered.

Not that I believe most people actively believed one thing and said another, but it’s pretty hard to believe something that will either make you immoral or get you fired (depending on whether you keep quiet or speak out about it).

Following the optimistic herd is generally the safest course of action for both career and personal happiness.

Ricardo A

May 24 2013 at 3:29pm

“The analysis underscores investors’ knowledge about the sensitivity of subprime loans to adverse movements in housing prices, and it refutes the idea that investors did not or could not determine how risky these loans were.”

I’m not sure this is true. That subprime loans are affected by housing prices is an obvious point. It doesn’t really refute anything. The table not only gets the magnitude of, say, the meltdown scenario wrong, but I think it really understates the likelihood of it happening (sure, in hindsight this seems obvious, but still).

To sum up: 1) they thought that the effect of a downturn was going to be a lot smaller than it was; 2) they thought the chances of a downturn were a lot smaller than they were.

And somehow this proves that investors really, really understood what they were doing…

guthrie

May 24 2013 at 4:22pm

@Steve,

I’m confused. What is the insight in your comment? What do Bryan’s words in that post have to do with this one?

Mike Rulle

May 24 2013 at 6:07pm

“1. A simple model where insiders and outsiders grossly overestimated housing price appreciation elegantly explains all the key facts.”

Isn’t this a tautology?

I still believe this was a financial crash predominantly, but not exclusively—although semantics can get tricky.

My take then and now——1)When looking at 20, 30 or 40 year real price appreciation in houses, the inflation adjusted appreciation was always about 1%, yet we did not have a crash that realized itself until 2008. Real housing prices cannot be the sole reason. It was primarily a financial bubble and crash. The “banks”—or the intermediators—caused the financial crash; then the Government fire bombed the financial sector to fix the problem.

2)It is impossible to accurately analyze what happened without focusing primarily on the role California and the Southwest played in the bubble. Their capital housing stock rose then declined in value at an extremely disproportionate rate relative to their population compared to the rest of the country. So, I do agree that real house prices, which doubled in California in 5 years between 2000-2005 (and are now back to 2004 levels), was a major contributor. But the purchase of houses was not the problem—-it was the refinancing in 2005-2006.

3)Refinancings dominated the securitization mortgage pools relative to new purchases at a rate of about 8-1, including California—-thus creating new securitization supply at an unprecedented rate. The refinancing peaked at the price peak years of 04-06. That is, it was a “mark to market” bubble by refinancing lenders more than by housing buyers. This led to exorbitant supply which hit a wall on distribution in June 2007, 15 months before the official “crash”. Underwriters jammed the market until there were no more buyers. With refinanced mortgages.

4)The “super senior” notes/CDS of the SPVs thus gradually became wildly discounted beyond all reason over the next 15 months because of massive over supply. This was the real crash—much more so than houses when risk adjusted. Evidence of this, is the AIG marks on their super “senior notes” CDS caused the bailout crisis—because of margin calls owed to “the street”. Yet, 2 years later, the Fed admitted they had yet to have one default on the AIG CDS super seniors. I doubt they have had any since of any significance.

5)The “housing” crash led to the belief that securitization per se was a faulty mechanism. The primary financing vehicle for housing disappeared overnight and has not returned.

6)Banks were demonized and stopped making loans and Fannie and Freddie have become the mortgage market. The “Post Office” now runs the mortgage market.

7)I do not know how this can be reversed. The bail out created the current market. The bailout is a permanent feature—or so it seems. The housing crisis is not over because it is a de-facto government financed business from soup to nuts. Compare how the 1907 and 1998 financial crises were handled versus the 2008 crisis. The Bull in the china shop is now in charge.

Obviously I think all bailout activity was a mistake.

Doug

May 24 2013 at 7:03pm

Mike Rulle is on the right track about it primarily being a financial market issue vs. a housing market failure.

House prices did fall, but the structured products derivatives on the housing pools fell much further. In August 2007 senior tranche CDOs traded down to 30 cents on the dollar and liquidity in these markets froze.

Needless to say overall home prices didn’t fall by 70% (in fact they’d need to fall even more since the senior tranches have credit support). After a few years many of these CDOs realize at 85 cents on the dollar or more. Which is why in the past few years mortgage hedge funds have averaged huge returns.

If the CDOs would have reflected the underlying home values the banks would have taken losses but you wouldn’t have seen the major failures of Bear, Lehman and others.

