Adam Tooze has a post discussing the bond vigilante theory:

The phrase “bond vigilante” is normally attributed to Ed Yardeni a Wall Street economist who coined it in the 1980s to describe the role of bond markets in disciplining governments.

“Bond Investors Are The Economy’s Bond Vigilantes”, Yardeni once declared. “So if the fiscal and monetary authorities won’t regulate the economy, the bond investors will. The economy will be run by vigilantes in the credit markets.” As Yardeni later spelled out: “By vigilantes, I mean investors who watch over policies to determine whether they are good or bad for bond investors … If the government enacts policies that seem likely to reignite inflation”, Yardeni elaborated, “the vigilantes can step in to restore law and order to the markets and the economy.”

This is an example of reasoning from a price change. If bond traders fear that government policies are likely to lead to higher inflation, this may result in higher interest rates (via the Fisher effect.) But higher interest rates due to the Fisher effect are not a contractionary policy. In order to prevent the inflation from occurring, the government must stop engaging in inflationary policies. Bond vigilantes won’t solve the problem.

Tooze discusses the 1994 bear market for bonds, an example often cited by proponents of the bond vigilante theory:

Furthermore, 1994 was not a spontaneous bond market attack. It too was triggered by the Fed.

In the summer of 1993 Alan Greenspan had become worried about the acceleration of inflation. Even though the Clinton administration in August 1993 had forced through the fiscal consolidation plan that would return the US Federal government to surplus, Greenspan wanted to add further dampening pressure. He was convinced that allowing for inflation expectations real interests rates had fallen to zero.

Tooze is appropriately skeptical of the bond vigilante theory, but is also reasoning from a price change. Tooze assumes the rate increase was caused by the Fed, presumably a contractionary monetary policy by the Fed. I see no evidence for this claim.

Here it will be helpful to revisit an analogy I often use. A bus drives from Denver to Salt Lake City. What determines the path of the bus? Is the path determined by the way the driver adjusts the steering wheel, or by the layout of the highway (combined with an assumption that the driver prefers to avoid going off the road?) In this analogy, the bus driver is the Fed and the road is the natural rate of interest under a 2% inflation target.

Here language fails us. It’s not clear what people mean when they ask what “determines” the path of the bus. The driver or the road?

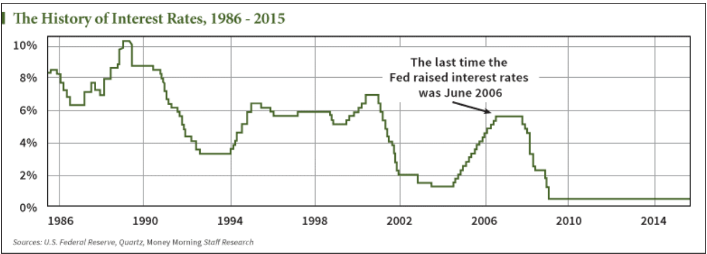

Tooze provides this helpful graph of short-term interest rates:

Why did interest rates rise during 1994? One could argue that the increase was caused by the Fed’s decision to raise its short-term rate target. Or one could argue that the Fed raised its target rate because the natural rate of interest rose as the economy strengthened in the mid-1990s, and they had to raise rates to keep inflation close to 2%. I find the latter explanation more useful.

If someone asked me to explain why I drove though Green River on my way from Denver to Salt Lake City, I would not explain this fact by referring to how I turned the steering wheel left and right at various times, I’d refer to the layout of I-70. I’d assume the listener understood that I tried to stay on the road.

But that view is not always adequate. If I plunged off the road and fell into a deep canyon, I would not explain that fact by pointing to the map, I’d point to my incompetence as a driver. If I wanted to explain why the US end up with 13% inflation in 1980, I would not assume that actual short-term interest rates always followed the path of the natural rate of interest, rather I’d assume they were mistakenly held below the natural rate during the late 1970s.

The 1990s were a successful period for monetary policy, and thus it’s enough to point to the map—movements in the natural rate of interest. We can infer from stable 2% inflation that the actual interest rate stayed pretty close to the natural interest rate during the 1990s.

HT: Matt Yglesias

READER COMMENTS

John Hall

Mar 1 2021 at 2:07pm

Scott, you write

“This is an example of reasoning from a price change. If bond traders fear that government policies are likely to lead to higher inflation, this may result in higher interest rates (via the Fisher effect.) But higher interest rates due to the Fisher effect are not a contractionary policy. In order to prevent the inflation from occurring, the government must stop engaging in inflationary policies. Bond vigilantes won’t solve the problem.”

I’m not sure how well you are characterizing the bond vigilante view here (though I am too young to have been one at the time). My guess is that Yardeni could respond that bond investors didn’t just sell off bonds due to higher expected inflation, they sold even more than that. In other words, you make it sound like real interest rates were constant, but they increased (I used 10 year yields minus 10 year Cleveland Fed inflation expectations and found a peak in November 1994, before turning over, the Fed kept tightening rates until 1995). This contributed to higher real borrowing costs for the federal government, at least temporarily (real rates were in a downtrend over this entire history).