Jed Trott

May 24 2013 at 9:14pm

It interesting how the probabilities are all round numbers. This would suggest to me that nobody was actually taking these numbers seriously. That sort of analysis was all mumbo-jumbo anyway because they had no idea what the scenarios should have been or what the probabilities they should have assigned to them were but the way they constructed them makes me think that they didn’t care much about this analysis either. I would suggest that the reason for this is that they didn’t fear the downside because they didn’t have to.

Jamie_NYC

May 24 2013 at 9:36pm

I can tell you how: it is nominal prices that matter for borrowers’ ability to pay, not real prices. Nominal nationwide housing prices have never declined, since Great Depression (and then only, presumably, because of decline in general price level). So, what probability would you assign to something that has never happened before, and besides has quite unpleasant implications? Where’s your evidence?

perfectlyGoodInk

May 25 2013 at 1:46am

How can experts nail the hard question of “What will happen to our investments given housing prices?” yet botch the easy question of “Will unprecedented increases in nominal housing prices continue indefinitely?”

When people’s expectations are affected by expectations of others, you get positive feedback loops, something that both adaptive and rational expectations both ignore completely.

ThomasH

May 25 2013 at 9:36am

“A simple model where insiders and outsiders grossly overestimated housing price appreciation elegantly explains all the key facts.”

This is the conventional wisdom (which I accept). The policy question is were there regulatory changes (higher capital requirements for “too big to fail” banks?) or monetary policies (ngdp targeting?) or tax policies (partial credits rather than deductions for home mortgage interest?) that could have prevented these private mistakes from having macroeconomic consequences?

perfectlyGoodInk

May 25 2013 at 3:37pm

Foote et al tells a good story, but it’s not the whole story. Most research I’ve seen argues that the originate-to-distribute model increases the amount of information asymmetry between borrower and lender. Foote et al’s main argument against this is Fact 7, that MBS investors were provided a lot of information. It does not address the quality of that information.

Note the finding of Keys et al (2010), “Did Securitization Lead to Lax Screening? Evidence from Subprime Loans” where they noted that 1) a FICO score of 620 seemed to be the cutoff of when loans were securitized and 2) loans to applicants just above 620 performed worse than to those just below 620.

Mian & Sufi (2009), Dell’Ariccia et al (2008), and Purnanandam (2009) also have empirical results that point to securitization. Foote et al do not really argue against the asymmetrical information explanation, and are mostly talking about *where* the asymmetry occurs: “the information and incentive problems giving rise to the crisis would not have existed between mortgage industry insiders and outsiders, as the inside job story suggests. Rather, these problems would have existed between different floors of the same Wall Street firm.”

They are also not arguing that securitization played no role: “we are sympathetic to the idea that securitization had some role in the financial crisis. Securitization cut out the middleman and allowed a direct link between borrowers and investors.” The main point is to argue against the CRA’s role (Fact 4: Government policy toward the mortgage market did not change much from 1990 to 2005) and to argue that irrational optimism was the most important factor.

Or in other words, there was a housing bubble. Well, duh. I think the only people who deny the bubble are economists who don’t realize that they’re working in a social science. Oh wait, I suppose that’s all economists who believe in rational or adaptive expectations.

Patri Friedman

May 27 2013 at 4:58pm

I totally disagree about which is the hard questions and which is easy. The conditional probabilities are simple modeling exercises. More complex than Black-Scholes, but of the same order problem. It’s like asking what the profit on buying a stock now & selling it in 10 years if you know the next 10 years of dividends. Sure, you don’t know exactly what the stock price will be in 10 years, you have to guess the P/E at that point, but you do know the dividend profits and those tell you the exact value of the first 10 years of dividends, and help you estimate the sale value decently.

Whereas figuring out what housing prices will do is more like asking the price trajectory for the whole stock market in the next 10 years – knowing nothing about the next 10 years of market dividends. It depends on unknown information which is fundamentally difficult to predict (the exact changes in the global & national economy, inflation that determines the nominal price changes, productivity gains, etc…)

It seems so clear to me that the former problem is so much easier that I’m amazed you switched them. It’s like the difference between predicting how much someone will save given their next 10 years of income vs. predicting their income for the next 10 years. Or predicting how much money a gold mine will make based on the next 10 years of gold prices vs. what those prices will be. Etc.

Comments are closed.