Scott Sumner

Mar 1 2021 at 7:37pm

It doesn’t matter. If real interest rates rose because of expectations of stronger economic growth I’d say the same thing. NGDP growth was pretty stable during the 1990s, so the Fed was responding to shifts in the equilibrium interest rate.

Zach

Mar 1 2021 at 3:46pm

Any particular back story related to your reference to Green River? Seems oddly specific.

Scott Sumner

Mar 1 2021 at 7:38pm

I just looked on the map and picked a random town. I’ve never even been to SLC or Green River. I wanted a metaphor of a road being twisty because it had to cross mountains.

marcus nunes

Mar 1 2021 at 7:06pm

Talking about interest rates, even of the “natural” variety is never satisfying. This post describes monetary policy exclusively in terms of NGDP growth relative to “trend”. It shows why the 90s were so stable. Implicitly, then, you can safely say the Fed followed the natural rate very closely!

https://marcusnunes.substack.com/p/inflation-mongering-is-back

Scott Sumner

Mar 1 2021 at 7:39pm

Yes, the natural rate is not very useful, as all we can do is infer we were close if NGDP is on track.

Tomas Breach

Mar 2 2021 at 2:24am

Hello Scott, you sometimes complain that economists exaggerate the Fed’s control over interest rates. But the view you lay out here sounds like mainstream Taylor Rule reasoning to me. Is there something missing from the central bank reaction functions conventional economists put in their models?

Scott Sumner

Mar 2 2021 at 11:50am

Tomas, I believe that economists tend to underestimate the extent to which the natural rate moves around. Thus during periods where the Fed is cutting rates, most economists think they are easing policy. I believe they are usually tightening policy, as the natural rate usually falls faster than the policy rate.

It’s not that the standard model is wrong, it’s that it’s misapplied.

Tomas Breach

Mar 2 2021 at 2:26pm

Thanks Scott, one last question: New Keynesians think the solution to the ZLB is to hold the policy rate at zero for a long time, longer than the liquidity trap lasts. When they see a sell-off in medium-term bonds, they fret that markets are disbelieving the zero rate commitment.

Is there something wrong with this perspective? You point out that a sell-off might be good news: markets expect inflation, and the Fed will follow the inflation to avoid “crashing the bus.” But New Keynesians might counter that inflation cannot arise if markets expect the Fed to follow its usual reaction function. Without some overheating tomorrow, policy will be tight today.

Rajat

Mar 2 2021 at 5:58am

“Why did interest rates rise during 1994? One could argue that the increase was caused by the Fed’s decision to raise its short-term rate target. Or one could argue that the Fed raised its target rate because the natural rate of interest rose as the economy strengthened in the mid-1990s, and they had to raise rates to keep inflation close to 2%. I find the latter explanation more useful.”

After rising strongly in 1993, the stock market fell when the Fed raised the funds rate in February 1994 and lost about 10% over the year. Doesn’t that suggest the Fed’s move was at least partly unexpected?

Scott Sumner

Mar 2 2021 at 11:51am

Yes, it was unexpected, but so was the rise in the natural rate of interest.

Michael Rulle

Mar 2 2021 at 9:23am

If you (Scott) were doing your own thought/real experiment, how would you try to create a test or prediction which could disprove your theory? For example, “natural rate of interest” is not observable and while it seems like it must exist (unlike dark matter which might not exist), it also can serve as a plug number to support a perspective.

I say this as someone who finds what you write persuasive —-yet economists I have liked and followed (e.g., Kling and Yardeni) differ significantly with you. (Although I have always liked them for reasons other than monetary theory, as the latter seems outside their primary area of interest)

Scott Sumner

Mar 2 2021 at 11:53am

The best test would be to stabilize NGDP futures prices. If it can’t be done, then I’m wrong. If it can be done, then Arnold Kling is wrong.

James

Mar 2 2021 at 1:01pm

What is the best test that can be done here and now when there is not currently an NGDP futures market?

Here is an idea: You monitor the public actions and statements of the Fed and make a public record of what you predict for inflation, unemployment, or any other variables that you think are affected by monetary policy in a predictable way. Then we compare the accuracy of your predictions to the out of sample accuracy of some very rudimentary AR(1) or exponential smoothing type models for the same variables.

Scott Sumner

Mar 3 2021 at 7:17pm

If you can consistently beat the market then don’t bother with predictions, just get rich!!

My forecast is always the market forecast.

Michael Rulle

Mar 3 2021 at 11:11am

I assume you are writing a shorthand version of a test. I think that because I assume one can manipulate (or target) the NGDP price if one has enough money (then again, many short squeezers have thought that—but they have limited funds). So, there have to be other actions to back up the Fed’s target. Right now, the target is inflation, —so perhaps we can use that as the shorthand?

Comments are closed.